An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

In response to airlines’ increasingly complex and variable airfare pricing regimes in recent decades, the Bureau of Labor Statistics moved from an individual fare code approach to tracking prices to an average-pricing approach; as a result, the Producer Price Index for scheduled passenger air transportation is better able to capture true airline pricing behavior.

The Bureau of Labor Statistics (BLS) publishes a monthly Producer Price Index (PPI) for the North American Industry Classification System (NAICS) industry 481111, scheduled passenger air transportation. The introduction of this index in 1989 expanded BLS coverage of service industries,1 with the airline industry accounting for approximately one-fifth of the revenue for NAICS sector 48–49, transportation and warehousing.2

Since the scheduled passenger air transportation price index was first introduced, airline pricing has changed substantially. The rising importance of the Internet as a distribution channel, as well as improvements in computerized revenue management systems, has allowed airlines to monitor supply and demand more closely. As a result, seat-by-seat variation in prices paid by passengers on the same flight has increased. Also, frequent-flyer programs have grown to the point where they have caused prices to vary as more passengers are awarded free or discounted tickets. More recently, airlines have expanded the number of ancillary fees they charge for transporting baggage and for other services related to air travel.

Because of all these developments, the method for calculating the price index for scheduled passenger air transportation was modified. This article discusses the transition from the fare-code-based pricing method used when BLS first introduced the index to the average-revenue-per-passenger approach that is currently employed. Whereas the fare-code approach was based on tracking the prices for individual tickets, the average-revenue method reflects the real transacted price for all passengers who travel on each BLS-sampled flight. The strategies that were more recently enacted to account for new ancillary fees also are described. The impacts of these changes are then evaluated, with a focus on the relationship between the PPI air passenger index and the price index produced by the airline trade organization Airlines for America (A4A).3

Throughout the 1990s, the PPI for the airline industry was based on a pricing method according to which an individual fare code offered by a sampled airline was selected for a specific origin and destination (O&D). The starting and ending point of a flight, the O&D is variously referred to as a route, city pair, or market. Each fare code specifies the following characteristics:

· The class in which the passenger will travel (e.g., first class, coach)

· Advance purchase information (e.g., 7 days in advance of the flight, 14 days, the same day as the flight)

· Allowable travel days (e.g., weekdays; weekends; all days; particular restricted days, such as holidays)

· Restrictions on changing or canceling the ticket

· Whether the ticket can be upgraded to a higher class of travel, pending availability

· The percentage of the number of miles flown that are granted as frequent-flyer miles (e.g., 150 percent of miles flown granted, 50 percent of miles flown granted)

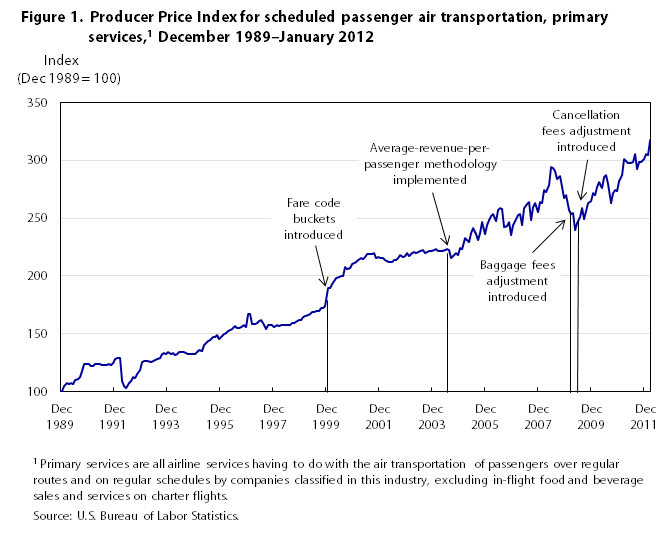

Figure 1 displays the PPI for scheduled passenger air transportation from December 1989 to January 2012 and illustrates the major PPI-related events that took place during that timeframe.

