An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

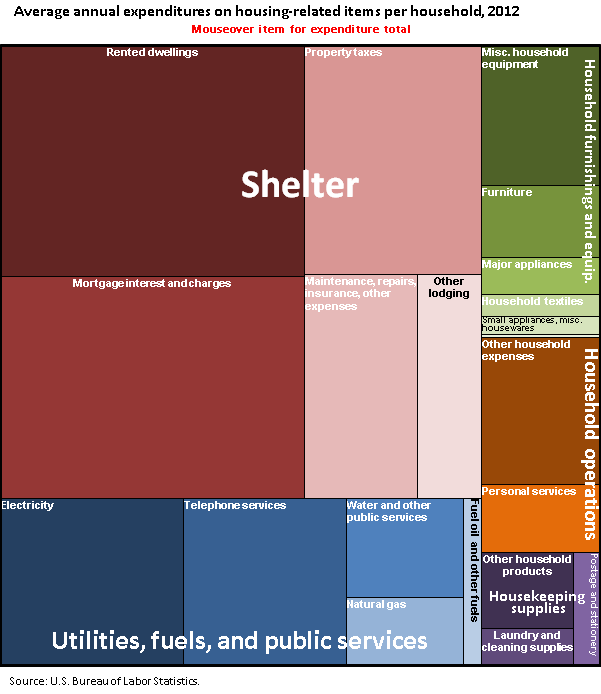

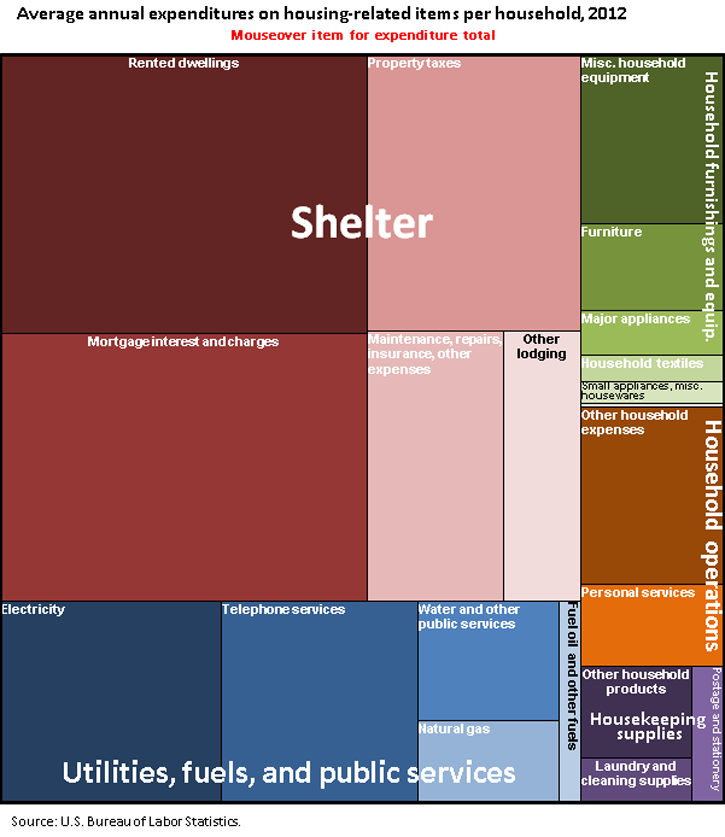

| Item | Expenditure |

|---|---|

|

Shelter, total |

$16,887 |

|

Owned dwellings |

|

|

Mortgage interest and charges |

3,067 |

|

Property taxes |

1,836 |

|

Maintenance, repairs, insurance, other expenses |

1,153 |

|

Rented dwellings |

3,186 |

|

Other lodging |

649 |

|

Utilities, fuels, and public services |

|

|

Natural gas |

359 |

|

Electricity |

1,388 |

|

Fuel oil and other fuels |

137 |

|

Telephone services |

1,239 |

|

Water and other public services |

525 |

|

Household operations |

|

|

Personal services |

368 |

|

Other household expenses |

791 |

|

Housekeeping supplies |

|

|

Laundry and cleaning supplies |

155 |

|

Other household products |

319 |

|

Postage and stationery |

136 |

|

Household furnishings and equipment |

|

|

Household textiles |

123 |

|

Furniture |

391 |

|

Floor coverings |

16 |

|

Major appliances |

197 |

|

Small appliances, misc. housewares |

98 |

|

Misc. household equipment |

754 |

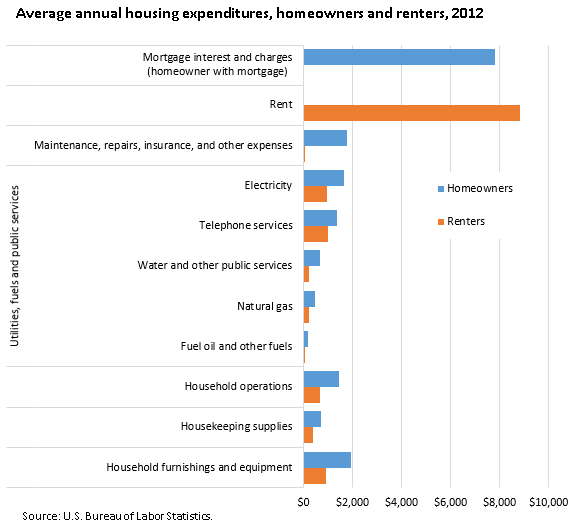

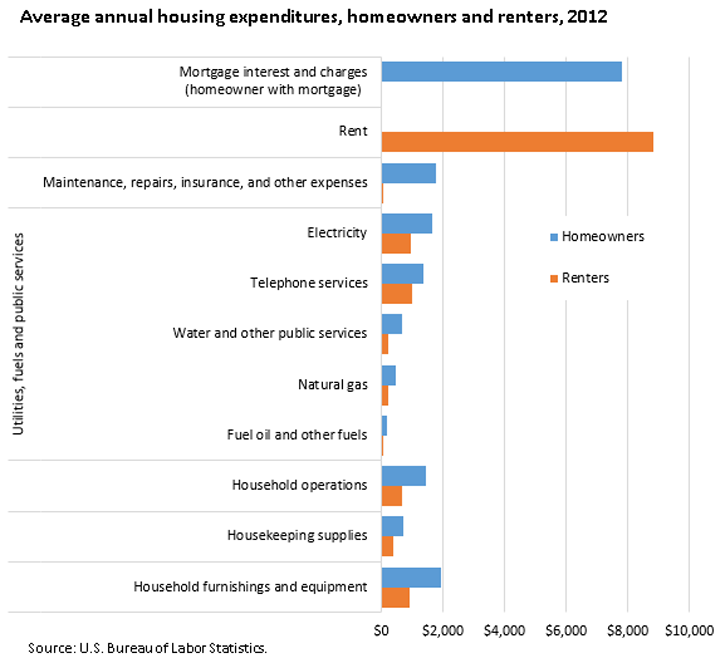

| Expenditure | Homeowners | Renters |

|---|---|---|

|

Mortgage interest and charges (homeowner with mortgage) |

