An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

This article was corrected on December 10, 2015. In figure 2B, several of the projected labor force participation rates for 1996–2006 and 2000–10 originally shown in the figure were somewhat lower than the rates BLS actually projected. In figure 3C, the base year labor force participation rate for 2000–10 was corrected to 67.1 instead of 67.2.

Crossref 0

How Longer Work Lives Ease the Crunch of Population Aging, SSRN Electronic Journal, 2009.

Every 2 years, the U.S. Bureau of Labor Statistics (BLS) publishes 10-year projections of the labor force, the macroeconomy, and detailed industry and occupational employment. Periodically, BLS evaluates prior projections to help data users understand the inherent limitations of the projections methods and to allow an internal review of the underlying assumptions and methods. This article evaluates the three sets of projections over the periods 1996–06, 1998–2008, and 2000–10.

BLS normally evaluates each projection independently. However, these three sets of projections were evaluated together because of two methodological issues. The first issue is the distinction between a “projection” and a “forecast.” The second is the manifestation of the Great Recession coupled with the assumption that the unemployment rate would be consistent with the mature phase of the business cycle expansion.

Important distinctions lie between a “projection” and a “forecast.” Focusing on the near term, forecasts attempt to predict actual outcomes. Projections look further into the future and depend on stated assumptions as well as analysis of long-run trends. Nevertheless, projections are important for long-run planning. The main responsibility of the BLS projections is to produce comprehensive and trustworthy information to help people choose careers. While the projections may not exactly match the actual data in the target year, they should capture the long-run trend, direction, and growth of the labor force, the macroeconomy, and industry. In addition, the growth of industries and labor force subcomponents of age, sex, race, and ethnic origin should be ranked relatively well. Because BLS is interested in the long-run characteristics of the economy, BLS assumed an unemployment rate thought to be consistent with a mature business cycle expansion.

Business cycle dynamics affect the path of the U.S. labor market and economy. The Great Recession was one of two recessions since the turn of the century and had the greatest impact. The first decade of this century was characterized by a global war on terrorism and bubbles followed by busts in the “high-tech,” financial, and housing markets. Such “shocks” to the economy can manifest as contractionary periods during the business cycle. Because projections depend on the underlying assumptions and because BLS assumed an unemployment rate, and therefore employment, that was consistent with a mature business cycle expansion, evaluating these projections in the context of the Great Recession was challenging. The long-run trends of the U.S. economy after the 2007–09 recession will not be clear for some time. Therefore, determining which portions of the errors in the 2008 and 2010 projections are due to business cycle dynamics is difficult as opposed to determining which portions will persist in the long run because of structural changes in the economy.1

The BLS 2006 projections are presented along with the projections to 2008 and 2010, allowing for the comparison of performance before, during, and after the Great Recession of 2007–09.2 Generally, BLS projections were consistent for the target years 2006, 2008, and 2010. However, the 2006 projections were much closer to the actual outcomes than were the 2008 and 2010 projections.

In addition to challenges presented by the recession, the introduction of a new industrial classification system and broad revisions to the occupational classification systems presented further difficulties in evaluating these sets of projections.3 Because of the revisions, projected industry employment data are limited to 17 aggregate sectors of the nearly 300 detailed industries published.4 Evaluation of employment by occupation for these sets of projections was omitted entirely because of the revised classification system.

Additional approaches were used to meaningfully evaluate these sets of projections. First, where data are available, the mean absolute error made by other projection publications is compared with the error made by BLS. Since no comparison data were available for the majority of publication series, BLS projections also are weighed against the performance of a naïve model.5 Finally, analyzing employment by shares and levels helps determine whether BLS projections provided accurate information for selecting industries in which to pursue a career.

In broad strokes, the BLS projections performed well. The mean absolute errors in the BLS projections were very close to those of other government agencies. Violations in the assumptions underlying the projections, including effects of the 2007–09 recession, proved challenging to not only the BLS projections but also the projections made by other sources as well as the naïve model. BLS outperformed the naïve model for the majority of the variables evaluated here.

