An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

BLS corrected a number in the first sentence of the conclusion to say, "The prevalence of savings and thrift plans increased 10 percentage points from 2009 to 2012, unlike other types of defined contribution plans, which did not change significantly." The original sentence incorrectly said 6 percentage points, instead of 10 percentage points.

Defined contribution plans have become a major source of retirement savings for American workers as the number of employers offering defined benefit plans to employees has declined.1 There are a variety of defined contribution plan types available, including savings and thrift plans.

Features can vary among employer-sponsored savings and thrift plans. For example, some plans let employees take out loans from their accounts, and others do not. The Bureau of Labor Statistics National Compensation Survey (NCS) program periodically publishes detailed data to provide a deeper understanding of savings and thrift plans and other defined contribution plans available to employees.

This issue of Beyond the Numbers looks at the growth in the prevalence and at selected characteristics2 of employer-provided savings and thrift plans in private industry in the United States. The data for this article come from the National Compensation Survey: Health and Retirement Plan Provisions in Private Industry in the United States, 2012. In some instances, comparisons of 2012 data are made to 2009 data, which came from National Compensation Survey: Health and Retirement Plan Provisions in Private Industry in the United States, 2009.

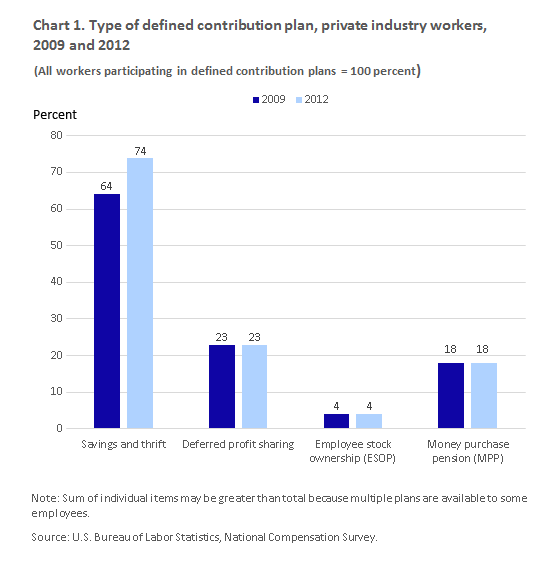

As seen in chart 1, data from the NCS revealed that 74 percent of participants in defined contribution plans in private industry participated in a savings and thrift plan in 2012, an increase from 64 percent in 2009. Over the same period, there was no significant change in the prevalence of other types of defined contribution plans: defined profit sharing, employee stock ownership (ESOP), and money purchase pensions.

A savings and thrift plan is a retirement account held by an employee in which a predetermined portion of his or her earnings can be saved.3 The employee’s contribution is usually not taxed until withdrawal. Employees are often allowed to select how their contributions are invested.4 In addition, some savings and thrift plans allow employees to receive loans or withdraw funds before retirement.

Savings and thrift and other defined contribution plans, such as money purchase pension and deferred profit-sharing plans, may fall under the 401(k) tax provision whereby employees are not taxed on contributions until benefits are disbursed.5 All savings and thrift plans are 401(k) plans, but not all 401(k) plans are savings and thrift plans. A defining characteristic of savings and thrift plans is employee contribution with employer matching. In order to receive the matching employer contribution, the employee must make contributions.

Other defined contribution plans usually do not have this employee contribution requirement. For example, participants in deferred profit-sharing plans are not required to make contributions in order to receive a share of the company’s profits. Money purchase plans sometimes allow employee contributions but do not require them.6 Similarly, employee stock ownership plans (ESOPs) will purchase company stock for the employee without requiring employee contributions.