$7,782 | |

|

Rent |

$8,812 | |

|

Utilities, fuels and public services |

||

|

Maintenance, repairs, insurance, and other expenses |

1,788 | 13 |

|

Electricity |

1,633 | 948 |

|

Telephone services |

1,382 | 982 |

|

Water and other public services |

683 | 241 |

|

Natural gas |

447 | 202 |

|

Fuel oil and other fuels |

194 | 35 |

|

Household operations |

1,439 | 655 |

|

Housekeeping supplies |

725 | 403 |

|

Household furnishings and equipment |

1,947 | 918 |

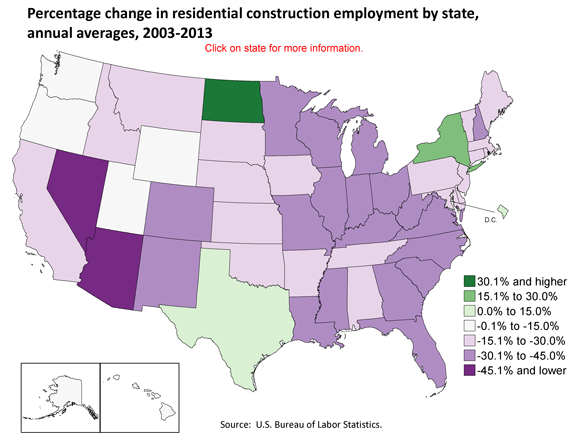

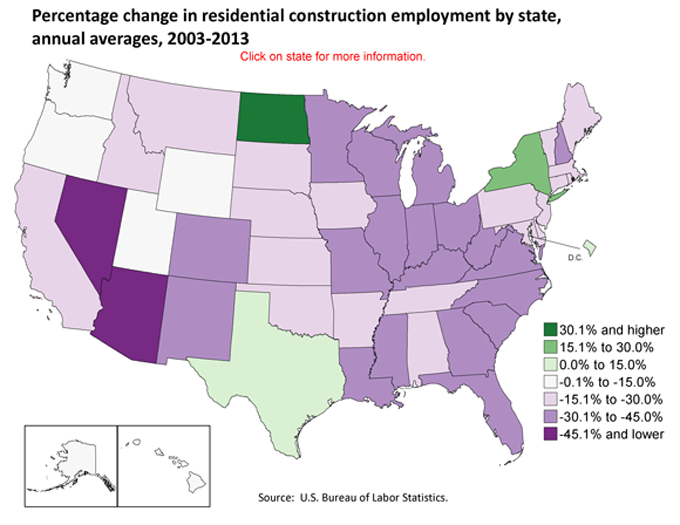

| State | Employment | Percent change | |

|---|---|---|---|

| 2003 | 2013(p) | ||

|

Alabama |

7,839 | 5,559 | -29.1 |

|

Alaska |

2,008 | 1,730 | -13.8 |

|

Arizona |

20,774 | 10,746 | -48.3 |

|

Arkansas |

3,745 | 2,761 | -26.3 |

|

California |

117,853 | 87,555 | -25.7 |

|

Colorado |

17,720 | 11,532 | -34.9 |

|

Connecticut |

7,657 | 5,425 | -29.1 |

|

Delaware |

3,511 | 2,612 | -25.6 |

|

District of Columbia |

1,111 | 1,141 | 2.7 |

|

Florida |

61,518 | 40,972 | -33.4 |

|

Georgia |

19,846 | 11,582 | -41.6 |

|

Hawaii |

4,475 | 3,804 | -15.0 |

|

Idaho |

5,465 | 4,184 | -23.4 |

|

Illinois |

35,409 | 19,686 | -44.4 |

|

Indiana |

18,146 | 11,563 | -36.3 |

|

Iowa |

7,617 | 5,822 | -23.6 |

|

Kansas |