BLS continues to perform well in projections of the labor force. BLS anticipated underprojections of population from the U.S. Census Bureau and offset them with slight adjustments to the BLS-projected labor force participation rates. These adjustments resulted in accurate projections of the labor force for each of the three sets of projections to 2006, 2008, and 2010. BLS correctly anticipated changing demographic trends that had important ramifications for the growth of the labor force, including the slowing growth in participation rates of women and impacts of the aging of baby boomers.

Results of the macroeconomic model, including gross domestic product (GDP), the unemployment rate, and employment growth in aggregate employment and productivity, were mixed because of the length and severity of the Great Recession. Projections to 2006 and 2008 were accurate, while the 2010 projections were much further from actual outcomes. Although most of the discrepancy was due to the recession, some was attributed to an assumed unemployment rate of 4 percent and rapid productivity growth in the 2010 projections. BLS adopted a more formal “full employment” economy assumption within its model, starting with the 2002–12 projections.6 Keeping the projected unemployment rate closely tied to the nonaccelerating inflation rate of unemployment (NAIRU) should help ensure that measures in future publications will be more reasonable.

At the aggregate level, projections for employment growth in each of the evaluated periods were expected to slow from the previous 10-year period.7 However, the slowdown in job growth was steeper than anticipated in the projections to 2006 and 2008, and the United States experienced an outright decline in employment between 2000 and 2010. Within the detailed industry sectors, the projections generally steered customers in the correct sector or industry as evidenced in the share analysis. BLS correctly expected that U.S. employment was moving toward a larger share of service sector jobs, with fewer opportunities in manufacturing. However, the magnitude of the decline in manufacturing was greatly underestimated. In comparing projections with actual data, the largest errors in the projections, aside from manufacturing, were in the mining and construction sectors. Mining experienced a turnaround from being a declining industry to being a growing industry largely because of an unexpected rise in the price of oil. Increased global demand and the commercial viability of fracking drilling techniques were the reasons for the rise in oil price. The housing bubble and bust severely affected construction employment, falling from its peak in 2007 to all-time record lows in just a few years. BLS, however, outperformed the naïve model for both the mining and construction sectors.

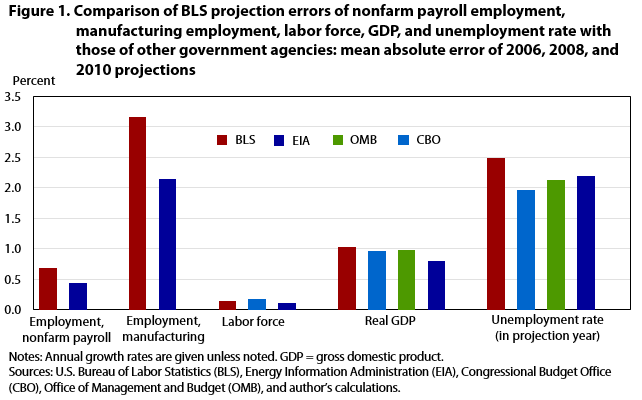

Performance of projections and forecasts is often gauged relatively; that is, the error of a given projection is compared with the error of another agency or firm. BLS publishes an outlook for many macroeconomic variables, numerous detailed labor force categories, and hundreds of industries and occupations. Most of these variables are not published elsewhere. A few of the more important aggregate measures that substantially affect the detailed employment projections are available for comparison. These measures include the projections of nonfarm payroll employment, manufacturing employment, the labor force, the GDP, and the unemployment rate. The mean absolute error of the BLS projection for each of these variables is presented along with those of three other government agencies: the Congressional Budget Office (CBO), the Office of Management and Budget (OMB), and the Energy Information Administration (EIA).8 (See figure 1.) Despite differences in assumptions, technique, and purpose, the mean absolute errors for agency projections were nearly equivalent to BLS projections for all categories.9 The BLS projections to 2010 were more optimistic than other agency projections and therefore contained slightly larger errors, whereas projections 2006 and 2008 were more comparable in scale.

