An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

Crossref 0

Consumer Expenditure Survey Methods Symposium and Microdata Users’ Workshop, July 17–20, 2018, Monthly Labor Review, 2019.

Consumer Expenditure Surveys Methods Symposium and Microdata Users’ Workshop, July 12–15, 2016, Monthly Labor Review, 2017.

The Consumer Expenditure Survey redesign initiative, Monthly Labor Review, 2016.

A Consumption-Based Definition of the Middle Class, Social Indicators Research, 2022.

Spending Response to the Expanded Child Tax Credit: An Analysis Using United States Consumer Expenditure Survey Data, Review of Income and Wealth, 2026.

Nonresponse is a common problem in household surveys, including the Consumer Expenditure Survey (CE). Methods to adjust for this problem have been in place for several years for many key items collected in the CE, including expenditures and income. Besides income, another important variable in analyzing expenditure patterns is taxes, because consumers presumably make expenditure and savings decisions based on after-tax income. However, before the data collected in 2013 were published, no mechanism was in place to adjust for nonresponse to tax questions. Data collection then changed in 2013 when TAXSIM, a model developed by the National Bureau of Economic Research, was introduced into the production process. The improvement in data quality was immediately evident: The percentage of consumer units for which tax data are available, along with average tax values calculated, increased substantially. In addition, levels of savings, computed as after-tax income less total expenditures, fell as expected. These results are observed for the population as a whole and for demographic groups within the population. This article includes details of the TAXSIM model and additional examples of how data quality improved because of its use in processing.

The Consumer Expenditure Survey (CE) collects information on expenditures, income, assets, liabilities, and taxes. Nonresponse is a concern in all these categories, and methods to adjust expenditures for nonresponse have been in place since the 1980s when the survey began collecting data regularly.1 In addition, since the publication of the 2004 data, the CE program has imputed income in cases in which respondents reported receipt, but not values, for sources of income. However, the tax reporting problem remained: CE participants were asked whether any member of their households paid taxes during the last 12 months besides those withheld from earnings and, if so, the amount paid.2 (For details on the selection of households participating in the CE, see chapter 16 of the BLS Handbook of Methods.3) If they did not know or refused to answer, the missing value was treated as if the participants reported it to be $0. As a result, average annual taxes in CE publications accounted for too small a share of income, a problem which was exacerbated when income imputation was introduced, as described later in this article.

However, starting with the published 2013 data, the income tax data have improved dramatically. These results are no longer published on the basis of responses from consumers who were directly asked how much they paid in taxes during the last 12 months. Instead, the CE estimates income taxes of all types using the TAXSIM model from the National Bureau of Economic Research (NBER). Researchers are increasingly looking at before- and after-tax income, along with expenditures, to examine income inequality and the economic well-being of people in the United States.4 The changes described in this article increase the CE value for this type of research. This article describes TAXSIM and demonstrates how much its use has improved CE data quality.

For most consumers who are asked, “During the last 12 months, did you or any member of your household PAY any federal income tax in addition to that withheld from earnings?” the answer is straightforward: “Yes” or “No.” However, when those who answer “Yes” are then asked, “What was the total amount paid by ALL household members?” the answer is not so straightforward. For example, the respondent is answering for all household members and may not have complete information for the others. Nevertheless, having federal income tax information is important when consumer expenditures are analyzed because consumers presumably make decisions based on take-home pay, and federal income taxes are both nondiscretionary and likely to account for a large share of a worker’s paycheck. Furthermore, other income taxes, such as state and local taxes, further increase the share that is removed from pay. Taxes affect the consumer’s ability to not only purchase goods and services but also save for future purchases, whether they are discrete (e.g., a new appliance, vehicle, or home), ongoing for a fixed time (e.g., college education), or permanent” (e.g., retirement). Therefore, having an accurate estimate of taxes paid is as important as having an accurate estimate of pretax income in analyzing consumer spending patterns.

Like all major surveys, the CE is subject to nonresponse and underreporting. The respondent often does not know or is unwilling to answer detailed questions about income and taxes.5 In the past, efforts to adjust for income nonresponse included publishing results for “complete” income reporters only. In general, consumer units6 for which the reference person7 reported at least one major income source were considered complete income reporters,8 regardless of whether or not they reported values for all sources for which they reported receipt. For example, the reference person could report a small amount of wage and salary income and be considered a “complete” reporter, even if substantial values for self-employment income, pension benefits, or other sources remained unreported for the reference person or others in the consumer unit. In addition, because the definition of reference person can be arbitrary in consumer units with more than one member (e.g., a husband and wife), the CE could define two consumer units with identical reporting patterns and demographics differently if the wife was the reference person in one case and the husband in the other. As noted, these definitions were supplanted when income imputation was introduced, which occurred with publishing of 2004 CE data. In this process, missing values for income are replaced with those estimated with the use of characteristics of the consumer unit or its members. For example, if the respondent reports that a member of the consumer unit worked for a wage or salary in the past year, but not the amount received, then that member’s age, occupation, and other characteristics are used in the imputation process.

