An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

The Producer Price Index (PPI) measures the average change over time in the selling prices received by domestic producers for their output. The PPI provides measures of final demand (price changes for goods, services, and construction sold to consumers, capital investment buyers, government, and export) and intermediate demand (price changes for goods, services, and construction sold to businesses, excluding capital investment goods, as inputs to production). This issue of Beyond the Numbers describes price changes in PPIs throughout 2014. Falling energy prices and rising services prices were some of the top movers in 2014.

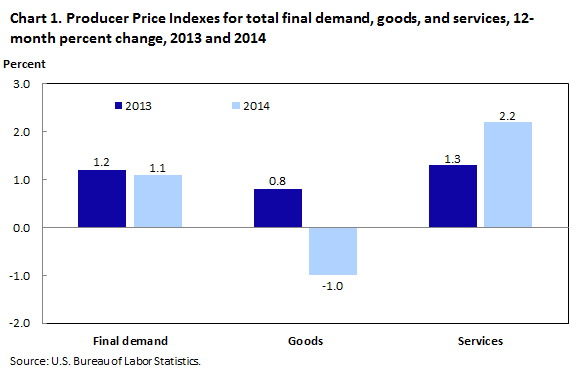

The PPI for final demand advanced 1.1 percent in 2014, little changed from a 1.2-percent increase in 2013. Led by a strong reversal in prices for final demand energy, the index for final demand goods fell 1.0 percent in 2014, following a 0.8-percent rise in 2013. The index for final demand construction moved up at a slower rate than it did in 2013, 2.1 percent compared with 3.2 percent. In contrast, because of an upturn in margins for final demand trade services, the index for overall final demand services increased 2.2 percent in 2014 after advancing 1.3 percent in the prior year.1 (See chart 1 and table 1.)

| Index | 2013 | 2014 |

|---|---|---|

| Final demand | ||

| Total final demand | 1.2 | 1.1 |

| Goods for final demand | 0.8 | -1.0 |

| Foods | -0.8 | 4.4 |

| Energy goods | 0.9 | -12.9 |

| Goods less foods and energy | 1.3 | 1.3 |

| Services for final demand | 1.3 | 2.2 |

| Trade services | -0.4 | 4.2 |

| Transportation and warehousing services | 2.0 | 0.5 |

| Services less trade, transportation, and warehousing | 2.0 | 1.4 |

| Construction for final demand | 3.2 | 2.1 |

| Intermediate demand, by type of commodity | ||

| Processed goods for intermediate demand | 0.1 | -2.2 |

| Processed foods and feeds | -2.6 | 3.1 |

| Processed energy goods | -1.2 | -12.4 |

| Processed materials less foods and energy | 0.7 | 0.3 |

| Unprocessed goods for intermediate demand | -1.9 | -8.1 |

| Unprocessed foodstuffs and feedstuffs | -6.2 | 2.8 |

| Unprocessed energy materials | 4.8 | -19.0 |

| Unprocessed nonfood materials less energy | -5.6 | -5.1 |

| Services for intermediate demand | 1.0 | 1.7 |

| Trade services for intermediate demand | -1.5 | 1.8 |

| Transportation and warehousing services for intermediate demand | 2.4 | 2.1 |

| Services less trade, transportation, and warehousing for intermediate demand | 1.5 | 1.6 |

| Construction for intermediate demand | 2.0 | 2.7 |

| Intermediate demand, by production flow | ||

| Stage-4 intermediate demand | 0.8 | 0.5 |

| Total goods inputs to stage-4 intermediate demand | 0.4 | -0.9 |

| Total services inputs to stage-4 intermediate demand | 1.3 | 2.0 |

| Stage-3 intermediate demand | 0.5 | 0.4 |

| Total goods inputs to stage-3 intermediate demand | 0.3 | -0.9 |

| Total services inputs to stage-3 intermediate demand | 1.0 | 1.8 |

| Stage-2 intermediate demand | -0.2 | -5.7 |

| Total goods inputs to stage-2 intermediate demand | -0.3 | -11.1 |

| Total services inputs to stage-2 intermediate demand | -0.1 | 1.5 |

| Stage-1 intermediate demand | 0.2 | -2.0 |

| Total goods inputs to stage-1 intermediate demand | -1.0 | -5.4 |

| Total services inputs to stage-1 intermediate demand | 2.0 | 2.6 |

Within intermediate demand, falling prices for processed energy materials such as gasoline and diesel fuel led the downturn in the index for processed goods, which decreased 2.2 percent in 2014 after inching up 0.1 percent a year earlier. Similarly, a sharp drop in crude petroleum prices drove the steeper rate of decline in the index for unprocessed goods–8.1 percent, compared with a 1.9-percent decrease in 2013. Similar to final demand, an upturn in the index for intermediate demand trade services led the accelerated advance in prices for overall services for intermediate demand, which moved up 1.7 percent in 2014 after advancing 1.0 percent in 2013.