| Variable | Projection source | Mean absolute value |

|---|---|---|

| Employment, nonfarm payroll (annual growth rate) | BLS | 0.7 |

|

| EIA | 0.4 |

|

| Actual | — |

| Employment, manufacturing | BLS | 3.2 |

|

| EIA | 2.2 |

|

| Actual | — |

| Labor force annual growth rate | BLS | 0.1 |

|

| CBO | 0.2 |

|

| EIA | 0.1 |

|

| Actual | — |

| GDP real (annual growth rate) | BLS(1) | 1 |

|

| CBO | 1 |

|

| OMB | 1 |

|

| EIA | 0.8 |

|

| Actual | — |

| Unemployment rate | BLS | 2.5 |

|

| CBO | 2 |

|

| OMB | 2.1 |

|

| EIA | 2.2 |

|

| Actual | — |

| Notes: (1) BLS data are not rebased for this table.They were published in 1992 & 1996 making them comparable to other comparisons. Notes: Annual growth rates are given unless noted. GDP = gross domestic product. Sources: U.S. Bureau of Labor Statistics (BLS), Energy Information Administration (EIA), Congressional Budget Office (CBO), Office of Management and Budget (OMB), and author’s calculations. | ||

The most notable discrepancy occurred with the 2010 assumption for the unemployment rate. BLS assumed this rate to be 4.0 percent, while other agencies expected between 4.5 percent and 5.2 percent. When these projections were being made, BLS was using a projected unemployment rate equivalent or very close to the previous peak in the business cycle. The base year, 2000, for the 2010 projections was the peak of a business cycle when the unemployment rate fell to 4.0 percent. Research now indicates that this rate was likely a lower than sustainable rate as measured by NAIRU.10 Starting with the 2002–12 projections, BLS more formally adopted a “full employment” economy assumption in which the unemployment rate was at or near NAIRU. While the unemployment rate was optimistic in the 2010 projections, the BLS error was nearly equivalent to the errors of the other agencies in the 2006 and 2008 projections.

Given the low unemployment rate assumption, the BLS projected growth rate of GDP to 2010 contained a slightly higher margin of error. However, BLS performed best among the agencies for projecting the GDP growth rate to 2006 and 2008. On average, over the three sets of projections, the BLS mean absolute error in the projected growth rate of GDP was nearly equivalent to errors of other agencies. Errors in the BLS-projected annual growth rate of the labor force were very small, averaging just 0.1 percent, about the same as those errors CBO and EIA projected. Most of the existing error stemmed from the 2010 projections because the participation rate declined rapidly between 2008 and 2010. Because the labor force is an important supply-side factor in future economic activity, a highly accurate projection is an important foundation for projecting the macroeconomy and employment.

The BLS employment outlook was more optimistic than that of EIA. Neither expected the extent of the declines in manufacturing that occurred in recent years. EIA, however, correctly projected declines in manufacturing employment for all three 10-year intervals. BLS determined that the market was at its bottom and projected that very slight increases would occur in manufacturing employment between 1998–2008 and 2000–10. The mean absolute error for the EIA projection of nonfarm payroll employment also was smaller than the BLS error, 0.4 percentage point compared with 0.7 percentage point. BLS consistently expected faster employment growth and a lower unemployment rate than did EIA in each of the three sets of BLS projections.

Comparable projections are not available for most publication series, including the detailed sectors of both employment and the labor force. As an alternative evaluation measure, BLS uses a naïve model for comparison purposes. A naïve model is any model that is simple to estimate and does not require sophisticated systems or processes. The more elaborate BLS model should outperform a naïve model for a majority of the variables presented.

The naïve model used here is a 10-year, two-point model based on the growth rate exhibited in the previous 10-year period. In other words, we assume that the growth rate exhibited over the previous decade will persist over the projected period. We test that BLS projections outperform the naïve model in at least half the variables presented. To do so, we treat each subaggregate variable in table 1 as a binary outcome equal to 1 when the mean absolute error of the BLS projection is smaller than the naïve error and otherwise equal to zero. As shown in the following equation, we then use a t-statistic to test the null hypothesis that the sample mean for the binary variable is less than or equal to 0.5:

Where  is the number of variables BLS outperformed the naïve model divided by the number (N) of variables presented, and

is the number of variables BLS outperformed the naïve model divided by the number (N) of variables presented, and  is the sample standard deviation for the binary/Bernoulli variable, √(x ∗ (1 –

is the sample standard deviation for the binary/Bernoulli variable, √(x ∗ (1 –  )). The p-value shows that our findings are significant at the 5-percent level. We therefore reject the null hypothesis that BLS outperforms the naïve model less than half the time.