6,350 | 4,924 | -22.5 |

|

Kentucky |

7,796 | 5,219 | -33.1 |

|

Louisiana |

7,813 | 5,425 | -30.6 |

|

Maine |

5,390 | 3,772 | -30.0 |

|

Maryland |

25,193 | 17,724 | -29.6 |

|

Massachusetts |

17,703 | 13,346 | -24.6 |

|

Michigan |

26,438 | 15,678 | -40.7 |

|

Minnesota |

16,656 | 10,190 | -38.8 |

|

Mississippi |

3,777 | 2,079 | -45.0 |

|

Missouri |

17,068 | 9,527 | -44.2 |

|

Montana |

4,261 | 3,510 | -17.6 |

|

Nebraska |

4,833 | 3,755 | -22.3 |

|

Nevada |

9,984 | 4,796 | -52.0 |

|

New Hampshire |

4,701 | 2,862 | -39.1 |

|

New Jersey |

25,331 | 20,400 | -19.5 |

|

New Mexico |

7,127 | 4,322 | -39.4 |

|

New York |

38,914 | 48,785 | 25.4 |

|

North Carolina |

31,811 | 20,328 | -36.1 |

|

North Dakota |

1,627 | 2,394 | 47.1 |

|

Ohio |

28,332 | 17,098 | -39.7 |

|

Oklahoma |

5,865 | 4,178 | -28.8 |

|

Oregon |

10,625 | 10,106 | -4.9 |

|

Pennsylvania |

36,006 | 25,973 | -27.9 |

|

Rhode Island |

3,217 | 2,331 | -27.5 |

|

South Carolina |

12,917 | 7,236 | -44.0 |

|

South Dakota |

2,968 | 2,478 | -16.5 |

|

Tennessee |

12,498 | 9,159 | -26.7 |

|

Texas |

38,678 | 41,652 | 7.7 |

|

Utah |

9,171 | 8,110 | -11.6 |

|

Vermont |

3,195 | 2,458 | -23.1 |

|

Virginia |

27,779 | 18,855 | -32.1 |

|

Washington |

21,015 | 19,137 | -8.9 |

|

West Virginia |