However, no attempt to adjust taxes had ever occurred. That is, no “complete tax reporter” category, imputation, or other mechanism was in place to mitigate the problems of nonresponse. Furthermore, while high tax-withholding amounts were edited in processing, some reports of low tax values were unedited, even if they made no sense or were almost certainly inaccurate. For example, a respondent with income higher than the lowest income tax reporting threshold could report $0 or even negative income taxes, because the member received a refund. If a respondent is issued a refund because of an overpayment, the refund is presumably less than the total paid. Therefore, even in cases in which a refund is correctly reported, the respondent should report taxes paid as positive values.9

In all these cases—nonresponse or $0 reported—the tax value was treated in the survey as $0. Hence, the average amount of taxes paid was seriously underestimated. To understand how much, consider that only 54 percent of CE participants who reported expenditures in 2012 reported a value for taxes they paid during the last 12 months; the rest (46 percent) mostly did not know the value or refused to provide it. (Those who reported that they did not pay taxes are also included in the 46 percent.) This figure varied widely by demographic. For example, only 45 percent of single persons reported paying taxes, compared with 59 percent of husband–wife-only families, or husbands and wives with their children (and no others) living with them. In addition, only 67 percent of those in the highest quintile reported paying taxes.

Furthermore, as noted previously, these problems were exacerbated when income imputation was introduced. To illustrate, consider consumers who report an income of at least $70,000 before taxes. These consumers by definition not only report substantial income even before any additional income sources are imputed, but on average, they also certainly owe a substantial share of that income in federal taxes alone. Although not directly comparable, data from the Internal Revenue Service show that federal taxes accounted for over 21 percent of adjusted gross income (AGI) for those reporting at least $75,000 in AGI for either 2003 or 2004.10 Nevertheless, in 2003, federal taxes accounted for less than 5 percent of income before taxes for consumer units in this group. Moreover, in 2004, the share dropped almost a full point, to under 4 percent. This percentage drop is due almost entirely to a fall in taxes reported: Because of imputation, income for this group rose by four-tenths of 1 percent (from $117,960 to $118,480); however, reported federal taxes decreased by nearly 16 percent (from $5,448 to $4,589).11 Even when state, local, and other taxes were added, total taxes accounted for less than 6 percent of total income before taxes ($7,204) in 2003 and 5 percent ($6,217) in 2004, after dropping 14 percent over these 2 years.

So how can the CE get more accurate tax data even if respondents do not know or do not want to answer questions about their tax liabilities? TAXSIM can help resolve this concern.

According to Feenberg and Coutts, “‘TAXSIM’ refers to a collection of programs and data sets implementing a microsimulation model of the U.S. federal and state income tax systems.”12 The TAXSIM model uses information from survey data to estimate tax liabilities. Using data inputs from the CE, including location, marital status, number of dependents, imputed income, homeownership, mortgage interest, property taxes, medical expenses over the Internal Revenue Service threshold, and charitable gifts, the TAXSIM model estimates tax liabilities for both federal and state. For those interested in estimating their own tax liabilities, the TAXSIM tool is available online.13

An important note is that the CE program began estimating taxes in the second quarter of 2013. Because of the survey design, most (but not all) consumer units were subject to the new tax estimation model in 2013. Those not subject to the new model have recorded tax values from the old “as reported” method. In 2014, CE program will estimate tax liabilities for all consumer units.

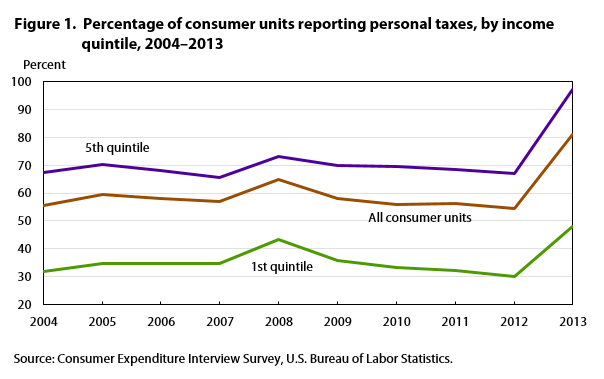

As noted previously, of CE participants who reported having expenditures in 2012, only 54 percent reported that they or members of their consumer unit paid any taxes during the last 12 months. This response rate varied little at least since 2004, except for a temporary increase in 2008, which was due to the distribution of federal economic stimulus payments (tax rebates) that year.14 However, the results for 2013, which include data estimated with TAXSIM, show the percentage of all consumer units for which tax values are available increased dramatically to 81 percent (figure 1).