| Month and year | Producer Price Index for scheduled passenger air transportation, primary services |

|---|---|

Dec 1989 | 100.0 |

Jan 1990 | 101.0 |

Feb | 105.1 |

Mar | 107.2 |

Apr | 106.9 |

May | 107.5 |

Jun | 107.0 |

Jul | 110.6 |

Aug | 110.7 |

Sep | 112.7 |

Oct | 117.7 |

Nov | 123.8 |

Dec 1990 | 124.1 |

Jan 1991 | 124.3 |

Feb | 122.5 |

Mar | 122.5 |

Apr | 124.0 |

May | 123.7 |

Jun | 123.6 |

Jul | 123.3 |

Aug | 123.5 |

Sep | 123.1 |

Oct | 123.7 |

Nov | 123.4 |

Dec 1991 | 124.8 |

Jan 1992 | 128.7 |

Feb | 128.8 |

Mar | 129.6 |

Apr | 109.5 |

May | 105.3 |

Jun | 103.0 |

Jul | 107.8 |

Aug | 109.5 |

Sep | 112.5 |

Oct | 112.0 |

Nov | 115.1 |

Dec 1992 | 118.7 |

Jan 1993 | 125.4 |

Feb | 126.3 |

Mar | 126.3 |

Apr | 126.4 |

May | 126.1 |

Jun | 126.3 |

Jul | 127.6 |

Aug | 128.5 |

Sep | 129.6 |

Oct | 132.3 |

Nov | 133.3 |

Dec 1993 | 132.7 |

Jan 1994 | 134.5 |

Feb | 132.5 |

Mar | 133.4 |

Apr | 132.2 |

May | 132.3 |

Jun | 134.4 |

Jul | 134.1 |

Aug | 134.1 |

Sep | 133.3 |

Oct | 132.8 |

Nov | 132.6 |

Dec 1994 | 132.3 |

Jan 1995 | 132.6 |

Feb | 134.7 |

Mar | 135.8 |

Apr | 135.0 |

May | 140.4 |

Jun | 142.2 |

Jul | 143.8 |

Aug | 144.9 |

Sep | 147.4 |

Oct | 147.4 |

Nov | 148.8 |

Dec 1995 | 145.3 |

Jan 1996 | 147.7 |

Feb | 150.3 |

Mar | 151.2 |

Apr | 152.2 |

May | 153.4 |

Jun | 154.3 |

Jul | 156.4 |

Aug | 155.3 |

Sep | 155.3 |

Oct | 156.0 |

Nov | 157.4 |

Dec 1996 | 155.7 |

Jan 1997 | 167.3 |

Feb | 167.0 |

Mar | 158.6 |

Apr | 158.9 |

May | 159.3 |

Jun | 161.4 |

Jul | 162.0 |

Aug | 159.8 |

Sep | 154.4 |

Oct | 157.5 |

Nov | 157.3 |

Dec 1997 | 157.3 |

Jan 1998 | 156.1 |

Feb | 157.5 |

Mar | 157.2 |

Apr | 158.0 |

May | 157.9 |

Jun | 157.5 |

Jul | 157.5 |

Aug | 157.5 |

Sep | 159.4 |

Oct | 159.7 |

Nov | 160.8 |

Dec 1998 | 161.6 |

Jan 1999 | 161.9 |

Feb | 164.9 |

Mar | 165.8 |

Apr | 166.5 |

May | 167.1 |

Jun | 168.8 |

Jul | 169.0 |

Aug | 169.4 |

Sep | 169.6 |

Oct | 172.0 |

Nov | 172.5 |

Dec 1999 | 173.9 |

Jan 2000 | 189.9 |

Feb | 189.3 |

Mar | 192.7 |

Apr | 195.6 |

May | 197.9 |

Jun | 199.2 |

Jul | 200.1 |

Aug | 200.2 |

Sep | 207.9 |

Oct | 206.2 |

Nov | 206.8 |

Dec 2000 | 210.3 |

Jan 2001 | 210.9 |

Feb | 212.3 |

Mar | 213.5 |

Apr | 215.7 |

May | 214.7 |

Jun | 216.2 |

Jul | 218.8 |

