An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

The Producer Price Index (PPI) measures the average change over time in selling prices received by domestic producers for their output. The main PPI measure of inflation, the Final Demand-Intermediate Demand (FD-ID) System, measures final demand inflation (price changes for goods, services, and construction sold to consumers, capital investment, government, and export buyers) and intermediate demand inflation (price changes for goods, services, and construction sold to businesses as inputs to production, excluding sales of capital investment). This issue of Beyond the Numbers describes PPI price movements in 2015.1

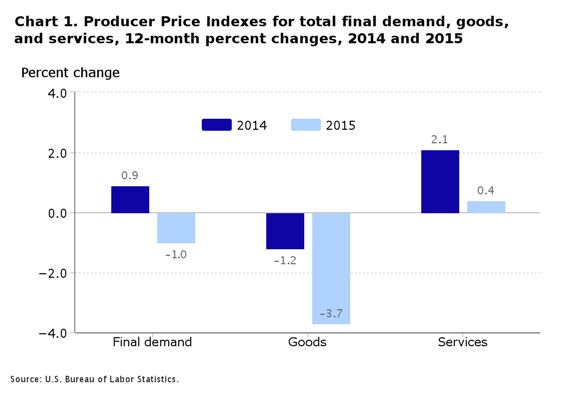

The PPI for final demand reversed course in 2015, falling 1.0 percent, compared with a 0.9-percent advance in 2014. In the goods sector, a sizeable downturn in prices for final demand foods in 2015 accounted for over half of the faster rate of decline in the index for final demand goods, which fell 3.7 percent after decreasing 1.2 percent in 2014. In addition, prices for final demand energy continued to drop, moving down at a steeper rate in 2015 than in the previous year. The index for final demand goods other than foods and energy was unchanged after rising in 2014.2 (See chart 1 and table 1.)

| Category | 2014 | 2015 |

|---|---|---|

| Final demand | 0.9 | -1.0 |

| Goods | -1.2 | -3.7 |

| Services | 2.1 | 0.4 |

| Index | 2014 | 2015 |

|---|---|---|

| Final demand | ||

| Total Final demand | 0.9 | -1.0 |

| Goods for final demand | -1.2 | -3.7 |

| Foods | 4.4 | -5.2 |

| Energy goods | -13.2 | -16.2 |

| Goods less foods and energy | 1.1 | 0.0 |

| Services for final demand | 2.1 | 0.4 |

| Trade services | 4.0 | 0.2 |

| Transportation and warehousing services | 0.8 | -3.4 |

| Services less trade, transportation, and warehousing | 1.4 | 1.0 |

| Construction for final demand | 2.2 | 1.8 |

| Intermediate demand, by type of commodity | ||

| Processed goods for intermediate demand | -2.6 | -6.4 |

| Processed foods and feeds | 3.0 | -9.2 |

| Processed energy goods | -12.9 | -16.5 |

| Processed materials less foods and energy | -0.1 | -3.6 |

| Unprocessed goods for intermediate demand | -8.7 | -25.0 |

| Unprocessed foodstuffs and feedstuffs | 2.9 | -18.8 |

| Unprocessed energy materials | -20.5 | -35.9 |

| Unprocessed nonfood materials less energy | -5.3 | -18.7 |

| Services for intermediate demand | 1.8 | 0.5 |

| Trade services for intermediate demand | 2.8 | -0.4 |

| Transportation and warehousing services for intermediate demand | 2.1 | -0.6 |

| Services less trade, transportation, and warehousing for intermediate demand | 1.5 | 0.8 |