5,815 | 3,867 | -33.5 |

|

Wisconsin |

15,734 | 9,439 | -40.0 |

|

Wyoming |

2,735 | 2,347 | -14.2 |

|

Footnotes: |

|||

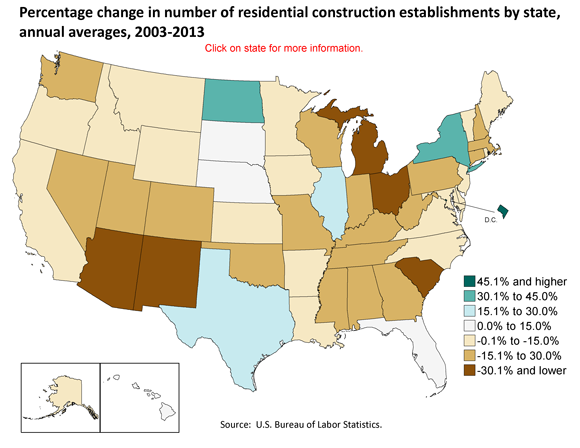

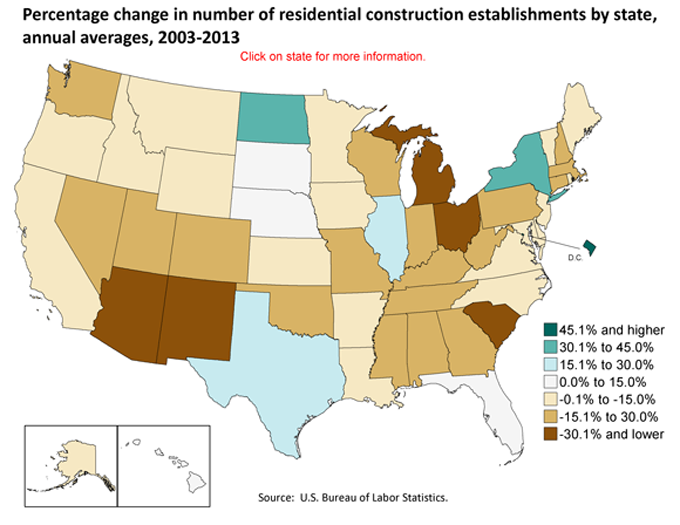

| State | Number of establishments | Percent change | |

|---|---|---|---|

| 2003 | 2013(p) | ||

|

Alabama |

2,093 | 1,667 | -25.9 |

|

Alaska |

468 | 462 | -1.3 |

|

Arizona |

3,213 | 2,394 | -31.2 |

|

Arkansas |

1,194 | 1,048 | -10.9 |

|

California |

19,395 | 16,600 | -14.1 |

|

Colorado |

4,508 | 3,526 | -23.1 |

|

Connecticut |

2,332 | 1,870 | -21.7 |

|

Delaware |

727 | 643 | -12.1 |

|

District of Columbia |

123 | 225 | 45.5 |

|

Florida |

10,408 | 10,995 | 9.0 |

|

Georgia |

5,532 | 3,931 | -28.8 |

|

Hawaii |

742 | 759 | 4.3 |

|

Idaho |

1,729 | 1,519 | -14.5 |

|

Illinois |

8,757 | 10,741 | 24.3 |

|

Indiana |

4,258 | 3,330 | -23.7 |

|

Iowa |

2,082 | 1,864 | -10.0 |

|

Kansas |

1,700 | 1,426 | -14.9 |

|

Kentucky |

1,986 | 1,496 | -21.4 |

|

Louisiana |

1,751 | 1,747 | -3.0 |

|

Maine |

1,470 | 1,434 | -5.7 |

|

Maryland |

4,949 | 4,681 | -7.0 |

|

Massachusetts |

4,995 | 4,444 | -15.7 |

|

Michigan |

7,802 | 4,775 | -41.4 |

|

Minnesota |

4,029 | 3,712 | -14.3 |

|

Mississippi |

994 | 774 | -22.3 |

|

Missouri |

3,954 | 3,005 | -25.2 |