| Quintile | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|---|---|

| 1st | 31.95 | 34.86 | 34.72 | 34.64 | 43.42 | 35.72 | 33.36 | 32.13 | 29.85 | 4.008 |

| 2nd | 52.84 | 58.09 | 55.43 | 54.86 | 63.41 | 54.83 | 51.13 | 51.94 | 51.04 | 72.10 |

| 3rd | 61.97 | 66.34 | 64.12 | 63.12 | 70.40 | 62.59 | 60.31 | 61.37 | 59.33 | 91.36 |

| 4th | 64.21 | 67.85 | 67.95 | 67.03 | 73.71 | 68.08 | 65.32 | 66.98 | 65.04 | 96.56 |

| 5th | 67.22 | 70.19 | 68.21 | 65.72 | 73.13 | 69.78 | 69.41 | 68.59 | 66.89 | 97.16 |

| All consumer units | 55.64 | 59.48 | 58.09 | 57.08 | 64.82 | 58.20 | 55.91 | 56.21 | 54.42 | 81.04 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||||||||||

An increase in the percentage of consumer units with tax data occurred across all income quintiles (figure 1). Less than one-third of the lowest quintile (29.9 percent) reported personal tax data in 2012, whereas nearly half (48.0 percent) had data assigned to them through TAXSIM in 2013. For the highest quintile, the number jumped from two-thirds (66.9 percent) in 2012 to nearly all (97.2 percent) in 2013.

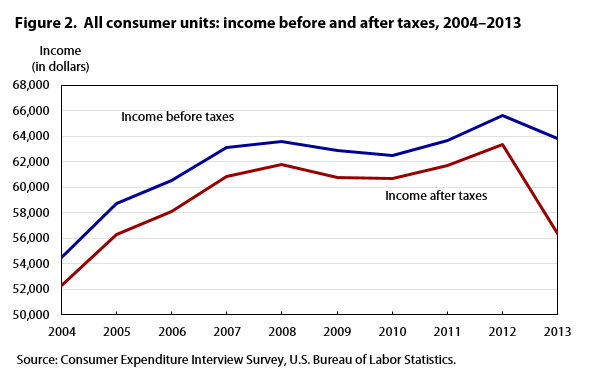

| Year | Income before taxes | Income after taxes |

|---|---|---|

| 2004 | $54,453 | $52,287 |

| 2005 | $58,712 | $56,304 |

| 2006 | $60,533 | $58,101 |

| 2007 | $63,091 | $60,858 |

| 2008 | $63,563 | $61,774 |

| 2009 | $62,857 | $60,753 |

| 2010 | $62,481 | $60,712 |

| 2011 | $63,685 | $61,673 |

| 2012 | $65,596 | $63,370 |

| 2013 | $63,784 | $56,352 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||

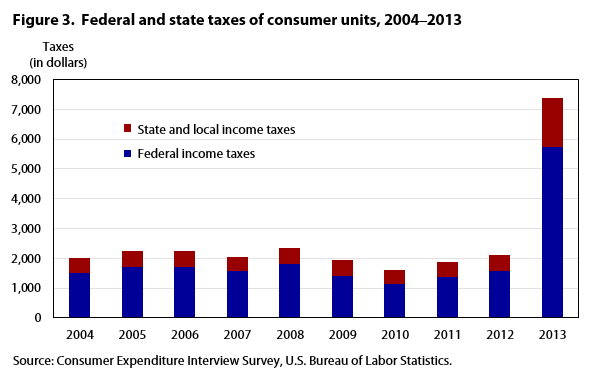

Similarly, in 2012, average income before taxes was $65,596, while income after taxes was $63,370, a difference of $2,226 (figure 2). In 2013, average income before taxes was $63,784, while income after taxes was $56,352, a difference of $7,432 after CE implemented the TAXSIM model. Thus, although income before taxes fell slightly (2.8 percent),15 total taxes more than tripled (rising 234 percent). The increase in total taxes resulted from substantial increases in federal taxes (266 percent), and state, local, and other taxes (210 percent), both of which more than tripled from 2012 to 2013 (figure 3). For researchers interested in income after taxes, also called “disposable income,” these new data are more accurate.