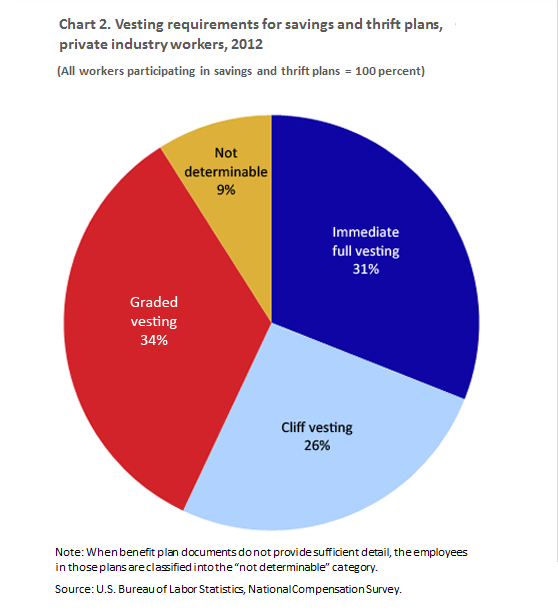

In the context of employee benefits, the two eligibility requirements identified by the NCS are the employee’s age and the length of time an employee must work before being eligible to participate in the plan, also called a service requirement. The service requirement is not to be confused with the vesting requirement, which is the length of time it takes for an employee to acquire full rights to the employer’s contribution to a retirement plan.

Among participants in savings and thrift plans offered by private industry employers:

Employees always have full ownership of their own contributions to the savings and thrift account. However, most savings and thrift plans require employees to wait a period of time until they have full rights to the employer’s contribution. This is what is known as the vesting requirement. Once this requirement is fulfilled, the employee’s right to the employer’s contribution is retained even in the event of a separation from the employer prior to retirement. NCS reports on three types of vesting requirements in savings and thrift plans:

When workers move from one job to another, they have to decide what will happen to the defined contribution retirement accounts provided by the previous employer. Rollover features are common in savings and thrift plans; they give employees an ability to transfer or roll over funds from other defined contribution plans into their current savings and thrift plan.

NCS data show that in 2012, 78 percent of private industry workers participating in savings and thrift plans had the option to roll over the assets from previous defined contribution plans into a current employer’s savings and thrift plan. Four percent of workers participating in savings and thrift plans in 2012 were not allowed to roll over funds into the current plans. It could not be determined for 18 percent of workers participating in savings and thrift plans in 2012 whether the rollover option existed.

In 2012, 58 percent of private industry workers participating in saving and thrift plans had the option to take out loans, with interest, from their savings and thrift plan before retirement. Loans typically must be repaid within 5 years and are limited to a portion of the account balance.7 Taking loans from one’s savings and thrift plan is discouraged, as employees have become more dependent on savings and thrift plans as their main source of retirement savings. While the employee is repaying a loan, contributions from the company are sometimes halted until the loan is repaid.8 NCS data on loans from savings and thrift accounts take into account only those loans that come from employees’ fully vested contributions.

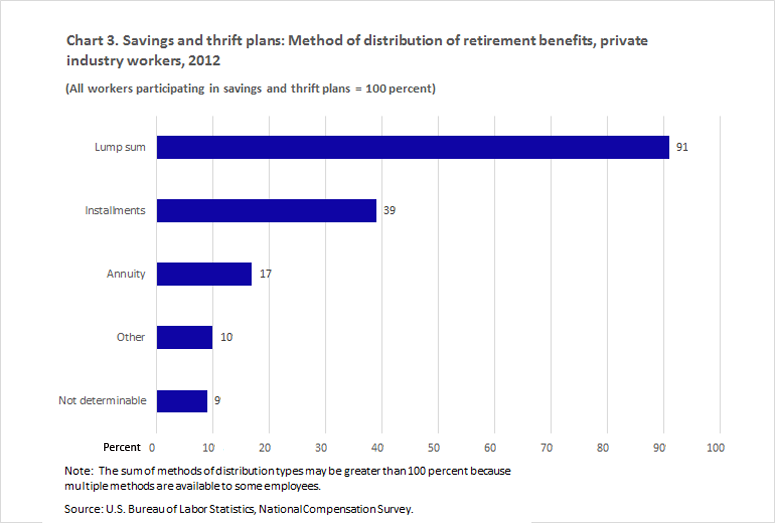

NCS produces data on four methods of benefit distribution in which savings and thrift plans are made available to employees upon retirement. (See chart 3.) Some employees have the option to receive their retirement savings in a combination of the methods of disbursement outlined below. However, employees who have a choice of disbursement method typically must choose only one:

Lump-sum option—The retiree can receive all the assets in his or her savings and thrift plan, both employee and employer contributions, plus interest and earnings, at one time. Among savings and thrift plan participants in private industry in 2012, 91 percent had this option available, compared with 90 percent in 2009.

Installments—Retirees receive regular payments from their savings and thrift plan until all savings have been depleted. If funds are still available after the death of the recipient, the remaining installment payments go to his or her estate. In 2012, 39 percent could receive their retirement savings in the form of installments. In 2009, 27 percent had that option.