|

Montana |

1,513 | 1,412 | -5.1 |

|

Nebraska |

1,268 | 1,237 | 0.9 |

|

Nevada |

1,028 | 843 | -16.1 |

|

New Hampshire |

1,162 | 905 | -24.4 |

|

New Jersey |

6,157 | 5,527 | -6.5 |

|

New Mexico |

1,710 | 1,224 | -32.0 |

|

New York |

10,295 | 13,646 | 36.6 |

|

North Carolina |

7,236 | 6,826 | -11.4 |

|

North Dakota |

503 | 699 | 44.7 |

|

Ohio |

6,709 | 4,641 | -32.2 |

|

Oklahoma |

1,411 | 1,211 | -17.5 |

|

Oregon |

3,812 | 3,299 | -12.6 |

|

Pennsylvania |

8,393 | 6,851 | -19.0 |

|

Rhode Island |

899 | 899 | -4.3 |

|

South Carolina |

3,195 | 1,965 | -36.6 |

|

South Dakota |

796 | 884 | 10.6 |

|

Tennessee |

2,591 | 2,182 | -16.0 |

|

Texas |

6,241 | 7,200 | 17.8 |

|

Utah |

2,552 | 1,945 | -22.3 |

|

Vermont |

888 | 787 | -13.7 |

|

Virginia |

5,756 | 5,301 | -12.0 |

|

Washington |

6,602 | 5,188 | -17.7 |

|

West Virginia |

1,670 | 1,209 | -28.7 |

|

Wisconsin |

4,088 | 3,117 | -26.2 |

|

Wyoming |

735 | 726 | -4.6 |

|

Footnotes: |

|||

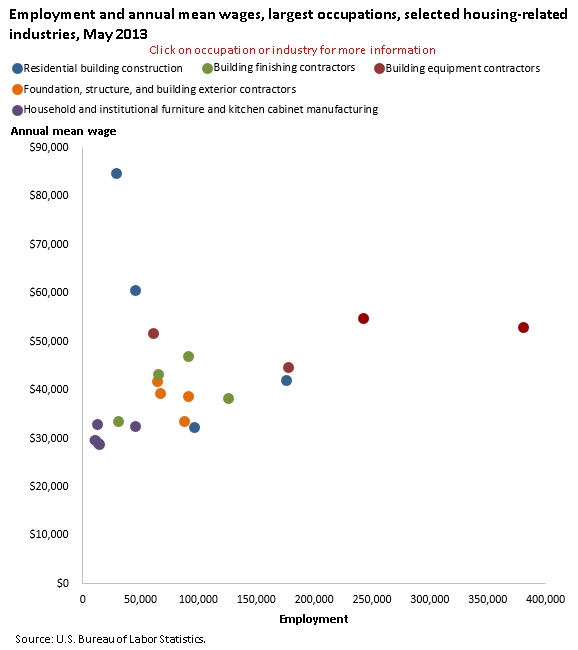

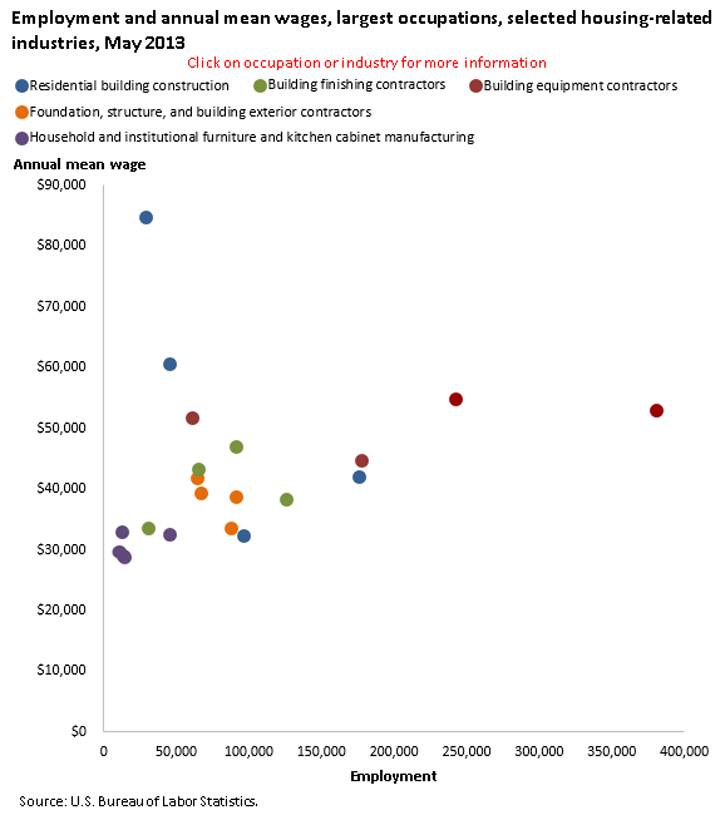

| Industry | Employment | Annual mean wage |

|---|---|---|

|

Residential building construction |

||

|

Construction managers |

29,010 | $84,650 |

|

First-line supervisors of construction trades and extraction workers |