| Construction for intermediate demand | 2.7 | 1.7 |

| Intermediate demand, by production flow | ||

| Stage 4 intermediate demand | 0.5 | -1.5 |

| Total goods inputs to stage 4 intermediate demand | -1.0 | -3.5 |

| Total services inputs to stage 4 intermediate demand | 2.1 | 0.7 |

| Stage 3 intermediate demand | 0.2 | -6.7 |

| Total goods inputs to stage 3 intermediate demand | -1.1 | -12.7 |

| Total services inputs to stage 3 intermediate demand | 1.8 | 0.6 |

| Stage 2 intermediate demand | -6.4 | -7.9 |

| Total goods inputs to stage 2 intermediate demand | -12.2 | -18.3 |

| Total services inputs to stage 2 intermediate demand | 1.7 | 0.8 |

| Stage 1 intermediate demand | -2.4 | -8.3 |

| Total goods inputs to stage 1 intermediate demand | -6.4 | -13.6 |

In the services sector, a smaller increase in the index for final demand trade services and a steep downturn in prices for final demand transportation and warehousing services resulted in substantially lower inflation for overall final demand services. (Trade indexes measure changes in margins received by wholesalers and retailers.3) The index for final demand services edged up 0.4 percent in 2015 following a 2.1-percent advance a year earlier. A downturn in the index for fuels and lubricants retailing and in prices for transportation of freight and mail, as well as larger declines in the index for airline passenger services, accounted for over half the slowing of the rate of increase in the index for final demand services.4 In addition, persistent weakness in prices for refined petroleum products were a major contributor to reduced inflation pressure further along the production and distribution chain.5

The index for final demand less foods, energy, and trade services edged up 0.3 percent in 2015, compared with a 1.3-percent advance in 2014. Historically, the indexes for food, energy, and trade services have exhibited greater short-term volatility than other components of the FD-ID system. As a result, PPI calculates a number of indexes tracking changes in prices for products excluding these potentially volatile components.6

As was the case within final demand, prices for intermediate demand goods fell more, while inflation slowed for intermediate demand services. The index for processed goods for intermediate demand decreased 6.4 percent in 2015 after moving down 2.6 percent in the preceding year, due to a downturn in prices for processed foods and feeds, along with larger declines for energy goods and processed core goods. Similar shifts in prices for unprocessed foodstuffs and feedstuffs, unprocessed energy materials, and unprocessed core goods led to a steeper decrease in the index for unprocessed goods for intermediate demand. Within intermediate demand services, the inflation rate slowed from 1.8 percent in 2014 to 0.5 percent in 2015, as the indexes for trade services and for transportation and warehousing services for intermediate demand turned down, while prices for services other than trade, transportation, and warehousing moved up at a slower rate than in 2014.

Foods. Prices for slaughter livestock dropped 25.7 percent in 2015 after climbing 17.9 percent in 2014, and the index for slaughter chickens fell 22.9 percent, compared with a 3.1-percent rise a year earlier. Prices for processed meats and poultry also fell following increases in 2014. The U.S. Department of Agriculture reported that total domestic beef production was little changed in 2015 at 23.7 billion pounds. However, in response to the rising value of the U.S. dollar, U.S. beef exports fell by 350 million pounds while imports jumped by 435 million pounds. Pork production surged 7.4 percent in 2015 to 24.5 billion pounds. Broiler chicken production rose 4.2 percent to 40.2 billion pounds, while exports of broiler chickens dropped 8.8 percent. Lower input costs, which were reflected by prepared animal feeds prices, falling 14.4 percent in 2015 and dropping 23.4 percent since 2012, also were a factor contributing to weaker selling prices for slaughter livestock and chickens, as well as, raw milk and dairy products.7