Crude petroleum and refined petroleum products. The petroleum sector in 2014 was led by gains in extraction of crude oil, as well as production and stockpiles of refined petroleum products. United States crude oil production averaged 14.2 million barrels per day in September 2014, 10.5 percent above its level a year earlier. Similarly, Canadian crude oil production increased 13.3 percent, to 4.6 million barrels per day over the same period. Worldwide, crude petroleum production rose 3.6 percent, to 93.5 million barrels per day from September 2013 to September 2014.2 Crude oil inputs to U.S. refineries averaged 16.4 million barrels per day in December 2014, 1.7 percent higher than their December 2013 level. Production of finished motor gasoline closed 2014 averaging 9.7 million barrels per day, a 5.0-percent increase from the previous December. Similar increases also occurred in jet fuel and diesel fuel production.3 U.S. stockpiles of crude oil grew 2.0 percent in 2014, while stockpiles of refined petroleum products such as total motor gasoline and distillate fuels (diesel and heating oil) increased 1.5 percent and 1.4 percent, respectively.

Services. Within both final demand and intermediate demand, the main source of higher inflation in 2014 compared with 2013 was higher margins for trade services (the difference between the prices wholesalers and retailers pay for goods and the prices at which they sell those goods). Margins for fuels and lubricants retailing surged 57.2 percent in 2014 after dropping 19.0 percent in the preceding year. Large over-the-month increases in retail margins for fuels and lubricants occurred in May, July, October, and December. In each of these months, refinery prices for gasoline fell, but retail prices moved down at slower rates, or even increased slightly. These divergent price shifts between production and distribution suggest wholesale-and retail-selling prices may deviate considerably from acquisition costs in the short run, during periods of falling prices. In contrast, food distributors consistently passed forward rising factory prices for food products. The PPI for final demand foods climbed 4.4 percent in 2014, primarily because of rising factory-gate prices for meats, processed poultry, and fluid milk products. The PPI for food and alcohol wholesaling turned up in 2014, while margins for food and alcohol retailing rose at a much faster rate than they did in 2013.

Final-demand goods. In 2014, the slower rate of increase in the index for final demand can be traced to prices for final demand goods, which turned down 1.0 percent after climbing 0.8 percent in 2013. The decrease in the index for final demand goods is primarily attributable to prices for final demand energy, which dropped 12.9 percent in 2014 after rising 0.9 percent a year earlier. Conversely, the index for final demand foods turned up 4.4 percent, following a 0.8-percent decline the previous year. Prices for final demand goods less foods and energy advanced 1.3 percent; the same rate as in 2013.

Product detail. Within the index for final demand goods, prices for gasoline dropped 27.5 percent in 2014 after moving down 0.8 percent in the previous year. The index for diesel fuel also decreased more than it had in 2013. Prices for home heating oil and liquefied petroleum gas turned down after rising in the previous year. In contrast, the rise in the index for meats accelerated to 15.9 percent in 2014 from 2.0 percent a year earlier. The index for pharmaceutical preparations also increased at a faster rate than it did in 2013.

Final-demand services. The index for final demand services advanced 2.2 percent in 2014 after a 1.3-percent rise in 2013. Margins for final demand trade services led the faster rate of increase, turning up 4.2 percent after declining 0.4 percent a year earlier. Conversely, prices for final demand transportation and warehousing services rose 0.5 percent, and the index for final demand services less trade, transportation, and warehousing climbed 1.4 percent; both of which advanced 2.0 percent in 2013.

Services detail. The index for fuels and lubricants retailing surged 57.2 percent in 2014, compared with a 19.0-percent drop the previous year. Margins for food wholesaling also turned up after falling in 2013. The indexes for food and alcohol retailing and for machinery, equipment, parts, and supplies wholesaling advanced at faster rates than they had in the preceding year. In contrast, the rise in the index for hospital outpatient care slowed to 1.3 percent in 2014 from 4.2 percent in the previous year. Prices for airline passenger services turned down after rising in 2013.

Intermediate demand includes goods, services, and maintenance and repair construction sold to businesses, excluding capital investment. BLS publishes two parallel treatments of intermediate demand, each constructed from the identical set of commodity price indexes. One treatment organizes commodities according to their type, and the other organizes commodities in accordance with a stage-based, production flow model.