)). The p-value shows that our findings are significant at the 5-percent level. We therefore reject the null hypothesis that BLS outperforms the naïve model less than half the time.

Civilian noninstitutional population. At BLS, the projections process begins with the outlook for the future size and composition of the population. (See figures 2 and 3.) BLS relies on the U.S. resident population projections from the U.S. Census Bureau for 136 categories for age, race, gender, and ethnic origin. BLS then converts the resident population projections to a civilian noninstitutional population (CNIP) concept. By definition, CNIP includes all persons 16 years of age and older residing in the 50 states and the District of Columbia who are not inmates of penal or mental institutions and are not in the Armed Forces. The 1996–2006 BLS outlook was derived on the basis of population projections that the U.S. Census Bureau published in 1995, whereas the 1998–2008 and 2000–10 projections used U.S. Census Bureau population projections done in 1997.11 All three sets of projections were based on the 1990 decennial census population.

| Year | Historical | 1996–2006 projections | 1998–2008 projections | 2000–10 projections |

|---|---|---|---|---|

| Civilian noninstitutional population | ||||

| 1994 | 196,814 | — | — | — |

| 1995 | 198,584 | — | — | — |

| 1996 | 200,591 | 200,591 | — | — |

| 1997 | 203,133 | 202,651 | — | — |

| 1998 | 205,220 | 204,711 | 205,220 | — |

| 1999 | 207,753 | 206,771 | 207,560 | — |

| 2000 | 212,577 | 208,831 | 209,901 | 212,577 |

| 2001 | 215,092 | 210,891 | 212,241 | 214,685 |

| 2002 | 217,570 | 212,951 | 214,581 | 216,793 |

| 2003 | 221,168 | 215,011 | 216,922 | 218,901 |

| 2004 | 223,357 | 217,071 | 219,262 | 221,009 |

| 2005 | 226,082 | 219,131 | 221,602 | 223,118 |

| 2006 | 228,815 | 221,191 | 223,942 | 225,226 |

| 2007 | 231,867 | — | 226,283 | 227,334 |

| 2008 | 233,788 | — | 228,623 | 229,442 |

| 2009 | 235,801 | — | — | 231,550 |

| 2010 | 237,830 | — | — | 233,658 |

| Labor force participation rates (percent) | ||||

| 1994 | 66.6 | — | — | — |

| 1995 | 66.6 | — | — | — |

| 1996 | 66.8 | 66.8 | — | — |

| 1997 | 67.1 | 66.9 | — | — |

| 1998 | 67.1 | 66.9 | 67.1 | — |

| 1999 | 67.1 | 67.0 | 67.1 | — |

| 2000 | 67.1 | 67.1 | 67.2 | 67.1 |

| 2001 | 66.8 | 67.2 | 67.3 | 67.1 |

| 2002 | 66.6 | 67.3 | 67.3 | 67.2 |

| 2003 | 66.2 | 67.4 | 67.4 | 67.2 |

| 2004 | 66.0 | 67.4 | 67.4 | 67.2 |

| 2005 | 66.0 | 67.5 | 67.5 | 67.3 |

| 2006 | 66.2 | 67.6 | 67.5 | 67.3 |

| 2007 | 66.0 | — | 67.6 | 67.4 |

| 2008 | 66.0 | — | 67.6 | 67.4 |

| 2009 | 65.4 | — | — | 67.5 |

| 2010 | 64.7 | — | — | 67.5 |

| Labor force | ||||

| 1994 | 131,056 | — | — | — |

| 1995 | 132,304 | — | — | — |

| 1996 | 133,943 | 133,943 | — | — |

| 1997 | 136,297 | 135,433 | — | — |

| 1998 | 137,673 | 136,924 | 137,673 | — |

| 1999 | 139,368 | 138,414 | 139,363 | — |

| 2000 | 142,583 | 139,905 | 141,054 | 140,863 |

| 2001 | 143,734 | 141,395 | 142,744 | 142,549 |

| 2002 | 144,863 | 142,885 | 144,434 | 144,235 |

| 2003 | 146,510 | 144,376 | 146,125 | 145,920 |

| 2004 | 147,401 | 145,866 | 147,815 | 147,606 |

| 2005 | 149,320 | 147,357 | 149,505 | 149,292 |

| 2006 | 151,428 | 148,847 | 151,195 | 150,978 |

| 2007 | 153,124 | — | 152,886 | 152,664 |

| 2008 | 154,287 | — | 154,576 | 154,349 |

| 2009 | 154,142 | — | — | 156,035 |

| 2010 | 153,889 | — | — | 157,721 |