Energy. Prices for crude petroleum and natural gas decreased 43.3 percent and 46.5 percent, respectively, in 2015. The Energy Information Administration reported that for the 12 months ending October 2015, monthly U.S. field production of crude oil grew 2.6 percent to over 290.5 million barrels (on average 9.370 million barrels per day in October 2015). From October 2010 to October 2015, U.S. average monthly field production of crude oil surged by 67 percent. For 2015 through September, world crude oil production averaged 79.8 million barrels per day, 2.4 percent higher than a year earlier.8 In terms of demand for petroleum products, product supplied to the market (a proxy for petroleum product consumption) advanced 2.8 percent in 2015 based on a comparison of weekly product supplied for 2014 and 2015. Consumption of finished motor gasoline rose 3.3 percent, while consumption of distillate fuels, such as diesel and heating oil, inched up 0.8 percent.9 In the natural gas sector, gross withdrawals for January through October 2015 outpaced the same period in 2014 by 5.9 percent, while consumption increased 4.5 percent over the same period. Net injections of natural gas to underground storage also expanded. As of October 2015, the end of the traditional refilling season for natural gas inventory, total natural gas in underground storage totaled 8.301 billion cubic feet, a 4.6-percent increase compared with the preceding October.10 Abundant supplies and low prices for both crude petroleum and natural gas have reverberated through the entire energy market.11

Services. As mentioned previously, falling prices for energy goods were a major factor in the slowing rate of increase in prices for final demand services. Falling energy prices also contributed to lower inflation for business demand services. The indexes for transportation and warehousing services for intermediate (business) demand and for chemicals wholesaling turned down in 2015. In addition, lower farm and processed food prices contributed to smaller increases in the indexes for both the wholesaling and retailing of food and alcohol. Responding to a largely flat stock market in 2015, prices for portfolio management, investment banking, and deposit services moved up at slower rates in 2015 than in 2014, when equity markets provided better returns. The U.S. economy expanded at a 2.4 percent rate in 2015, the same rate as in 2014. These moderate rates of economic growth have left many service sector firms with little pricing power.12 For example, the PPIs for paper and plastics products wholesaling, management consulting services, and cable network advertising time sales fell in 2015 following advances in the preceding year.

Final demand services. In 2015, the downturn in the index for final demand was led by prices for final demand services, which advanced 0.4 percent after a 2.1-percent rise in 2014. Margins for final demand trade services accounted for two-thirds of the slowing rate of increase, moving up 0.2 percent after rising 4.0 percent a year earlier. Prices for final demand transportation and warehousing services turned down 3.4 percent in 2015 following a 0.8-percent advance in the previous year. The index for final demand services less trade, transportation, and warehousing increased less than in the previous year, rising 1.0 percent after moving up 1.4 percent in 2014.

Product detail. Within the index for final demand services, margins for fuels and lubricants retailing turned down 14.9 percent in 2015, compared with a 47.2-percent surge a year earlier. The indexes for truck transportation of freight and for securities brokerage, dealing, and investment advice also declined following advances in the preceding year. Prices for airline passenger services fell more than in 2014. The indexes for portfolio management and for machinery, equipment, parts, and supplies wholesaling rose less than in the preceding 12-month period. In contrast, prices for consumer loans (partial) turned up 0.5 percent in 2015 after falling 5.8 percent in the previous year. The index for health, beauty, and optical goods retailing also increased following a decrease in 2014. Prices for services related to securities brokerage and dealing advanced more than in the previous year.

Final demand goods. Prices for final demand goods fell 3.7 percent in 2015 following a 1.2-percent decline in the previous year. Over half of the faster rate of decrease is attributable to the index for final demand foods, which turned down 5.2 percent after rising 4.4 percent in 2014. Prices for final demand goods less foods and energy were unchanged, compared with a 1.1-percent advance a year earlier. The index for final demand energy dropped 16.2 percent subsequent to a 13.2-percent decline in 2014.

Product detail. Leading the faster rate of decrease in final demand goods prices, the index for meats turned down 17.3 percent in 2015 following a 15.9-percent jump in the preceding year. Prices for utility natural gas, electric power, processed poultry, and chicken eggs also declined after rising in 2014. The index for iron and steel scrap fell at a faster rate than in the prior year. Conversely, prices for motor vehicles turned up 2.8 percent in 2015 after edging down 0.1 percent in the previous year. The indexes for liquefied petroleum gas and corn decreased less than in 2014.

