Whether I’m working from my home “office” or I travel into my “real” office, I notice a lot of construction activity. In my neighborhood, the number of work trucks seems to multiply every day, with homeowners getting new roofs, updated decks, expanded kitchens, and even large additions. Away from the neighborhood, I pass cranes high above me that are the makings of new residences, new office buildings, new schools, and more. Given all this construction, I thought I’d take a look at what BLS data have to say about construction prices.

I am going to focus on the Producer Price Index (PPI) for “intermediate demand.” You might already be familiar with the PPI, which was first published in 1902. The PPI measures the average change over time in the selling prices domestic producers receive for their output. The headline number reports on “final demand.” That is the average change in selling prices received by producers for products sold for personal consumption, capital investment, government, and export. But what about goods and services sold to businesses for further production, such as those used in construction projects? That’s where the “intermediate demand” index comes in.

Within the intermediate demand categories, the PPI provides price changes for both services and goods. Goods used for construction include “materials” and “components.” Materials are partially processed products that will be further processed into completed products. Softwood lumber and plywood are examples of materials.

Components are complete commodities purchased for assembly with other commodities. Sinks, windows, and doors are “components.” There are other inputs to construction as well, such as energy, transportation, and trade services, which fall into other PPI intermediate demand categories. But today the main focus is on materials and components we see every day at construction sites.

Your local roofing contractor and the mega-construction company building that new hospital are affected by the change in price for these intermediate demand goods. Those price changes probably are passed on to the final customer. So let’s look at what’s been happening to some of those intermediate demand prices.

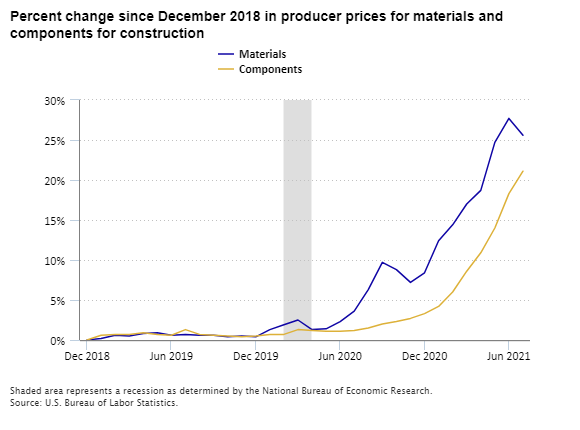

Overall, the price of materials and components for construction registered a 1-month increase of 0.6 percent in July 2021 and a 20-percent increase from a year earlier. Here’s a chart showing a little longer history, separately for materials and components. The prices of both changed little during 2019 but surged upward later. Between the two, materials prices grew earlier, and by a larger amount, but fell back a bit in July 2021.

Editor’s note: Data for this chart are available in the table below.

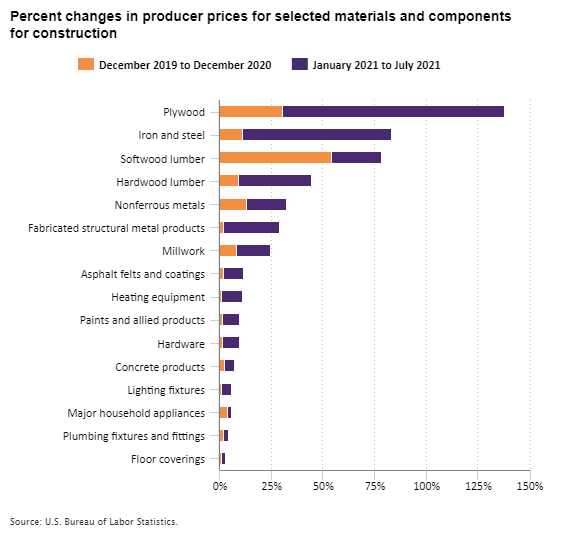

The PPI measures price changes for many products. I chose a few, based on some local construction projects I’ve seen lately. For example, the neighbor down the street is putting a two-story addition onto the back of her house. A project like that probably requires a lot of wood products—and that might make it expensive. In the last 19 months, the prices received by producers of plywood more than doubled.

Along the nearby highway, there’s a large warehouse under construction, perhaps related to the increase in online shopping and home delivery. The owner may have seen price increases for many of the construction materials, including an 83-percent increase in the price of iron and steel in the past 19 months. The second chart shows that large price increases in wood and metal products dwarfed those observed for most other materials and components for construction.