| Sources: U.S. Census Bureau and U.S. Bureau of Labor Statistics. | ||||

| Projection years | Base year | Projected | Actual |

|---|---|---|---|

| Labor force | |||

| 1996–2006 | 133,943 | 148,847 | 151,428 |

| 1998–2008 | 137,673 | 154,576 | 154,287 |

| 2000–10 | 142,583 | 157,721 | 153,889 |

| Civilian noninstitutional population | |||

| 1996–2006 | 200,591 | 221,191 | 228,815 |

| 1998–2008 | 205,220 | 228,623 | 233,788 |

| 2000–10 | 212,577 | 233,658 | 237,830 |

| Labor force participation rates (percent) | |||

| 1996–2006 | 66.80 | 67.60 | 66.20 |

| 1998–2008 | 67.10 | 67.60 | 66.00 |

| 2000–10 | 67.10 | 67.50 | 64.70 |

| Sources: U.S. Census Bureau and U.S. Bureau of Labor Statistics. | |||

Challenges were revealed when these population projections were compared with actual published data because differences between the 1990 and 2000 censuses of the population are large. (See figure 2A). The 2000 census counted the U.S. resident population as 281.4 million people, a 13.2-percent increase over the 1990-census population of 248.7 million. Numerically, the increase was 32.7 million, the largest increase between any two censuses. The difference between the 2000 census estimates and projections was a considerable 6.8 million. The higher population count was reflected most notably in the count of men, in the count of Hispanics, and within the 18- to 29-year-old-age category.12 The difference in population weights between the 1990 and 2000 censuses resulted in the underprojection of CNIP in all three sets of BLS projections. Because young Hispanic men participate in the labor force at higher-than-average rates, underestimating the immigration of young Hispanic men by the U.S. Census Bureau resulted in larger errors in the BLS projections of labor force and in the labor force participation rate.

Evaluation of CNIP projections was complicated not only because of the increased population count in the 2000 census but also because of changes in the classification of race categories. The race categories that OMB established before the 2000 census were “White,” “Black,” and “Asian and other.” The 2000 census, for the first time, allowed respondents to classify themselves in more than one racial category, adding a multiple race group. The new race categories in the 2000 census became “White only,” “Black only,” “Asian only,” and “All other races,” which included the multiple race groups combined with American Indian, Alaska Native, Native Hawaiian, and Pacific Islander. Therefore, a comparison of racial categories with currently published data is not evaluated here.

Despite the differences in census counts, the population projections were close to the actual outcome. (See figure 3B). Differences between the projection of CNIP and the now-published actual data were the

· 2006 projection of the populations underprojected by 7.6 million, or 3.4 percent;

· 2008 projection of the population underprojected by 5.2 million, or 2.3 percent; and

· 2010 projection of the population underprojected by 4.2 million, or 1.8 percent.

For growth rates, the 1996–2006 projections anticipated 1.0-percent annual growth for the CNIP, 0.3 percentage point lower than that which occurred. The 1998–2008 projections estimated 1.1-percent annual growth, which was 0.2 percentage point lower than the actual growth, and the 2000–10 projections expected 1.0-percent growth, 0.1 percentage point lower than the actual rate. The CNIP projection underperformed the naïve model.