Processed goods for intermediate demand. The index for processed goods for intermediate demand dropped 6.4 percent in 2015, following a 2.6-percent decline in 2014. Sixty percent of the faster rate of decline in prices for processed goods for intermediate demand can be attributed to the index for processed materials less foods and energy, which moved down 3.6 percent in 2015, compared with a 0.1-percent decrease in the prior 12-month period. Prices for processed foods and feeds turned down 9.2 percent after advancing 3.0 percent in 2014. The index for processed energy goods decreased 16.5 percent after falling 12.9 percent in the previous year.

Product detail. Within the index for processed goods for intermediate demand, nearly 20 percent of the faster rate of decline can be traced to prices for steel mill products, which turned down 19.8 percent in 2015, after a 0.7-percent increase a year earlier. The indexes for meats, utility natural gas, plastic resins and materials, and ethanol also declined after moving up in 2014.13 Prices for diesel fuel fell more than in the preceding year. In contrast, the decrease in the index for lubricating oil base stocks slowed to 16.1 percent in 2015 from 36.1 percent in the previous 12-month period. Prices for primary basic organic chemicals also fell less than in 2014. The index for confectionery materials turned up after declining in the previous 12-month period.

Unprocessed goods for intermediate demand. The index for unprocessed goods for intermediate demand dropped 25.0 percent in 2015, after falling 8.7 percent in 2014. Over half of the faster rate of decline in prices for unprocessed goods for intermediate demand was the result of the index for unprocessed foodstuffs and feedstuffs, which turned down 18.8 percent in 2015, following a 2.9-percent advance a year earlier. Prices for unprocessed energy materials declined 35.9 percent after decreasing 20.5 percent in 2014. The index for unprocessed nonfood materials less energy fell 18.7 percent following a 5.3-percent decline in the previous year.

Product detail. Nearly half of the faster rate of decline in 2015 in the index for unprocessed goods for intermediate demand can be attributed to prices for slaughter cattle, which turned down 27.7 percent after rising 26.3 percent in the previous 12-month period. The indexes for natural gas, slaughter chickens, and nonferrous metals also fell after moving higher in 2014. Prices for crude petroleum and for iron and steel decreased more than in the preceding year. Conversely, the decline in the index for corn slowed to 1.6 percent in 2015 from 12.5 percent a year earlier. Prices for oilseeds also fell less than in the previous year, while the index for raw cotton turned up after decreasing in 2014.

Services for intermediate demand: In 2015, the index for services for intermediate demand rose 0.5 percent following a 1.8-percent advance in 2014. Forty percent of the slower rate of increase in prices for services for intermediate demand can be traced to margins for trade services for intermediate demand, which fell 0.4 percent in 2015, compared with a 2.8-percent increase in the prior 12-month period. The advance in the index for services less trade, transportation, and warehousing for intermediate demand slowed to 0.8 percent from 1.5 percent in 2014. The index for transportation and warehousing services for intermediate demand turned down 0.6 percent after increasing 2.1 percent in the previous year.

Product detail: Margins for paper and plastics products wholesaling turned down 3.5 percent in 2015 after a 7.6-percent advance in the previous year. The indexes securities brokerage, dealing, and investment advice; transportation of freight and mail; and fuels and lubricants retailing also declined after moving up in 2014. Prices for portfolio management rose less than they had in the prior year. In contrast, the increase in the index for services related to securities brokerage and dealing accelerated to 20.5 percent in 2015, from 2.6 percent in the prior year. Prices for business loans (partial) declined less in 2015, while the index for building materials, paint, and hardware wholesaling turned up after falling in 2014.