Aug | 219.0 |

Sep | 218.8 |

Oct | 220.2 |

Nov | 215.3 |

Dec 2001 | 216.1 |

Jan 2002 | 215.4 |

Feb | 215.3 |

Mar | 214.0 |

Apr | 212.6 |

May | 212.2 |

Jun | 212.3 |

Jul | 214.2 |

Aug | 214.0 |

Sep | 215.2 |

Oct | 217.7 |

Nov | 216.6 |

Dec 2002 | 217.2 |

Jan 2003 | 219.6 |

Feb | 217.0 |

Mar | 220.0 |

Apr | 220.4 |

May | 220.2 |

Jun | 220.9 |

Jul | 221.7 |

Aug | 222.4 |

Sep | 220.1 |

Oct | 220.8 |

Nov | 221.2 |

Dec 2003 | 221.6 |

Jan 2004 | 222.0 |

Feb | 222.9 |

Mar | 221.2 |

Apr | 221.8 |

May | 221.7 |

Jun | 222.3 |

Jul | 222.9 |

Aug | 222.1 |

Sep | 215.2 |

Oct | 217.7 |

Nov | 220.1 |

Dec 2004 | 217.9 |

Jan 2005 | 224.5 |

Feb | 223.7 |

Mar | 232.5 |

Apr | 230.9 |

May | 229.4 |

Jun | 237.1 |

Jul | 241.3 |

Aug | 236.6 |

Sep | 231.4 |

Oct | 237.1 |

Nov | 246.5 |

Dec 2005 | 236.4 |

Jan 2006 | 244.4 |

Feb | 248.4 |

Mar | 251.7 |

Apr | 253.7 |

May | 247.8 |

Jun | 256.9 |

Jul | 258.8 |

Aug | 258.0 |

Sep | 242.6 |

Oct | 243.4 |

Nov | 247.0 |

Dec 2006 | 235.1 |

Jan 2007 | 244.3 |

Feb | 247.4 |

Mar | 252.4 |

Apr | 253.9 |

May | 243.9 |

Jun | 258.5 |

Jul | 262.1 |

Aug | 264.0 |

Sep | 248.2 |

Oct | 259.1 |

Nov | 262.6 |

Dec 2007 | 255.6 |

Jan 2008 | 264.0 |

Feb | 263.0 |

Mar | 274.2 |

Apr | 272.3 |

May | 278.3 |

Jun | 294.0 |

Jul | 293.2 |

Aug | 290.4 |

Sep | 283.7 |

Oct | 286.1 |

Nov | 277.1 |

Dec 2008 | 267.7 |

Jan 2009 | 269.5 |

Feb | 256.8 |

Mar | 253.6 |

Apr | 254.1 |

May | 239.6 |

Jun | 245.4 |

Jul | 251.3 |

Aug | 258.9 |

Sep | 249.5 |

Oct | 255.8 |

Nov | 262.8 |

Dec 2009 | 265.1 |

Jan 2010 | 271.3 |

Feb | 269.6 |

Mar | 276.4 |

Apr | 281.4 |

May | 275.8 |

Jun | 285.0 |

Jul | 286.8 |

Aug | 279.7 |

Sep | 263.1 |

Oct | 271.3 |

Nov | 273.8 |

Dec 2010 | 273.4 |

Jan 2011 | 282.2 |

Feb | 286.9 |

Mar | 301.0 |

Apr | 299.3 |

May | 297.6 |

Jun | 297.7 |

Jul | 298.5 |

Aug | 305.2 |

Sep | 292.2 |

Oct | 298.8 |

Nov | 298.5 |

Dec 2011 | 300.6 |

Jan 2012 | 305.3 |

Feb | 304.7 |

Mar | 317.3 |

One advantage of pricing a single fare code was that it ensured consistency with the “fixed input output price index” (FIOPI) assumptions that form the basis of the program’s index methodology.4 In addition, the terms of transaction for each sale were held constant in all pricing periods.