45,480 | 60,660 |

|

Construction Laborers |

96,080 | 32,340 |

|

Carpenters |

176,260 | 41,990 |

|

Building finishing contractors |

||

|

Construction Laborers |

30,520 | 33,510 |

|

Drywall and ceiling tile installers |

65,610 | 43,240 |

|

Carpenters |

90,970 | 46,860 |

|

Painters, construction and maintenance |

125,750 | 38,340 |

|

Building equipment contractors |

||

|

Sheet metal workers |

61,120 | 51,660 |

|

Heating, air conditioning, and refrigeration mechanics and installers |

177,580 | 44,680 |

|

Plumbers, pipefitters, and steamfitters |

242,720 | 54,850 |

|

Electricians |

380,900 | 52,980 |

|

Foundation, structure, and building exterior contractors |

||

|

Carpenters |

64,330 | 41,730 |

|

Cement masons and concrete finishers |

66,700 | 39,300 |

|

Construction laborers |

87,400 | 33,590 |

|

Roofers |

91,250 | 38,580 |

|

Household and institutional furniture and kitchen cabinet manufacturing |

||

|

Upholsterers |

12,270 | 32,870 |

|

Woodworking machine setters, operators, and tenders, except sawing |

13,230 | 28,960 |

|

Team assemblers |

14,720 | 28,730 |

|

Cabinetmakers and bench carpenters |

45,290 | 32,450 |

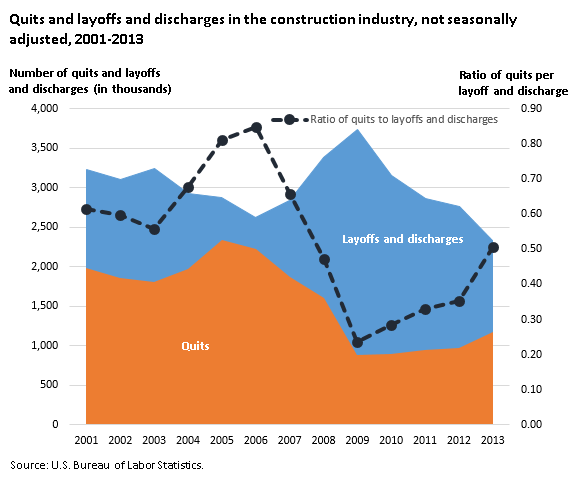

| Year | Layoffs and discharges | Quits | Ratio of quits to layoffs and discharges |