Processed goods for intermediate demand. The index for processed goods for intermediate demand moved down 2.2 percent in 2014, following a 0.1-percent advance in 2013. The index for processed energy goods dropped 12.4 percent in 2014, compared with a 1.2-percent decline in the prior 12-month period. Price increases for processed materials less foods and energy slowed to 0.3 percent from 0.7 percent in 2013. Conversely, the index for processed foods and feeds turned up 3.1 percent in 2014 after decreasing 2.6 percent the previous year.

Product detail. Within the index for processed goods for intermediate demand, prices for diesel fuel fell 26.1 percent in 2014 subsequent to a 0.9-percent decrease a year earlier. The indexes for gasoline, primary basic organic chemicals, and lubricating oil base stocks also declined more than they had in 2013. In contrast, prices for meats surged 15.9 percent in 2014, following a 2.0-percent rise in the previous 12-month period. The index for industrial electric power turned up after falling in 2013.

Unprocessed goods for intermediate demand. Prices for unprocessed goods for intermediate demand dropped 8.1 percent in 2014, after decreasing 1.9 percent in 2013. The index for unprocessed energy materials fell 19.0 percent in 2014, following a 4.8-percent advance a year earlier. This drop boosted the faster rate of decline among unprocessed goods for intermediate demand. Conversely, prices for unprocessed foodstuffs and feedstuffs turned up 2.8 percent after decreasing 6.2 percent in 2013. The decrease in the index for unprocessed nonfood materials less energy slowed to 5.1 percent in 2014 from 5.6 percent in the previous year.

Product detail. Leading the faster rate of decline in 2014 in the index for unprocessed goods for intermediate demand, prices for crude petroleum fell 37.1 percent, compared with a 7.1-percent advance in the previous 12-month period. The indexes for iron and steel scrap and raw milk also turned down in 2014 after rising in 2013. Oilseeds prices fell more than in the previous year. In contrast, the slaughter cattle index surged 26.3 percent in 2014, following a 6.0-percent rise a year earlier. Prices for grains fell less than they had in 2013.

Services for intermediate demand: In 2014, the index for services for intermediate demand rose 1.7 percent, after moving up 1.0 percent in 2013. Over 80 percent of this acceleration can be traced to prices for trade services for intermediate demand, which turned up 1.8 percent subsequent to a 1.5-percent decline in the previous year. The index for services less trade, transportation, and warehousing for intermediate demand advanced 1.6 percent in 2014, following a 1.5-percent rise in the previous year. Conversely, price advances for transportation and warehousing services for intermediate demand slowed to 2.1 percent from 2.4 percent in 2013.

Commodity detail: In 2014, nearly 40 percent of the acceleration in the index for services for intermediate demand can be attributed to margins for paper and plastics products wholesaling, which moved up 3.8 percent in 2014, following an 11.9-percent decline in 2013. The indexes for food wholesaling and for fuels and lubricants retailing also turned up in 2014. Margins for metals, minerals, and ores wholesaling declined less than they did in 2013. In contrast, prices for airline passenger services turned down 1.8 percent in 2014 after rising 5.0 percent in the previous year. The index for business loans (partial) fell more than it did in 2013.

Stage 4 intermediate demand. The stage 4 intermediate demand index measures price changes for products purchased by industries that primarily produce output sold to final demand. The index for stage 4 intermediate demand advanced 0.5 percent in 2014 after rising 0.8 percent in 2013. In 2014, a 2.0-percent increase in prices for total services inputs to stage 4 intermediate demand outweighed a 0.9-percent-decline in the index for total goods inputs to stage 4 intermediate demand. Higher prices for portfolio management; meats; concrete products; and machinery, equipment, parts, and supplies wholesaling outweighed declines in the indexes for gasoline and diesel fuel.

Stage 3 intermediate demand. The stage 3 intermediate demand index measures price changes for products purchased by industries that primarily produce output sold to industries classified in stage 4. The index for stage 3 intermediate demand rose 0.4 percent in 2014 subsequent to a 0.5-percent increase a year earlier. In 2014, a 1.8-percent advance in prices for total services inputs to stage 3 intermediate demand outweighed a 0.9-percent decrease in the index for total goods inputs to stage 3 intermediate demand. Advances in the indexes for transportation of freight and mail, slaughter cattle, industrial electric power, and thermoplastic resins and materials outweighed lower prices for gasoline and diesel fuel.