However, airline industry trends that occurred throughout the 1990s and 2000s revealed key weaknesses with the fare code method. As airline computer systems became more advanced, the airlines began issuing a larger variety of fare codes so that they could more easily react to changes in demand. At the same time, the airline industry shifted away from traditional distribution channels, such as call centers and brick-and-mortar travel agencies, and toward Internet-based distribution channels. The shift toward Internet-based distribution channels was expedited as the airlines began to charge customers small fees for speaking with call center representatives and as they stopped paying commissions to traditional travel agencies, causing many of them to go out of business.5 Web-based airline ticket distributors, such as Expedia and Travelocity, earned increasing revenues and market share during that time. Airlines responded by selling tickets directly to consumers via the Internet in order to compete with these online travel agencies.

At the same time, consumers felt that they could make informed decisions and realize greater savings by using both online travel agents and the airlines’ websites to do comparison shopping. Internet bookings from those two sources grew from 7 percent of all bookings in 1999 to 30 percent by 2002.6 As airlines began selling more tickets directly online to passengers, they introduced an increasing number of new fare codes, including Internet-only fares and deep discount email sales. As these and more fare codes were introduced, it became increasingly difficult to represent industry prices with existing PPI item allocations. Requesting additional items was considered, but respondent burden was a concern, with BLS unwilling to jeopardize continued cooperation with the survey.

At the time, the PPI airline index did not encompass these Internet fare codes. As a result, in early 2003 BLS analysts conducted research to gauge the feasibility of augmenting pricing data to include deeply discounted web-based fares. The research indicated that it would not be possible to use the fare code method to maintain constant-quality fare codes to be tracked over time, because many web-based fare codes were introduced with deep discounts and then quickly discontinued. This strategy on the part of the airlines created a twofold problem: deeply discounted fare codes with special restrictions were almost impossible to select for pricing, and even if these fare codes were selected for pricing, they would be discontinued so quickly that they could not be priced consistently from month to month. For example, some airlines introduce holiday fire sales on the Fourth of July and then remove these fare codes as soon as the holiday ends.

Another shortcoming of the fare code method is that frequent-flyer mile awards, referred to as zero fares in the industry, were excluded from the PPI because they do not generate revenue. Worse, the problem was exacerbated by rapidly rising numbers of frequent-flyer miles granted through avenues other than air travel, such as credit card spending, hotel stays, rental car bookings, and shopping at preferred vendors.7 The total number of frequent-flyer awards redeemed grew 61.7 percent from 1997 to 2005.8 With the fare code method, this increased granting of frequent-flyer awards was not directly shown as a price decrease in the data for the index.

As airlines changed or removed fare codes that the PPI tracked, the typical procedure was to substitute another fare code with similar characteristics. Base fare codes were frequently taken as substitutes, because they were usually offered each month. These codes, however, did not reflect periodic fare sales and were not always regularly used. As more and more fare codes were replaced over time, the PPI airline index ended up with a large number of base fare codes that tended to increase in a slow and steady manner, irrespective of market conditions.

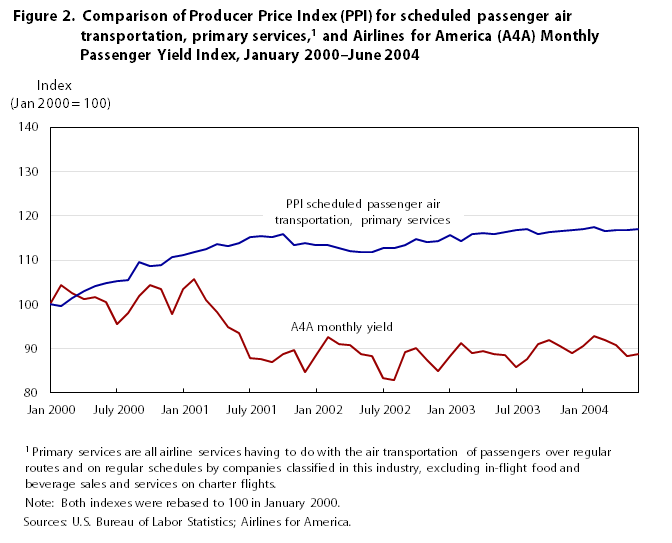

As figure 2 illustrates, the limitations of the fare code method caused the PPI passenger airline index to fail to capture price declines that were reflected in the A4A Monthly Passenger Yield Index9 in the period from January 2000 to June 2004. During this period, the PPI airline index grew almost 20 percent while the A4A index declined more than 10 percent.