Annuity—Retirees typically receive the benefit as a stream of guaranteed periodic payments over their lifetime. In 2012, 17 percent had an annuity option available. In 2009, that number was 15 percent.

Other—Such as a combination of installments and annuity. In 2012, 10 percent of private industry workers in savings and thrift plans had an option from the “other” category available, compared with 12 percent in 2009.

The prevalence of savings and thrift plans increased 10 percentage points from 2009 to 2012, unlike other types of defined contribution plans, which did not change significantly. When compared with cliff vesting or immediate full vesting, graded vesting is slightly more prevalent in savings and thrifts plans. Approximately four-fifths of private industry workers participating in savings and thrift plans had the option to roll over the assets from previous defined contribution plans into a current employer’s savings and thrift plan. More than half of savings and thrift plan participants were eligible to receive loans from their savings and thrift plans. The majority of savings and thrift plan participants were able to receive their savings and thrift savings in a lump sum upon retirement. Most savings and thrift plan participants had eligibility requirements based on length of service and/or age in order to participate in their employers’ savings and thrift plans.

This Beyond the Numbers article was prepared by John E. Foster and David C. Zook, economists in the Office of Compensation and Working Conditions, email: Zook.David@bls.gov, telephone: (202) 691-6224.

Information in this article will be made available to sensory-impaired individuals upon request. Voice phone: (202) 691-5200. Federal Relay Service: 1-800-877-8339. This article is in the public domain and may be reproduced without permission.

John E. Foster and David C. Zook, “Selected characteristics of savings and thrift plans for private industry workers,” Beyond the Numbers: Pay & Benefits, vol. 4, no. 11 (U.S. Bureau of Labor Statistics, July 2015), https://www.bls.gov/opub/btn/volume-4/selected-characteristics-of-savings-and-thrift-plans-for-private-industry-workers.htm

1 Defined benefit pension plans guarantee retirement benefits based on formulas that take into account a participant’s retirement age, length of service, or pre-retirement earnings. In contrast, defined contribution plans only guarantee the employer’s contribution over the course of an employee’s career, not the final amount of retirement savings received by an employee. See “The last private industry pension plans: a visual essay” by William J. Wiatrowski regarding the declining incidence of defined benefit pension plans (https://www.bls.gov/opub/mlr/2012/12/art1full.pdf).

2 The terms “core” and “non-core” are used by NCS to describe key attributes of plans (core) and more detailed provisions of health and retirement plans (non-core). Due to resource constraints, data on the more detailed provisions are not collected every year. The NCS questionnaire on savings and thrift plans includes questions on plan type, employee and employer contribution, investment options with respect to employers’ contributions, and automatic enrollment. Non-core questions cover savings and thrift eligibility and vesting, investment of savings and thrift funds, the ability to roll over other defined contribution plans into an employer’s savings and thrift plan, the ability to take out loans from one’s savings and thrift plan, and disbursements of savings and thrift plans. This article covers non-core attributes of savings and thrift plans.

3 See “National Compensation Survey: Glossary of Employee Benefit Terms” for information about other types of defined contribution plans (https://www.bls.gov/ncs/ebs/glossary20112012.htm#retirement_benefits).

4 See “Employees given range of investment options in 401(k) plans” (https://www.bls.gov/opub/btn/archive/program-perspectives-on-defined-contribution-plan-investment-choices-pdf.pdf).

5 See “401(k) Plans” from the Internal Revenue Service (http://www.irs.gov/Retirement-Plans/401(k)-Plans).

6 An exception exists for some money purchase plans, notably TIAA-CREF plans used by academic institutions, which require dual funding: in order to get the larger employer contribution, an employee must contribute a set percentage to the plan. This is not a match per se.

7 See “National Compensation Survey: Glossary of Employee Benefit Terms,” (https://www.bls.gov/ncs/ebs/glossary20132014.htm#retirement_benefits)

8 See Beshears, John, Choi, James J., Laibson, David, Madrian, Brigitte C., A Primer on 401(k) Loans, Prepared for the 10th Annual Joint Conference of the Retirement Research Consortium August 7–8, 2008 Washington, D.C. (http://scholar.harvard.edu/files/laibson/files/a_primer_on_401k_loans.pdf)

Publish Date: Wednesday, July 1, 2015