Stage 2 intermediate demand. The stage 2 intermediate demand index measures price changes for products purchased by industries that primarily produce output sold to industries classified in stage 3. In 2014, the index for stage 2 intermediate demand fell 5.7 percent, following a 0.2-percent decline in 2013. Prices for total goods inputs to stage 2 intermediate demand dropped 11.1 percent, compared with a 0.3-percent decrease a year earlier. In contrast, the index for total services inputs to stage 2 intermediate demand rose 1.5 percent subsequent to a 0.1-percent decline in the prior year. In 2014, the index for crude petroleum sank 37.1 percent in 2014 after rising 7.1 percent in 2013. Prices for liquefied petroleum gas also turned down in 2014. The indexes for primary basic organic chemicals and business loans (partial) fell more than they had in 2013. Conversely, margins for paper and plastics products wholesaling advanced 3.8 percent in 2014, following an 11.9-percent decline a year earlier. Prices for corn fell less than they had in 2013.

Stage 1 intermediate demand. The stage 1 intermediate demand index measures price changes for products purchased by industries that primarily produce output sold to industries classified in stage 2. The index for stage 1 intermediate demand moved down 2.0 percent in 2014, compared with a 0.2-percent advance in 2013. Prices for total goods inputs to stage 1 intermediate demand fell 5.4 percent after declining 1.0 percent a year earlier. Conversely, the index for total services inputs to stage 1 intermediate demand rose 2.6 percent, following a 2.0-percent increase in 2013. Leading the downturn in prices for stage 1 intermediate demand, the index for primary basic organic chemicals dropped 19.2 percent in 2014, compared with a 1.5-percent decrease in the prior year. Prices for gasoline also fell more than they had in 2013. The index for carbon steel scrap turned down in 2014, while prices for portfolio management rose less than in 2013. In contrast, the decline in margins for metals, minerals, and ores wholesaling slowed to 2.8 percent from 9.9 percent in the previous year. The index for electric power advanced more in 2014 than in the previous year, while margins for paper and plastics products wholesaling turned up after falling in 2013.

This Beyond the Numbers article was prepared by Joseph Kowal, Lana Borgie, Brian Hergt, and Antonio Lombardozzi, economists in the Producer Price Index Program. Email: ppi-info@bls.gov Telephone: 202-691-7705.

Information in this article will be made available upon request to individuals with sensory impairments. Voice phone: (202) 691-5200. Federal Relay Service: 1-800-877-8339. The article is in the public domain and may be reproduced without permission.

Joseph Kowal, Lana Borgie, Brian Hergt, and Antonio Lombardozzi, “Producer inflation in 2014: energy prices drop but prices for services advance ,” Beyond the Numbers: Prices & Spending, vol. 4 / no. 3 (U.S. Bureau of Labor Statistics, February 2015), https://www.bls.gov/opub/btn/volume-4/producer-inflation-in-2014-energy-prices-drop-but-prices-for-services-advance.htm

1 The Final Demand-Intermediate Demand (FD–ID) system was first introduced in January 2011 as a set of experimental indexes. With the release of January 2014 data, FD–ID replaced the Stage of Processing (SOP) indexes. Nearly all new FD–ID goods, services, and construction indexes provide historical data back to either November 2009 or April 2010, and the indexes for goods that correspond with the historical SOP indexes go back to the 1970s or earlier. For more information about the FD–ID system, see “A new, experimental system of indexes from the PPI program,” Monthly Labor Review, February 2011, https://www.bls.gov/opub/mlr/2011/02/art1full.pdf; or Producer price indexes: PPI Final Demand–Intermediate Demand (FD–ID) aggregation system (U.S. Bureau of Labor Statistics, February 3, 2014), https://www.bls.gov/ppi/fdidaggregation.htm.

Also, for more detail about overall PPI methodology, see “Producer Prices,” BLS Handbook of Methods (U.S. Bureau of Labor Statistics), chap. 14, https://www.bls.gov/opub/hom/pdf/homch14.pdf.

2 United States, Canadian, and Worldwide production figures were downloaded from the Energy Information Administration website (http://www.eia.gov/), Geography/Countries/Data/Petroleum & Other Liquids/Production/Monthly & Quarterly (http://www.eia.gov/cfapps/ipdbproject/IEDIndex3.cfm?tid=50&pid=53&aid=1).

3 Weekly Petroleum Status Report, DOE/EIA-0208(2014-52), U.S. Energy Information Administration, (U.S. Department of Energy, December 31, 2014. http://www.eia.gov/petroleum/supply/weekly/archive/2014/2014_12_31/pdf/wpsrall.pdf. Data for crude oil inputs to refineries are available in table 2, on page 2. For data on crude oil and refined petroleum products stockpiles, see tables 4-6 and figures 1-6 on pages 4-12.

Publish Date: Monday, February 23, 2015