| Year | Federal income taxes (dollars) | State and local income taxes (dollars) |

|---|---|---|

| 2004 | 1,519 | 472 |

| 2005 | 1,696 | 534 |

| 2006 | 1,711 | 519 |

| 2007 | 1,569 | 468 |

| 2008 | 1,817 | 542 |

| 2009 | 1,404 | 524 |

| 2010 | 1,136 | 482 |

| 2011 | 1,370 | 505 |

| 2012 | 1,568 | 526 |

| 2013 | 5,743 | 1,629 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||

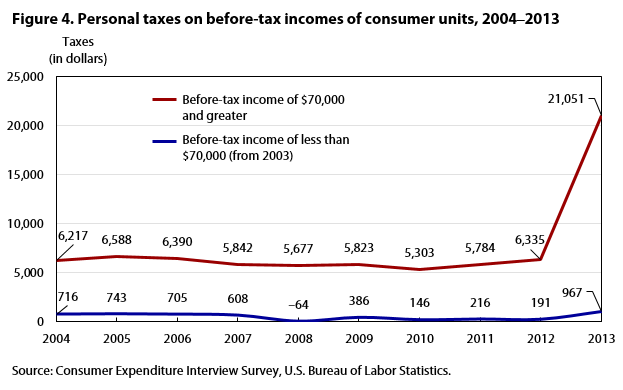

| Year | Before-tax income of $70,000 and greater | Before-tax income of less than $70,000 (from 2003) |

|---|---|---|

| 2004 | $6,217 | $716 |

| 2005 | $6,588 | $743 |

| 2006 | $6,390 | $705 |

| 2007 | $5,842 | $608 |

| 2008 | $5,677 | –$64 |

| 2009 | $5,823 | $386 |

| 2010 | $5,303 | $146 |

| 2011 | $5,784 | $216 |

| 2012 | $6,335 | $191 |

| 2013 | $21,051 | $967 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||

Although consumer units with higher incomes had larger increases in personal taxes in dollars than consumer units with lower incomes (figure 4), they did not have larger increases in percentages. In 2012, consumer units with before-tax income of $70,000 and greater reported paying $6,335 in personal taxes. In 2013, TAXSIM estimated that consumer units with a before-tax income of $70,000 and greater had an estimated tax liability of $21,051, an increase of $14,716, or 232 percent. In contrast, consumer units with before-tax income of less than $70,000 reported $191 in personal taxes in 2012 and had an estimated average tax liability of $967 in 2013, an increase of $776, or 406 percent.16 Furthermore, in 2012, federal taxes, as reported, accounted for 4.6 percent of income before taxes for the high income group ($70,000 and greater), with state, local, and other taxes accounting for an added 1.5 percent. However, in 2013, federal taxes were estimated to account for 12.7 percent, with state and local to now account for 3.3 percent.

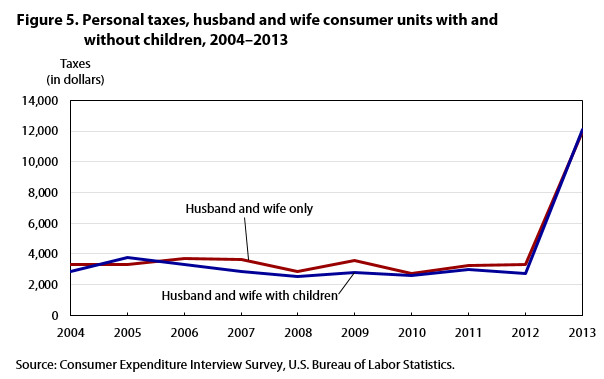

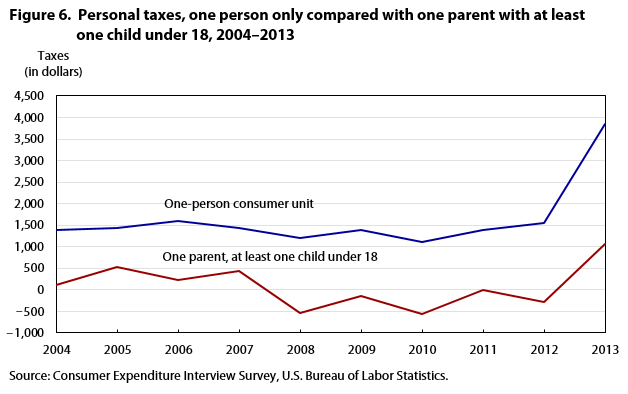

Interestingly, marital status is more important than parental status in determining similarity of outcome. This detail is notable because the presence of children usually means the tax filer can claim dependents and thereby reduce the amount of taxes owed. However, married couples with and without children (figure 5) are more similar to each other than married couples without children are to single persons (figure 6) or married couples with children are to single parents (figure 6).