It’s time for a new roof at my house—and I see companies producing the asphalt products used on roofs charged 12 percent higher prices in July 2021 than 19 months earlier. From my window, I can see one neighbor is replacing an aging heating and air conditioning unit, while another is installing a new patio. Their contractors are experiencing a variety of price changes. In the past 19 months, producer prices rose 11 percent for heating equipment and 7 percent for concrete products. Finally, with a lot of people spending the last year or more working and schooling from home, it may be time to spruce up that interior. Some of the materials your contractor may need include cabinets, windows, doors, and other “millwork,” whose prices over the last 19 months are up 25 percent; paint products, up 10 percent; lighting fixtures, up 6 percent; and sinks and other plumbing fixtures, up 4 percent.

Unusually large and fast price increases sometimes turn out to be temporary. Fuel prices often are volatile like this. Recently, construction materials prices might have been as well. In July 2021, producer prices for softwood lumber fell 29 percent.

Editor’s note: Data for this chart are available in the table below.

BLS measures changes in producer prices for items like these each month. The PPI moves differently for final demand and intermediate demand because the mix of goods and services consumed by these users differs. Likewise, even within the construction sector, the mix of inputs used for production varies. For example, construction of single-family homes might require more lumber, while construction of warehouses might require more steel.

We just looked at the producer price indexes that examine “intermediate demand” for detailed materials and components used in construction overall. Additional breakdowns of price changes for products used in construction and other industries are available from a different set of producer price indexes, known as the “inputs to industry” indexes. These two sets of indexes rely on somewhat different data and methods to track different producers’ use of inputs, so their estimates of overall producer price changes sometimes differ slightly. Together they offer a fuller picture. The inputs-to-industry indexes offer a more detailed breakdown of price changes for inputs consumed by specific construction industries.

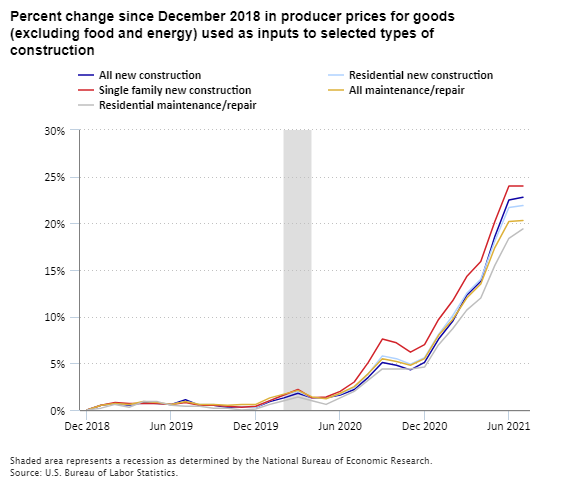

Consider the overall producer prices paid for goods (excluding food and energy) used as inputs to different types of construction. The third chart shows that these prices rose most for construction of new single-family homes. This might partly reflect more intensive use of softwood lumber in construction of new single family homes than in some other types of construction.

Editor’s note: Data for this chart are available in the table below.

The price changes examined here just scratch the surface of the detail available from the PPI each month. As you think about your next homeowner project or pass by another large construction site, you now know where you can find that latest information on selling prices for intermediate demand. These data let you know how much contractors’ input prices change for the materials they need for the projects in your homes and neighborhoods.

| Month | Materials | Components |

|---|---|---|

| Dec 2018 | 0.0% | 0.0% |

| Jan 2019 | 0.2 | 0.6 |

| Feb 2019 | 0.6 | 0.7 |

| Mar 2019 | 0.5 | 0.7 |

| Apr 2019 | 0.8 | 0.9 |

| May 2019 | 0.9 | 0.7 |

| Jun 2019 | 0.6 | 0.6 |

| Jul 2019 | 0.7 | 1.3 |

| Aug 2019 | 0.6 | 0.7 |

| Sep 2019 | 0.6 | 0.6 |

| Oct 2019 | 0.4 | 0.5 |

| Nov 2019 | 0.5 | 0.4 |

| Dec 2019 | 0.4 | 0.5 |

| Jan 2020 | 1.3 | 0.7 |

| Feb 2020 | 1.9 | 0.7 |

| Mar 2020 | 2.5 | 1.3 |

| Apr 2020 | 1.3 | 1.2 |

| May 2020 | 1.4 | 1.1 |

| Jun 2020 | 2.3 | 1.1 |

| Jul 2020 | 3.6 | 1.2 |

| Aug 2020 | 6.3 | 1.5 |

| Sep 2020 | 9.7 | 2.0 |

| Oct 2020 | 8.8 | 2.3 |

| Nov 2020 | 7.2 | 2.7 |

| Dec 2020 | 8.4 | 3.3 |

| Jan 2021 | 12.4 | 4.2 |

| Feb 2021 | 14.4 | 6.0 |

| Mar 2021 | 17.0 | 8.6 |

| Apr 2021 | 18.7 | 10.9 |

| May 2021 | 24.7 | 14.0 |

| Jun 2021 | 27.7 | 18.3 |

| Jul 2021 | 25.6 | 21.1 |

| Material or component | December 2019 to December 2020 | January 2021 to July 2021 |