|---|---|---|---|

2001 | 3,226 | 1,987 | 0.62 |

2002 | 3,106 | 1,856 | 0.60 |

2003 | 3,245 | 1,811 | 0.56 |

2004 | 2,922 | 1,975 | 0.68 |

2005 | 2,878 | 2,335 | 0.81 |

2006 | 2,623 | 2,228 | 0.85 |

2007 | 2,843 | 1,867 | 0.66 |

2008 | 3,389 | 1,604 | 0.47 |

2009 | 3,743 | 888 | 0.24 |

2010 | 3,156 | 901 | 0.29 |

2011 | 2,868 | 947 | 0.33 |

2012 | 2,769 | 975 | 0.35 |

2013 | 2,328 | 1,180 | 0.51 |

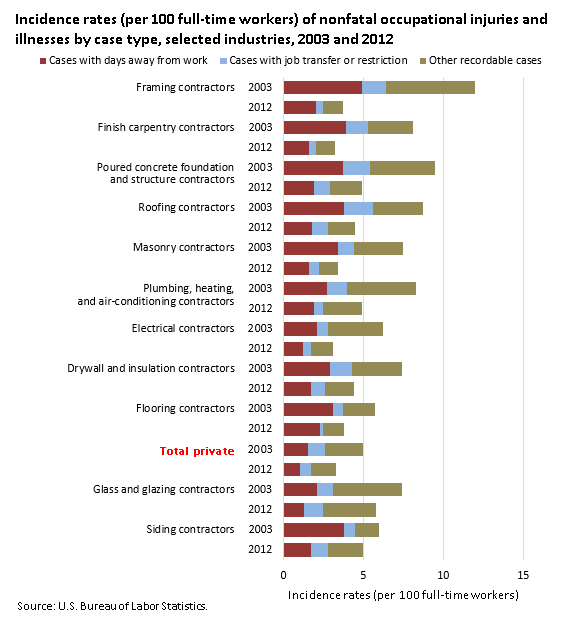

| Industry | Year | Cases with days away from work | Cases with job transfer or restriction | Other recordable cases |