| Year | Husband and wife only | Husband and wife with children |

|---|---|---|

| 2004 | $3,326 | $2,881 |

| 2005 | $3,338 | $3,780 |

| 2006 | $3,682 | $3,287 |

| 2007 | $3,629 | $2,826 |

| 2008 | $2,855 | $2,538 |

| 2009 | $3,560 | $2,813 |

| 2010 | $2,708 | $2,603 |

| 2011 | $3,216 | $2,976 |

| 2012 | $3,297 | $2,716 |

| 2013 | $11,982 | $12,087 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||

Starting with married couples, the results of TAXSIM are dramatic. Note that between 2004 and 2012, reported personal taxes never reached $4,000 for married couples either with children or without. However, in 2013, TAXSIM estimates about $12,000 on average for each group.

| Year | One-person consumer unit | One parent, at least one child under 18 |

|---|---|---|

| 2004 | $1,383 | $103 |

| 2005 | $1,425 | $519 |

| 2006 | $1,602 | $220 |

| 2007 | $1,423 | $445 |

| 2008 | $1,205 | –$545 |

| 2009 | $1,395 | –$148 |

| 2010 | $1,117 | –$562 |

| 2011 | $1,378 | –$11 |

| 2012 | $1,546 | –$281 |

| 2013 | $3,838 | $1,056 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||

Single persons and single parents follow trends similar to each other from 2004 through 2012 and, as with other groups, show a large increase in average taxes for 2013. More interesting is that reported taxes were negative for single parents for each year from 2008 through 2012. As noted previously, in 2008, the first year in which this phenomenon is observed, the tax rebate could have resulted in negative taxes being paid, at least in some consumer units. However, after 2008, the explanation is not so apparent. Although no information on the Earned Income Tax Credit was directly collected until 2013, coincident with the implementation of TAXSIM, single parents who received this credit may have reported it as a refund before 2013. Or single parents may have been more inclined to report refunds, but not taxes paid, resulting in a negative value. Regardless, with TAXSIM implemented, single parents on average were estimated to have paid more than $1,000 in taxes, substantially more than even the smallest negative report would imply.

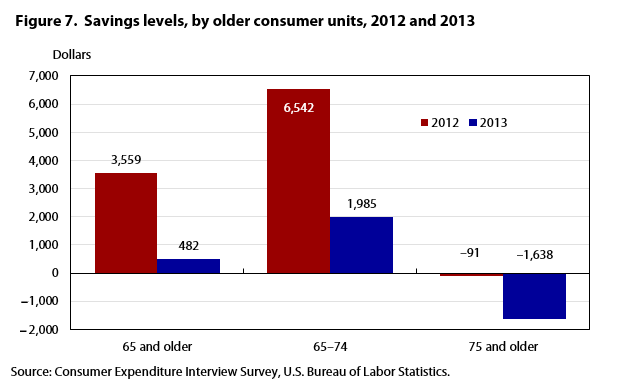

Even more interesting are the implications for analyses of consumer spending, as mentioned earlier in this article. Most easily demonstrated are savings. Broadly construed, “savings” can be defined as the difference between income after taxes and total expenditures. A positive gap is “savings,” whereas a negative gap is “dissavings.” The life-cycle theory suggests that while young adults, consumers have low average income and may go into debt to pay for education, a first home, or other reasons. It further suggests that during middle age, as average incomes increase, they will start to pay off these debts and to save in order to finance retirement years, when they will dissave, in part because of their return to lower average income status. However, for older consumers, the data collected prior to 2012 did not strongly support this theory. As shown in figure 7, in 2012, consumer units with reference persons age 65 and older on average “saved” more than $3,500. Even more impressive, was that within this group, those with a reference person younger than 75 “saved” more than $6,500. The oldest group (older than 75) dissaved, but negligibly so, with average annual expenditures exceeding average income after taxes by only $91 on average.17 Once TAXSIM is introduced, the numbers shift dramatically. For the group as a whole, savings falls substantially to less than $500. Within the group, those in the younger portion save less than $2,000, whereas those in the older portion dissave by a substantial amount: their expenditures exceed after-tax income by more than $1,600.

| Year | 65 and older | 65 to 74 | 75 and older |

|---|---|---|---|

| 2012 | $3,559 | $6,542 | –$91 |

| 2013 | $482 | $1,985 | –$1,638 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | |||