Labor force participation rate. After continual expansion in the 1970s, 1980s, and 1990s, the labor force participation rate peaked at 67.1 percent over the 1997–2000 period. Following the 2001 recession, it declined to 66.0 in 2004 and remained close to that level through 2008 (see figure 2B). Over the next 6 years and specifically after the recession of 2007–09, the labor force participation rate declined substantially reaching 64.7 percent in 2010 and falling to 62.9 percent in 2014. When the 1996, 1998, and 2000 projections were being made, participation rates were still in the midst of a long-term trend of growth. BLS correctly expected that this trend would reverse, projecting first a flattening and then a slight decline over the coming decade. Specifically, BLS correctly expected the following changes to long standing trends in the labor force participation rates:

· The participation rate of both women and men would slow. The rate for women would continue to grow at a slightly faster rate than the rate for men.

· The participation rate of youths (16 to 24 years old) and their share of the labor force would decline.

· The participation rate of prime-age workers (25 to 54 years old) would flatten while their share of the labor force would decline.

Although these changes in trends were correctly anticipated, BLS overprojected the labor force participation rate in all three sets of projections. At least some of the error is accounted for by BLS upward adjustments to the projected labor force participation rates for what was believed to be an underestimation of the population as discussed previously. The participation rate projected for 2006 was 67.6 but the actual rate was 66.2. (See figure 3C.) For 2008, BLS projected a 67.6-percent participation rate, higher than the 66.0 percent realized. The 2010 rate also was overprojected at 67.5 percent since the actual rate fell more substantially to 64.7 percent after the great recession of 2007–09. The BLS projected CNIP and labor force projected data were closer to actual data than were the BLS-projected labor force participation rates for the three sets of the projections. Although the projections of the labor force participation rates were consistently high, BLS still outperformed the naïve model by 0.1 percentage point.

Labor force. To derive labor force projections, BLS multiplies the projected participation rates by their respective CNIPs. The labor force categories are then summed to get the aggregate labor force.13 The projected labor force is an important input and constraint for the rest of the projections process, particularly those parts of the process used to project GDP and aggregate employment measures.

| Year | Annual | 10-year average annual growth (percent) | Projections (2006, 2008, and 2010) |