|---|---|---|---|---|

Framing contractors | 2003 | 4.9 | 1.5 | 5.6 |

| 2012 | 2.0 | 0.5 | 1.2 |

Finish carpentry contractors | 2003 | 3.9 | 1.4 | 2.8 |

| 2012 | 1.6 | 0.4 | 1.2 |

Poured concrete foundation and structure contractors | 2003 | 3.7 | 1.7 | 4.1 |

| 2012 | 1.9 | 1.0 | 2.0 |

Roofing contractors | 2003 | 3.8 | 1.8 | 3.1 |

| 2012 | 1.8 | 1.0 | 1.7 |

Masonry contractors | 2003 | 3.4 | 1.0 | 3.1 |

| 2012 | 1.6 | 0.6 | 1.2 |

Plumbing, heating, and air-conditioning contractors | 2003 | 2.7 | 1.3 | 4.3 |

| 2012 | 1.9 | 0.6 | 2.4 |

Electrical contractors | 2003 | 2.1 | 0.7 | 3.4 |

| 2012 | 1.2 | 0.5 | 1.4 |

Drywall and insulation contractors | 2003 | 2.9 | 1.4 | 3.1 |

| 2012 | 1.7 | 0.9 | 1.8 |

Flooring contractors | 2003 | 3.1 | 0.6 | 2.0 |

| 2012 | 2.3 | 0.2 | 1.3 |

Total private | 2003 | 1.5 | 1.1 | 2.4 |

| 2012 | 1.0 | 0.7 | 1.6 |

Glass and glazing contractors | 2003 | 2.1 | 1.0 | 4.3 |

| 2012 | 1.3 | 1.2 | 3.3 |

Siding contractors | 2003 | 3.8 | 0.7 | 1.5 |

| 2012 | 1.7 | 1.1 | 2.2 |

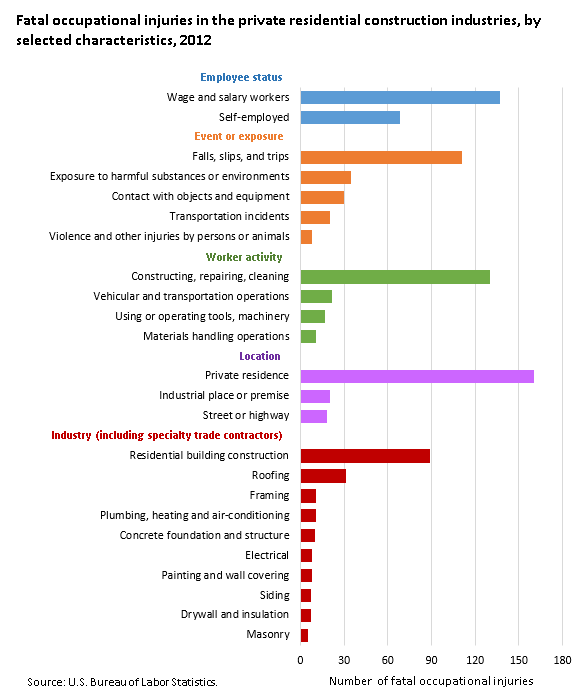

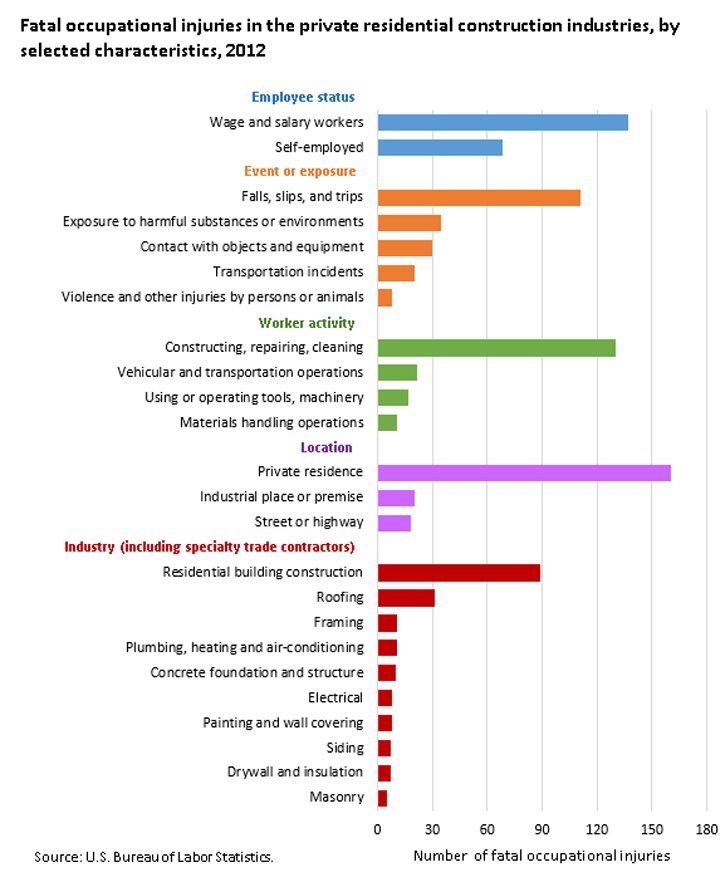

| Characteristic | Number of fatal occupational injuries |

|---|---|

|

Employee status |

|

|

Wage and salary workers |

137 |

|

Self-employed |

68 |

|

Event or exposure |

|

|

Falls, slips, and trips |

111 |

|

Exposure to harmful substances or environments |

35 |

|

Contact with objects and equipment |

30 |

|

Transportation incidents |

20 |

|

Violence and other injuries by persons or animals |

8 |

|

Worker activity |

|

|

Constructing, repairing, cleaning |

130 |

|

Vehicular and transportation operations |

22 |

|

Using or operating tools, machinery |

17 |

|

Materials handling operations |

11 |

|

Location |

|

|

Private residence |

160 |

|

Industrial place or premise |

20 |

|

Street or highway |

18 |

|

Industry (including specialty trade contractors) |

|

|

Residential building construction |

89 |

|

Roofing |

31 |

|

Framing |

11 |

|

Plumbing, heating and air-conditioning |

11 |

|

Concrete foundation and structure |

10 |

|

Electrical |

8 |

|

Painting and wall covering |

8 |

|

Siding |

7 |

|

Drywall and insulation |

7 |

|

Masonry |

5 |