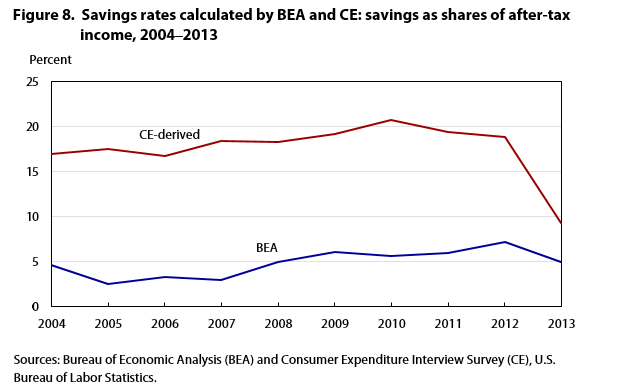

| Source | 2004 | 2005 | 2006 | 2007 | 2008 | 2009 | 2010 | 2011 | 2012 | 2013 |

|---|---|---|---|---|---|---|---|---|---|---|

| CE-derived | 17.0 | 17.6 | 16.7 | 18.4 | 18.3 | 19.2 | 20.8 | 19.4 | 18.8 | 9.3 |

| BEA | 4.6 | 2.5 | 3.3 | 3.0 | 4.9 | 6.1 | 5.6 | 6.0 | 7.2 | 4.9 |

| Sources: Bureau of Economic Analysis (BEA) and Consumer Expenditure Interview Survey (CE), U.S. Bureau of Labor Statistics. | ||||||||||

A related concept is the “savings rate,” or the portion of disposable income that is saved as opposed to spent. Savings rates have been low in recent years, as measured by the Bureau of Economic Analysis (BEA), which computes the official figures for the United States. Figure 8 shows that prior to 2013, the CE savings rate ranged from about 3 to 6 times the official BEA rate.18 However, in 2013, it is less than double the BEA rate. Although the gap in estimates is still substantial (4.9 percent for BEA and 9.3 for CE), both rates are in the single digits, whereas prior to 2013, only the BEA rate was ever below 10 percent. One reason for the continued gap may be due to different definitions of income, spending, drawing from assets to finance current consumption, or other factors across the sources. Another reason may be that the published CE tax data are estimated with TAXSIM for only 11 of every 12 consumer units interviewed in 2013, because of the rotating panel structure of the survey. That is, those interviewed in January 2013 reported taxes for calendar year 2012, and these reported values were used in publication; those interviewed from February onward had their taxes estimated by TAXSIM for the portion owed in 2013 (i.e., January taxes for those interviewed in February, January and February taxes for those interviewed in March, and so forth).

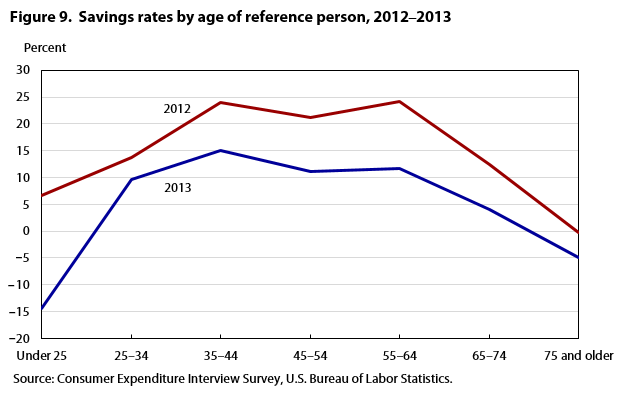

| Age range | 2012 | 2013 |

|---|---|---|

| Under 25 | 6.7 | –14.4 |

| 25–34 | 13.7 | 9.6 |

| 35–44 | 24.0 | 15.0 |

| 45–54 | 21.2 | 11.1 |

| 55–64 | 24.1 | 11.7 |

| 65–74 | 12.5 | 4.1 |

| 75 and older | –0.3 | –5.0 |

| Source: Consumer Expenditure Interview Survey, U.S. Bureau of Labor Statistics. | ||

Similar patterns hold when we examined the savings rates by demographic groups, rather than for the nation as a whole. For example, when returning to the age data (figure 9), the savings rate decreases accordingly from 12.5 percent for the 65- to 74-year-old group in 2012 to 4.1 percent in 2013 and from a negligible (dis)savings rate of –0.3 percent for the 75 and older group in 2012 to a noticeable –5.0 percent in 2013.19 In addition, the pattern demonstrated in 2013 is consistent with the life-cycle theory, with the youngest dissaving substantially (perhaps through debt) and the oldest dissaving noticeably, with those in the middle-age groups (35 to 64) saving at the highest rates. In contrast, in 2012, all groups save except for the oldest, which dissaves negligibly.