The production flow treatment of intermediate demand is a stage-based system of price indexes. The stage-based indexes can be used to study price transmission relationships between intermediate demand stages, and to final demand. The production flow treatment contains four main indexes: intermediate-demand stages 1 through 4. Indexes for the four stages were developed by assigning each industry in the economy to one of four stages of production, where industries assigned to the fourth stage primarily produce output consumed for final demand, industries in the third stage primarily produce output consumed by stage 4 industries, industries assigned to the second stage primarily produce output consumed by stage 3 industries, and industries assigned to the first stage produce output primarily consumed by stage 2 industries. The four stage-based intermediate demand indexes track price change for the net inputs consumed by industries assigned to each of the four stages. The stage 4 intermediate-demand index, for example, tracks price change for inputs consumed, not produced, by industries included in the fourth stage. Hence, this index measures price change in the inputs to production for industries that primarily produce final demand goods, services, and construction.

In 2015, prices in all four stages of intermediate demand by production flow were consistent with the downturn in final demand. The indexes for stage 4 and stage 3 intermediate demand both fell after rising in 2014. These stages were dominated by lower food prices, with total foods inputs to stage 4 intermediate demand declining 9.1 percent in 2015 following a 3.7-percent increase a year earlier, and total foods inputs to stage 3 dropping 20.4 percent after a 5.5-percent advance in 2014. Inputs to stage 2 intermediate demand decreased more in 2015 than in the prior year, and were heavily influenced by energy prices, with energy inputs to stage 2 intermediate demand falling 37.5 percent after a 24.9-percent decline in 2014. Inputs to stage 1 intermediate demand also moved down more in 2015, mainly due to prices for stage 1 goods inputs less food and energy, which decreased 10.5 percent after falling 7.2 percent in 2014.

Stage 4 intermediate demand: The index for stage 4 intermediate demand turned down 1.5 percent in 2015 after rising 0.5 percent in the previous 12-month period. Prices for total goods inputs to stage 4 intermediate demand fell 3.5 percent after declining 1.0 percent in 2014. The increase in the index for total services inputs to stage 4 intermediate demand slowed to 0.7 percent from 2.1 percent in the prior year. In 2015, prices for meats dropped 17.3 percent after advancing 15.9 percent a year earlier. Prices for securities brokerage, dealing, and investment advice; plastic products; and steel mill products also turned down after rising in 2014. The increase in the index for portfolio management slowed, while prices for diesel fuel declined more than in 2014. In contrast, the index for services related to securities brokerage and dealing jumped 20.5 percent in 2015, compared with a 2.6-percent rise in the preceding year. Prices for business loans (partial) and corn declined at slower rates than in 2014.

Stage 3 intermediate demand: The index for stage 3 intermediate demand turned down 6.7 percent in 2015 after rising 0.2 percent in the prior year. Prices for total goods inputs to stage 3 intermediate demand dropped 12.7 percent subsequent to a 1.1-percent decline a year earlier. The advance in the index for total services inputs for stage 3 intermediate demand slowed to 0.6 from 1.8 percent in 2014. Prices for slaughter cattle dropped 27.7 percent in 2015, following a 26.3-percent jump in the prior year. The indexes for slaughter chickens, steel mill products, asphalt, and transportation of freight and mail also turned down after moving up in 2014. Prices for jet fuel and raw milk fell more than in the prior year. In contrast, the index for services related to securities brokerage and dealing increased 20.5 percent following a 2.6-percent advance in 2014. Prices for slaughter turkeys also rose more than in the preceding year, while the index for business loans (partial) fell less than in 2014.

Stage 2 intermediate demand: The index for stage 2 intermediate demand declined 7.9 percent in 2015, following a 6.4-percent decrease in 2014. Prices for total goods inputs to stage 2 intermediate demand fell 18.3 percent after moving down 12.2 percent in the prior year. The index for total services inputs to stage 2 intermediate demand climbed 0.8 percent in 2015, compared with a 2.7-percent advance in the prior year. Prices for natural gas dropped 46.5 percent following a 4.5-percent rise in 2014. The indexes for plastic resins and materials; steel mill products; and securities brokerage, dealing, and investment advice also turned down after advancing a year earlier. Prices for crude petroleum and prepared animal feeds declined more than they did in 2014. In contrast, the increase in the index for services related to securities brokerage and dealing accelerated to 20.5 percent in 2015, from 2.6 percent in the previous 12-month period. Prices for liquefied petroleum gas fell less than in 2014, while the index for co-employment staffing services turned up in 2015.