| Month and year | A4A Monthly Passenger Yield Index | PPI scheduled passenger air transportation, primary services |

|---|---|---|

Jan 2000 | 100.0 | 100.0 |

Feb | 104.3 | 99.7 |

Mar | 102.5 | 101.5 |

Apr | 101.2 | 103.0 |

May | 101.6 | 104.2 |

Jun | 100.4 | 104.9 |

July 2000 | 95.6 | 105.4 |

Aug | 97.9 | 105.4 |

Sep | 101.9 | 109.5 |

Oct | 104.3 | 108.6 |

Nov | 103.5 | 108.9 |

Dec | 97.8 | 110.7 |

Jan 2001 | 103.4 | 111.1 |

Feb | 105.6 | 111.8 |

Mar | 100.9 | 112.4 |

Apr | 98.4 | 113.6 |

May | 94.8 | 113.1 |

Jun | 93.6 | 113.8 |

July 2001 | 87.9 | 115.2 |

Aug | 87.7 | 115.3 |

Sep | 87.0 | 115.2 |

Oct | 88.9 | 116.0 |

Nov | 89.7 | 113.4 |

Dec | 84.7 | 113.8 |

Jan 2002 | 88.5 | 113.4 |

Feb | 92.6 | 113.4 |

Mar | 91.1 | 112.7 |

Apr | 90.9 | 112.0 |

May | 88.8 | 111.7 |

Jun | 88.3 | 111.8 |

July 2002 | 83.4 | 112.8 |

Aug | 83.0 | 112.7 |

Sep | 89.2 | 113.3 |

Oct | 90.1 | 114.6 |

Nov | 87.5 | 114.1 |

Dec | 85.0 | 114.4 |

Jan 2003 | 88.4 | 115.6 |

Feb | 91.3 | 114.3 |

Mar | 89.0 | 115.9 |

Apr | 89.6 | 116.1 |

May | 88.8 | 116.0 |

Jun | 88.5 | 116.3 |

Jul 2003 | 85.9 | 116.7 |

Aug | 87.6 | 117.1 |

Sep | 90.9 | 115.9 |

Oct | 91.9 | 116.3 |

Nov | 90.6 | 116.5 |

Dec | 89.1 | 116.7 |

Jan 2004 | 90.5 | 116.9 |

Feb | 92.9 | 117.4 |

Mar | 91.9 | 116.5 |

Apr | 90.9 | 116.8 |

May | 88.3 | 116.7 |

Jun | 88.7 | 117.1 |

John L. Lucier, and William J. Page III, "Scheduled passenger air transportation in the Producer Price Index: improvements and trends," Monthly Labor Review, U.S. Bureau of Labor Statistics, September 2013, https://doi.org/10.21916/mlr.2013.31

One method that BLS employed to deal with these issues was the introduction of a variation of the fare code method: the “fare code bucket” strategy, which was used from 2000 until 2004. With this approach, a group of fare codes with similar restrictions was presented to respondents on each survey form. When the originally selected fare code was either discontinued or not used in a given period, the respondent was instructed to provide instead the price for a ticket represented by one of the fare codes with similar restrictions. The price for the latter ticket was then directly compared with the price for the ticket covered by the originally selected fare code. The fare code bucket strategy allowed the index to capture some airline price changes that were executed by moving ticket inventory across similar fare codes, but the improvement was only transitory, because it still failed to capture deeply discounted temporary fare sales and zero fares.