As noted earlier, the tax questions asked in the survey may be difficult for some respondents to answer and thus contribute to the relatively low response rate for these questions. Therefore, with the need to ask these questions eliminated, the implementation of TAXSIM is expected to provide another benefit: reduction of respondent burden. One way to measure the reduction is to compare the average time a respondent takes to complete the section of the survey in which these questions are asked (currently Section 21B of the Interview Survey) before and after the questions are eliminated. However, because the tax questions will remain in the survey until the next redesign of the questionnaire in April 2015 and no data are available specifically on the time needed to collect the tax data, measuring the reduction in this way is a topic for future investigation.

Nonresponse is a common problem in household surveys. In the CE, methods have long been in place to handle nonresponse to expenditure data. Since publication of the 2004 data, the method of multiple imputation has been used to address nonresponse for income data. Introduced in 2013 is another major improvement—using TAXSIM software to produce estimates for tax data. As this article shows, implementing TAXSIM has substantially increased data quality. At the same time, this process is expected to reduce respondent burden by eliminating questions that are difficult to answer.

The remaining major financial item for which no procedure is in place is financial assets and liabilities. Although mechanisms for handling nonresponse for some liabilities, such as mortgages and car loans have long been in place, other items, such as credit card balances, checking and savings deposits, and student loans, are not currently adjusted. A team is now investigating those items not currently adjusted. If a feasible method is found, the results it yields will represent another milestone in the improvement of CE data quality.

ACKNOWLEDGMENTS: The CE program gratefully acknowledges the support of the NBER for improving the tax estimates and especially Dan Feenberg, Research Associate, NBER, whose assistance with TAXSIM was crucial from the beginning of the project.

!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>Geoffrey D. Paulin, and William Hawk, "Improving data quality in Consumer Expenditure Survey with TAXSIM," Monthly Labor Review, U.S. Bureau of Labor Statistics, March 2015, https://doi.org/10.21916/mlr.2015.5

1 Prior to 1980, the survey was collected periodically, approximately once every 10 years. This time frame changed when the 1972–1973 survey was conducted, because the economy experienced serious dislocations almost as soon as the survey was completed.

2 Because of the rotating panel nature of the data, some participants interviewed in March 2014 reported expenditures that occurred in December 2013. However, in April, the earliest expenditures collected occurred in January 2014. Although the TAXSIM models described in this article were implemented with production of 2013 data, the questions were scheduled to be collected throughout 2014 and first quarter (January through March) 2015.

3 “Consumer expenditures and income,” “Sample design: selection of households,” BLS Handbook of Methods (U.S. Bureau of Statistics, July 10, 2013), chapter 16, p. 5, https://www.bls.gov/opub/hom/pdf/homch16.pdf.

4 See, for example, Jonathan Fisher, David S. Johnson, and Timothy M. Smeeding, “Inequality of income and consumption in the U.S.: measuring the trends in inequality from 1984 to 2011 for the same individuals,” Review of Income and Wealth, July 2, 2014, http://on linelibrary.wiley.com/doi/10.1111/roiw.12129/abstract; and Bruce D. Meyer and James X. Sullivan, “Consumption and income inequality and the great recession,” American Economic Review, American Economic Association, vol. 103, no. 3, May 2013, pp. 178, http://harris.uchicago.edu/sites/default/files/AEAPandP20 13.pdf.

5 See Geoffrey D. Paulin and David L. Ferraro, “Imputing income in the Consumer Expenditure Survey,” Monthly Labor Review, December 1994, pp. 23–31, https://www.bls.gov/mlr/1994/ 12/art3full.pdf.

6 According to the Consumer Expenditure Survey (CE) glossary, “A consumer unit comprises either (1) all members of a particular household who are related by blood, marriage, adoption, or other legal arrangements; (2) a person living alone or sharing a household with others or living as a roomer in a private home or lodging house or in permanent living quarters in a hotel or motel, but who is financially independent; or (3) two or more persons living together who use their income to make joint expenditure decisions. Financial independence is determined by the three major expense categories: housing, food, and other living expenses. To be considered financially independent, the respondent must provide, either entirely or in part, at least two of the three major expense categories,” https://www.bls.gov/cex/csxgloss.htm.

7 The reference person is defined as “The first member mentioned by the respondent when asked to ‘start with the name of the person or one of the persons who owns or rents the home.’ It is with respect to this person that the relationship of the other consumer unit members is determined.” See Consumer Expenditure Survey glossary, https://www.bls.gov/cex/csxgloss.htm.

8 According to the definition of “complete income reporters” in the Consumer Expenditure Survey (CE) glossary, “major sources of income” include sources “such as wages and salaries, self-employment income, and Social Security income”; see CE glossary, https://www.bls.gov/cex/csxgloss.htm. Certain other limited conditions meet the definition of complete income reporter, including when the reference person reports zero income for all income sources and the nonreference person or the consumer unit reports a value for income from a major source and zero or other value for all other sources of income.