Stage 1 intermediate demand: The index for stage 1 intermediate demand declined 8.3 percent in 2015, following a 2.4-percent decrease a year earlier. Prices for total goods inputs to stage 1 intermediate demand dropped 13.6 percent after moving down 6.4 percent in 2014. The index for total services inputs to stage 1 intermediate demand turned down 0.9 percent, following a 2.9-percent rise a year earlier. Prices for iron and steel scrap dropped 52.0 percent in 2015 after falling 16.9 percent in in the preceding 12-month period. Prices for diesel fuel also declined at a faster rate than in 2014. The indexes for nonferrous scrap, ethanol, natural gas, steel mill products, and fuels and lubricants retailing turned down after rising in the previous year. Conversely, the decrease in the index for business loans (partial) slowed to 5.7 percent in 2015, from 10.0 percent in the previous 12-month period. Prices for services related to securities brokerage and dealing advanced more, while prices for primary basic organic chemicals declined less than they did in 2014.

This Beyond the Numbers article was prepared by Joseph Kowal, Scott Sager, Lana Conforti, and Brian Hergt economists in the Producer Price Index Program. Email: ppi-info@bls.gov. Telephone: 202-691-7705.

Information in this article will be made available upon request to individuals with sensory impairments. Voice phone: (202) 691-5200. Federal Relay Service: 1-800-877-8339. The article is in the public domain and may be reproduced without permission.

Joseph Kowal, Scott Sager, Lana Conforti, and Brian Hergt, “Producer prices in 2015: Services inflation slows, goods prices continue to decrease ,” Beyond the Numbers: Prices & Spending, vol. 5 / no. 3 (U.S. Bureau of Labor Statistics, February 2016), https://www.bls.gov/opub/btn/volume-5/producer-prices-in-2015.htm

1 PPI 12-month percent changes for December 2015 will be finalized with the release of data on May 13, 2015. All PPI data are recalculated 4 months after original publication to reflect late reporting by survey respondents.

2 The Final Demand-Intermediate Demand (FD-ID) system was first introduced in January 2011 as a set of experimental indexes. With the release of data for January 2014, the FD-ID system replaced the Stage of Processing (SOP) system. Nearly all new FD-ID goods, services, and construction indexes provide historical data back to either November 2009 or April 2010, while the indexes for goods that correspond with the historical SOP indexes go back to the 1970s or earlier. For more information about the FD-ID system, see “A new, experimental system of indexes from the PPI program,” Monthly Labor Review, February 2011, https://www.bls.gov/opub/mlr/2011/02/art1full.pdf, or, visit the PPI FD-ID system webpage at https://www.bls.gov/ppi/fdidaggregation.htm.

3 PPIs for trade services measure changes in margins received by wholesalers and retailers. For more information see “Wholesale and retail Producer Price Indexes: margin prices,” Beyond the Numbers: Prices and Spending (U.S. Bureau of Labor Statistics, August 2012, vol. 1. No. 8, https://www.bls.gov/opub/btn/volume-1/pdf/wholesale-and-retail-producer-price-indexes-margin-prices.pdf.

4 For a detailed discussion of price transmission across stages of processing, see Jonathan Weinhagen, “An empirical analysis of price transmission by stage of processing,” Monthly Labor Review, November 2002, pp. 3–11, at https://www.bls.gov/opub/mlr/2002/11/art1full.pdf.

5 For a discussion of fuel surcharges and their influence on transportation prices, see “Current Price Topics: The Impact of Fuel Surcharges on the PPI,” Focus on Prices and Spending (U.S. Bureau of Labor Statistics, August 2011, https://www.bls.gov/opub/focus/volume2_number6/ppi_2_6.pdf.