To better reflect the increased use of the Internet and discounted and zero fares, BLS analysts developed a new method that uses average prices, calculated by dividing total passenger revenue (excluding taxes and government fees) earned from the sale of all tickets on all of the sampled airline’s flights on a selected O&D by the total number of passengers who traveled on those flights. This price is referred to as the average revenue per passenger, or ARPP, and the associated method is called the ARPP method.

An important consideration in establishing the ARPP method was how to define the period to be covered by the transactions involved. Ideally, ARPP data would cover an entire month so that any and all travel-related events that occur in a given month (such as holidays) would be included. However, this approach presented a problem because participating airlines needed a number of days after the end of the month to retrieve and report the data. The problem arises because the BLS requires a closeout date for price submission so that indexes can be calculated and analyzed prior to public dissemination, and this closeout date occurs close to the end of the month, too early for the airlines to provide data on all travel days in the month. As a result, full monthly ARPP data could be reported only with a 1-month lag. Using an ARPP that covers the first 21 calendar days of the current month was selected as an alternative. This strategy allowed ample time (about 7 business days, on average) for a participating airline to retrieve and submit its data for inclusion in the current month’s index. Also, three occurrences of each day of the week would be used to calculate the data. This stipulation is important because airline fares typically fluctuate with the day of the week of travel and the averages would, therefore, not be comparable if varying numbers of weekday or weekend flights were included from month to month. Finally, using a 21-day period served to produce a more accurate index than would be produced with a 7- or 14-day period, because, with the former, more flights are represented.

To maintain consistency with the FIOPI principle, the O&D and class of service are held constant in all ARPP transactions collected. Once the O&D is selected, it is classified as domestic or international.

Using the ARPP pricing method allows the PPI to capture price trends from all ticketed transactions, regardless of how or by what means the tickets are distributed. Figure 3 demonstrates that, once the ARPP method was fully introduced by late 2004, the PPI airline index exhibited vastly different movement on a month-to-month basis, compared with its movement when the fare code method was in effect. The index also began to exhibit the expected seasonal pattern of fares increasing each year at the beginning of the summer vacation season in June.

The ARPP methodology was implemented on a flow basis. As each airline that was sampled agreed to ARPP pricing, the new data were incorporated into the index and that airline’s fare-code-based pricing was discontinued. The process began in early 2004 and was completed by the end of that year.

As the airline industry lost more than $50 billion between 2001 and 2011,10 firms began to focus increasingly on alternative revenue management strategies. One important way that airlines generated additional revenue was through new or increased ancillary fees. Although some ancillary fees had existed for years, many airlines started charging new fees for services that traditionally were part of the service that passengers expected when purchasing an airline ticket. Among the new fees were fees for first and second checked bags, cancellations of tickets, seat selection, blankets and pillows, carry-on bags, reservations made over the phone or in person (as opposed to those made over the Internet), and in-flight food and beverages. Revenue attributable to most of these fees is a small part of overall revenue, with the exception of baggage and cancellation charges, which are the most common and the largest of the new fees in terms of revenue. Revenue from these two sources, which have become increasingly important contributors to airlines’ bottom lines, grew from $1.4 billion in 2007 to $5.7 billion in 2010.11 Figure 4 shows the growth in revenue generated by baggage and cancellation fees over the last two decades.

Because system limitations prevent most airlines from accounting for ancillary fees on an O&D basis, such fees are not included in the average-revenue-per-passenger data collected for the PPI. BLS attempted to obtain data on baggage and cancellation fees directly from sampled airlines, but the airlines were unable to report the information in a timely manner. As a result, BLS instead utilizes fee data published by the Bureau of Transportation Statistics (BTS). With these data, BLS developed a procedure to capture the percent change caused by the implementation of first and second checked bag fees by U.S. airlines. First, average bag fees per passenger are calculated for each sampled airline by dividing total passenger baggage fee revenue by total passengers. Then, the average bag fees per passenger are added to the average revenue per passenger, for each O&D that the PPI collects directly from the airlines, yielding the adjusted average revenue per passenger. This adjusted average revenue per passenger is used in the PPI airline index, with the adjustment calculated separately on a quarterly basis for domestic and international O&Ds. The procedure allows the PPI to incorporate the baggage fees within the 5-month period after initial publication of the index, a period in which PPI data remain subject to revision.12 The initial baggage fee adjustment was first reflected in the PPI airline index in March 2009 in a manner that isolated the change due to the imposition of first and second checked bag fees. Baggage fees continues to be adjusted each quarter, and a similar procedure was instituted for cancellation fees, with data reflecting this adjustment introduced in May 2009.