|---|---|---|

| Plywood | 30.7% | 107.2% |

| Iron and steel | 11.3 | 72.1 |

| Softwood lumber | 54.3 | 23.9 |

| Hardwood lumber | 9.2 | 35.5 |

| Nonferrous metals | 13.0 | 19.6 |

| Fabricated structural metal products | 2.0 | 27.1 |

| Millwork | 8.4 | 16.5 |

| Asphalt felts and coatings | 2.1 | 9.6 |

| Heating equipment | 0.6 | 10.4 |

| Paints and allied products | 1.6 | 8.3 |

| Hardware | 1.4 | 8.1 |

| Concrete products | 2.2 | 4.9 |

| Lighting fixtures | 1.2 | 4.6 |

| Major household appliances | 3.9 | 1.8 |

| Plumbing fixtures and fittings | 1.9 | 2.4 |

| Floor coverings | 0.4 | 2.6 |

| Month | All new construction | Residential new construction | Single family new construction | All maintenance/repair | Residential maintenance/repair |

|---|---|---|---|---|---|

| Dec 2018 | 0.0% | 0.0% | 0.0% | 0.0% | 0.0% |

| Jan 2019 | 0.5 | 0.5 | 0.5 | 0.5 | 0.2 |

| Feb 2019 | 0.7 | 0.7 | 0.8 | 0.7 | 0.6 |

| Mar 2019 | 0.5 | 0.6 | 0.7 | 0.6 | 0.3 |

| Apr 2019 | 0.8 | 0.7 | 0.7 | 0.9 | 0.9 |

| May 2019 | 0.7 | 0.7 | 0.7 | 0.8 | 0.9 |

| Jun 2019 | 0.6 | 0.6 | 0.6 | 0.6 | 0.5 |

| Jul 2019 | 1.1 | 0.9 | 0.8 | 0.9 | 0.4 |

| Aug 2019 | 0.5 | 0.6 | 0.5 | 0.6 | 0.4 |

| Sep 2019 | 0.5 | 0.6 | 0.5 | 0.6 | 0.2 |

| Oct 2019 | 0.3 | 0.4 | 0.4 | 0.5 | 0.2 |

| Nov 2019 | 0.3 | 0.3 | 0.3 | 0.6 | 0.0 |

| Dec 2019 | 0.3 | 0.3 | 0.4 | 0.6 | 0.1 |

| Jan 2020 | 0.9 | 1.0 | 1.0 | 1.3 | 0.6 |

| Feb 2020 | 1.3 | 1.6 | 1.6 | 1.7 | 1.0 |

| Mar 2020 | 1.8 | 2.0 | 2.2 | 2.1 | 1.4 |

| Apr 2020 | 1.3 | 1.3 | 1.3 | 1.4 | 1.0 |

| May 2020 | 1.3 | 1.3 | 1.4 | 1.2 | 0.6 |

| Jun 2020 | 1.6 | 1.7 | 2.0 | 1.8 | 1.3 |

| Jul 2020 | 2.2 | 2.4 | 3.0 | 2.5 | 2.0 |

| Aug 2020 | 3.5 | 3.9 | 5.1 | 3.9 | 3.2 |

| Sep 2020 | 5.1 | 5.8 | 7.6 | 5.5 | 4.4 |

| Oct 2020 | 4.8 | 5.5 | 7.2 | 5.2 | 4.4 |

| Nov 2020 | 4.3 | 4.9 | 6.2 | 4.8 | 4.4 |

| Dec 2020 | 5.1 | 5.6 | 7.0 | 5.5 | 4.6 |

| Jan 2021 | 7.6 | 8.1 | 9.7 | 8.0 | 7.0 |

| Feb 2021 | 9.5 | 10.1 | 11.7 | 9.7 | 8.7 |

| Mar 2021 | 12.3 | 12.5 | 14.3 | 12.0 | 10.7 |

| Apr 2021 | 13.8 | 14.0 | 15.9 | 13.5 | 12.0 |

| May 2021 | 18.6 | 18.1 | 20.2 | 17.4 | 15.5 |

| Jun 2021 | 22.5 | 21.7 | 24.0 | 20.2 | 18.4 |

| Jul 2021 | 22.8 | 21.9 | 24.0 | 20.3 | 19.4 |