9 For example, a respondent who paid $100 in taxes and received a $10 refund actually paid $90. The survey instrument asks for both the amount paid in total ($100 here) and the amount of the refund. However, if the respondent reports, “I did not pay anything in taxes; I received a refund,” the instrument may show $0 for taxes paid and $10 for the refund, resulting in –$10 calculated for the taxes paid. At the same time, overreporting of taxes was adjusted. For example, if the respondent reported an amount for taxes withheld from the last paycheck that exceeded a critical value (percentage of income), the case was reviewed and the tax value was reset in accordance with the critical value. This adjustment exacerbates the downward bias in tax estimates. That is, the values provided were capped if deemed too high, but not increased—or even checked—if too low.

10 The data cited are not directly comparable, in part, because of the range of incomes described ($70,000 or greater for Consumer Expenditure Survey (CE) and $75,000 or greater for the Internal Revenue Service) but also because the components of income collected in the CE are not based directly on the adjusted gross income concept. In any case, the data cited are from “All returns: selected income and tax items, by size and accumulated size of adjusted gross income, tax year 2012,” table 1.1 (Internal Revenue Service), https://www.irs.gov/statistics/soi-tax-stats-individual-statistical-tables-by-size-of-adjusted-gross-income; click “2003” and “2004” under “Individual income tax returns filed and sources of income, all returns: selected income and tax items.”

11 This decrease is to be expected if respondents who required imputation because of nonresponse to income questions also reported little or no tax information. If so, filling in the blanks for income would move some who reported less than $70,000 into the $70,000-and-greater category, which may or may not affect average income for this group but would definitely lower the average tax value for the now-larger group, because it would include a larger percentage of $0 or near-$0 tax reports.

12 Daniel Feenberg and Elisabeth Coutts, “An introduction to the TAXSIM model,” Journal of Policy Analysis and Management, vol. 12, no. 1, 1993, pp. 189–194, http://users.nber.org/~taxsim/feenberg-coutts.pdf.

13 For more on estimating tax liabilities, see the TAXSIM tool, http://users.nber.org/~taxsim/taxsim- calc9/index.html.

14 In 2008, the Consumer Expenditure Survey (CE) included a special question about tax rebates received from the economic stimulus payments. The CE program included these tax rebates in the personal taxes section. A consumer unit receiving a rebate was counted as a consumer unit reporting a (negative) personal tax. As a result, the percentage of consumers reporting taxes was noticeably higher than for any year between 2004 (the first data to include imputed income information) and 2012 (the last data processed before TAXSIM was introduced). For more information, see “Consumer Expenditure Survey results on the 2008 economic stimulus payments (tax rebates)” (U.S. Bureau of Labor Statistics, October 15, 2009), https://www.bls.gov/cex/taxrebate.htm.

15 In 2013, the income section of the CE questionnaire changed. Some sources of income (for example, nonfarm self-employment income and farm self-employment income) were combined into a single question, and others were reconfigured (for example, dividends were separated from royalties, estates, and trusts and combined with interest income, which had been collected as a single item through 2012).

16 The dollar values for the less-than-$70,000 income group are so low because, in both 2012 and 2013, personal taxes were negative for all consumers with less than $30,000 in income before taxes. In 2012, even those in the $30,000 to $39,999 group reported negative taxes (–$45) on average. However, the percentage increase still holds, at least for the highest income members of this group ($50,000 to $69,999): In 2012, the value of reported taxes paid was $1,084; in 2013, the TAXSIM-derived value was $4,388, an increase of 305 percent. Even this value is substantially larger than the 232 percent described in the text for those with before-tax income of at least $70,000.

17 From 2004 through 2011, those reference persons age 75 and older only dissaved in 3 years: 2006 (–$54), 2009 (–$404), and 2011 (–$909). In the other years, savings for this group ranged from $109 (2010) to $1,379 (2004). In none of these years did those aged from 65 to 74 dissave. The smallest savings level for this group in this period was $2,969 (2008), still nearly $1,000 more than shown for 2013.

18 Data can be found at “Comparison of personal saving in the NIPAs with personal saving in the FFAs,” table (U.S. Bureau of Economic Analysis, August 2014), https://www.bea.gov/iTable/index_nipa.cfm.

19 From 2004 through 2011, the savings rate for the older group ranged from a (dis)savings rate of about –3 percent (2011) to a savings rate of about 5 percent (2004). For the younger group, the savings rate ranged from nearly 7 percent (2008 and 2009) to nearly 15 percent (2010).