Although the PPI for scheduled passenger air transportation and the A4A Monthly Passenger Yield Index are similar, there are some important differences between them. The main difference involves the FIOPI concept, to which the PPI must adhere whereas the A4A index does not. In order to stay consistent with FIOPI, the PPI holds trip length constant by collecting average prices for specified O&Ds. By contrast, the A4A index does not hold trip length constant, instead using systemwide data. As a result, when airlines add or drop routes, A4A data may be affected whereas the PPI (under a methodology that is consistent with its use as a price deflator) would not. The A4A index divides total revenue by revenue passenger miles flown, while the PPI uses only the number of passengers in the denominator. Also, the PPI includes baggage and cancellation fee data that are excluded from the A4A index. Table 1 compares and contrasts the PPI and the A4A index.

| PPI | A4A |

|---|---|

| Average revenue per passenger, plus adjustments for bag and cancellation fees * excludes government taxes and fees | Yield: the average fare paid by customers to fly 1 mile * excludes government taxes and fees * excludes baggage and cancellation fees |

| Published monthly, usually by the second week of the next month | Monthly data typically released around the 21st day of the next month |

| Data published by geographic region and class of service | Data published by geographic region |

| Domestic (coach and first class) and international | Domestic |

| O&D and class of service are held constant | Trip length is not held constant |

| Sample of all U.S. airlines | Data from Alaska, American, Delta, JetBlue, Southwest,(1) United, and US Airways and their affiliated regional airline partners |

| Data are based on a sample of O&Ds from each participating airline and include zero fares (frequent flyer miles) | Data are based on 100 percent of scheduled service and reflect all "revenue" passengers, including those redeeming frequent flyer miles ($0 fare) for award travel |

| (1) Southwest was recently added in January 2012, reflecting data back to January 2008. | |

Quantitative analysis.

Figure 5 shows the PPI airline index after the ARPP methodology was implemented in 2004. Since that time, the magnitude and the direction of the changes in the PPI have closely mirrored the changes in the A4A Monthly Passenger Yield Index.

Figure 6 shows 1-month percent changes in the two indexes for the period from January 2000 to July 2004. Over this period, the PPI exhibited minimal changes (ranging mostly between plus and minus 2 percent). After 2004, the PPI exhibited changes ranging between plus and minus 6 percent, more in line with changes in the A4A Monthly Passenger Yield Index during the same time.

Twelve-month percent changes in these indexes, shown in figure 7, offer further visual evidence of the PPI’s movement before and after the introduction of the ARPP methodology. Prior to 2005 the changes differed from those of the A4A index, whereas after 2005 both indexes have exhibited similar long-term trends.

Clearly, the discrepancies between the PPI and the A4A index were substantially reduced after the ARPP methodology was introduced into the PPI in the middle of 2004. The correlation of these time series confirms this observation. Taking 1- and 12-month changes tends to remove trend and seasonality from time series, making the series stationary. The series can then be correlated. The following tabulation shows the correlation of the 1- and 12-month percent changes for the PPI and the A4A index:

| Period | 1-month percent change | 12-month percent change |

| January 2000–February 2012 | 0.432 | 0.675 |

| January 2000–July 2004 | –.121 | –.113 |

| July 2004–February 2012 | .671 | .917 |

The tabulation shows that, in the period prior to the implementation of the ARPP methodology in 2004, the coefficients were close to zero, so the changes in the indexes were weakly correlated. After the ARPP implementation, a much different picture emerged: changes in the PPI began showing significant positive correlation with the A4A index, with the 12-month changes particularly strongly correlated. This strong correlation indicates that the two measures now show similar long-term trends.