6 Historically, PPIs for food and energy goods have exhibited greater short-term volatility than PPIs for goods other than food and energy. As a result, the program long ago introduced a number of indexes tracking changes in prices for goods excluding one or both of these potentially volatile components. For those who prefer it, this information has permitted data users to analyze movements in prices to the exclusion of potentially large movements in food and energy prices. With the transition from the SOP to the FD-ID system, the program continues to produce these indexes. In addition, with the FD-ID expansion that includes prices for many services, it has been observed that the indexes for wholesale and retail trade, which measure changes in margins, also are subject to potentially large short-term changes in prices. Consequently, to assist data users looking to exclude this volatility, the Producer Price Index calculates a number of indexes excluding prices for trade services. These indexes include final demand services less trade services and final demand less trade services. In addition, the program calculates an index for final demand less foods, energy, and trade services, removing all three potentially volatile components.

7 Livestock, Dairy, and Poultry Outlook, LDP-M-258, Dec. 15, 2015, U. S. Department of Agriculture, Economic Research Service, p. 22, http://www.ers.usda.gov/media/1959920/ldp-m-258.pdf.

8 This Week in Petroleum, U.S. Energy Information Administration, (U.S. Department of Energy, visited Jan. 19, 2016, on the Web at http://www.eia.gov/petroleum/weekly/.) Crude oil statistics for prices, reserves, production, refining, processing, and imports/exports are available online by accessing the Data tab and selecting from the available options. Data specific to U.S. crude oil field production are available at http://www.eia.gov/dnav/pet/hist/LeafHandler.ashx?n=PET&s=MCRFPUS1&f=M. Data specific to world crude oil production are available at www.eia.gov/totalenergy/data/monthly/pdf/sec11_5.pdf.

9 According to the Energy Information Administration, petroleum product supplied “Approximately represents consumption of petroleum products because it measures the disappearance of these products from primary sources, i.e., refineries, natural gas processing plants, blending plants, pipelines, and bulk terminals. In general, product supplied of each product in any given period is computed as follows: field production, plus refinery production, plus imports, plus unaccounted for crude oil, (plus net receipts when calculated on a PAD District basis), minus stock change, minus crude oil losses, minus refinery inputs, minus exports.” The data for petroleum product supplied cited in this article is available at http://www.eia.gov/dnav/pet/pet_cons_wpsup_k_w.htm.

10 Natural Gas Monthly, U.S. Energy Information Administration (U.S. Department of Energy, visited Jan. 19, 2016), http://www.eia.gov/naturalgas/monthly/. For data specific to natural gas production, select Table 1. Summary of natural gas supply and disposition in the United States, 2010–2015. For data specific to natural gas inventory, select Table 9. Underground natural gas storage by season. A pdf version of the entire report is available at http://www.eia.gov/naturalgas/monthly/archive/2015/2015_12/pdf/ngm_all.pdf.

11 The indexes for utility electric power, utility natural gas, and asphalt fell in 2015 after rising in 2014. Prices for gasoline, diesel fuel, jet fuel, and home heating oil exhibited substantial declines for the second consecutive calendar year.

12 Gross Domestic Product: Fourth Quarter and Annual 2015 (Advance Estimate), BEA 16–04, Bureau of Economic Analysis, Jan. 29, 2016, at www.bea.gov/newsreleases/national/gdp/2016/pdf/gdp4q15_adv.pdf, p. 6.

13 Commodities are often purchased by different types of buyers. As a result, a commodity is often included in several FD–ID indexes. For example, regular gasoline is commonly purchased for personal consumption, export, and government use—categories within final demand. The weight apportioned to business purchases of gasoline is reflected within the index for processed goods for intermediate demand. The PPI program publishes only one commodity index for regular gasoline, reflecting sales to all types of buyers, and this index is used in all FD–ID aggregations. In cases when buyer type is an important price-determining characteristic, indexes are often created on the basis of the specific type of buyer. For example, within the PPI category for loan services, separate indexes for consumer loans and business loans have been constructed.

Publish Date: Friday, February 26, 2016