The effect of baggage and cancellation fees was analyzed in a May 2012 Beyond the Numbers article.13 The authors of that article estimate that, if the adjustment for new baggage and cancellation fees had not been made, the PPI for scheduled passenger air transportation would have been 1.6 percent lower in December 2009 than the final data indicated.

As the complexity and variation of airfare pricing increased in recent decades, BLS responded by modifying the methodology used to track prices from an individual fare code approach to an average-pricing approach. The latter methodology allows the PPI to monitor prices for all passenger ticket sales for a given O&D and seat class. This approach greatly increases the number of transactions that are included in the PPI sample. It also allows the index to reflect price changes caused by the addition of new fare codes, the shifting of inventory across existing fare codes, and the granting of frequent-flyer mile awards. Since this change, the PPI for scheduled passenger air transportation has behaved similarly to the A4A Monthly Passenger Yield Index.

BLS also has developed strategies to ensure that new and expanded airline fees are reflected in the air transportation PPI. BTS data are now used to adjust average prices to account for baggage and cancellation fees. This modification has been critical, given that airline baggage and cancellation fee revenue quadrupled between 2007 and 2010.

As a result of these methodological improvements, the Bureau of Economic Analysis (BEA) began using the PPI for NAICS 481111 to deflate the air transportation portion of the personal consumption expenditures account in July 2008. The BEA did not previously use the PPI for NAICS 481111, because the agency was not satisfied that the fare code pricing methodology measured price trends accurately.

1 See Roslyn Swick, Deanna Bathgate, and Michael Horrigan, “Services producer price indices: past, present, and future,” paper prepared June 30, 2006, for presentation at the Conference on Research in Income and Wealth, July 17–19, 2006, Cambridge, MA, http://conference.nber.org/confer/2006/si2006/prcr/swick.pdf.

2 “2007 Economic Census” (U.S. Census Bureau), https://www.census.gov/econ/census07.

3 “A4A monthly passenger and cargo yield (fares per mile)” (Washington, DC: Airlines for America®, June 2013), http://www.airlines.org/Pages/A4A-Monthly-Passenger-Yield-(Fares-per-Mile).aspx

4 See “Services producer price indices,” section 2.5.

5 The number of travel agency establishments dropped 46 percent from 1997 to 2007, according to 1997 and 2007 Economic Census data.

6 “Airline ticketing: impact of changes in the airline ticket distribution industry,” GAO-03-749 (U.S. General Accounting Office, July 31, 2003), http://www.gao.gov/products/GAO-03-749.

7 “Press room: Top 10 mileage earning methods,” Frequent Flyer Services (Colorado Springs, CO, updated daily), http://www.frequentflyerservices.com/press_room/facts_and_stats/top_ten.php.

8 “Press room: Yearly award redemption figures—U.S.,” Frequent Flyer Services (Colorado Springs, CO, updated daily), http://www.frequentflyerservices.com/press_room/yearly_award_redemption/index.php.

9 The yield, or revenue passenger mile, is the average price, excluding taxes, paid to fly 1 mile. (See “A4A monthly passenger and cargo yield (fares per mile).”)

10 “U.S. airlines post lower earnings in 2011 due to rising costs” (Airlines for America®, February 28, 2012), http://www.airlines.org/Pages/news_2-28-2012.aspx.

11 Air Carrier Financial Schedule P-1.2 (Bureau of Transportation Statistics, March 2013), http://www.transtats.bts.gov/Fields.asp?Table_ID=295.

12 See “Producer Price Indexes: Frequently Asked Questions (FAQs),” questions 14 and 20 (U.S. Bureau of Labor Statistics, May 14, 2011), https://www.bls.gov/ppi/ppifaq.htm.

13 “How new fees are affecting the Producer Price Index for air travel,” Beyond the Numbers (U.S. Bureau of Labor Statistics, May 2012), https://www.bls.gov/opub/btn/volume-1/how-new-fees-are-affecting-the-producer-price-index-for-air-travel.htm.