|---|---|---|---|

| 1957 | 66,929 | 1.21 | — |

| 1958 | 67,639 | 1.1 | — |

| 1959 | 68,369 | 1.1 | — |

| 1960 | 69,628 | 1.13 | — |

| 1961 | 70,459 | 1.28 | — |

| 1962 | 70,614 | 1.29 | — |

| 1963 | 71,833 | 1.32 | — |

| 1964 | 73,091 | 1.39 | — |

| 1965 | 74,455 | 1.36 | — |

| 1966 | 75,770 | 1.31 | — |

| 1967 | 77,347 | 1.46 | — |

| 1968 | 78,737 | 1.53 | — |

| 1969 | 80,734 | 1.68 | — |

| 1970 | 82,771 | 1.74 | — |

| 1971 | 84,382 | 1.82 | — |

| 1972 | 87,034 | 2.11 | — |

| 1973 | 89,429 | 2.22 | — |

| 1974 | 91,949 | 2.32 | — |

| 1975 | 93,775 | 2.33 | — |

| 1976 | 96,158 | 2.41 | — |

| 1977 | 99,009 | 2.5 | — |

| 1978 | 102,251 | 2.65 | — |

| 1979 | 104,962 | 2.66 | — |

| 1980 | 106,940 | 2.6 | — |

| 1981 | 108,670 | 2.56 | — |

| 1982 | 110,204 | 2.39 | — |

| 1983 | 111,550 | 2.23 | — |

| 1984 | 113,544 | 2.13 | — |

| 1985 | 115,461 | 2.1 | — |

| 1986 | 117,834 | 2.05 | — |

| 1987 | 119,865 | 1.93 | — |

| 1988 | 121,669 | 1.75 | — |

| 1989 | 123,869 | 1.67 | — |

| 1990 | 125,840 | 1.64 | — |

| 1991 | 126,346 | 1.52 | — |

| 1992 | 128,105 | 1.52 | — |

| 1993 | 129,200 | 1.48 | |

| 1994 | 131,056 | 1.44 | — |

| 1995 | 132,304 | 1.37 | — |

| 1996 | 133,943 | 1.29 | — |

| 1997 | 136,297 | 1.29 | — |

| 1998 | 137,673 | 1.24 | — |

| 1999 | 139,368 | 1.19 | — |

| 2000 | 142,583 | 1.26 | — |

| 2001 | 143,734 | 1.3 | — |

| 2002 | 144,863 | 1.24 | — |

| 2003 | 146,510 | 1.27 | — |

| 2004 | 147,401 | 1.18 | — |

| 2005 | 149,320 | 1.22 | — |

| 2006 | 151,428 | 1.23 | 1.1 |

| 2007 | 153,124 | 1.17 | — |

| 2008 | 154,287 | 1.15 | 1.2 |

| 2009 | 154,142 | 1.01 | — |

| 2010 | 153,889 | 0.77 | 1.1 |

| Source: U.S. Bureau of Labor Statistics. | |||

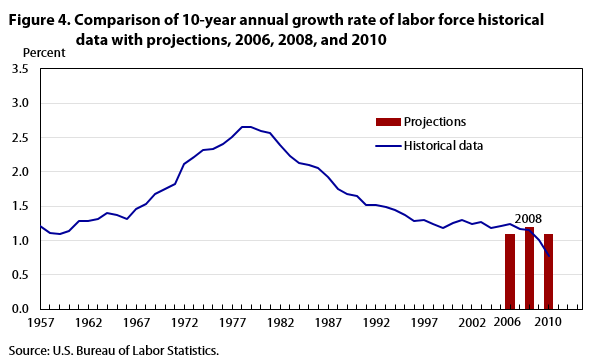

Changes to the labor force tend to happen gradually over long periods. The demographic composition of the population plays an important role in changes to the trends. For example, the baby-boom generation first entered the workforce in the 1970s, boosting the growth rate of the labor force. Moreover, women’s participation rates grew considerably in the 1970s and 1980s. These two trends worked together, increasing the growth rate of the labor force considerably to a peak 10-year compound annual rate of 2.6 percent over the 1970–80 period (see figure 4). Since then, the labor force growth has gradually but steadily slowed to half that rate, reaching 1.3 percent in 1990–2000. With the onset of the 2007–09 recession, the annual growth rate fell precipitously, reaching 0.8 percent over the 2000–10 decade. Projections of the labor force growth were very similar across the 2006, 2008, and 2010 projections. Because of the steep slowdown in labor force growth following the 2007–09 recession, the projections to 2006 and 2008 were much closer to the actual outcome than the projections to 2010.

As these projections were published, BLS and other population data users knew that the 2000 census would likely result in a higher population count. The labor force is a vital input to the economy because its growth represents the potential human capital available to produce U.S. goods and services. It is also a constraint because, as the population ages, fewer people are available to contribute to the labor force. Since labor force outlook is the key determinant of GDP and employment growth and therefore is critical in occupational and industry employment projections, BLS preferred to have the error in the projected participation rates rather than in the projected count of the labor force. As such, BLS subtly adjusted the labor force participation rate for the 30-to-64 years age categories, resulting in somewhat higher aggregate labor force participation rates.14 This choice reduced the error in the labor force projections while increasing the error in the projected participation rates.

BLS projections of the labor force came very close to the published estimates. The labor force was projected to increase by 1.1 percent annually over 1996–2006, only slightly slower than the 1.2 percent realized (see table 2). Over the 1998–2008 period, BLS marginally overprojected labor force growth at 1.2 percent, just 0.1 percentage point faster than what actually occurred. Over the 2000–10 period, BLS correctly expected the labor force growth to slow as a larger portion of the baby boomers moved into lower participation age cohorts rates. However, BLS anticipated that the long-run trend would occur gradually, declining only slightly to 1.0 percent over 2000–10 period. This projection was correct with growth rates exhibited in the first 8 years of the decade. However, over the last 2 years of the projection period, the labor force growth not only slowed but also posted an actual decline, pulling the growth rate over the entire 2000–10 decade down to 0.8 percent.

The absolute error in the BLS labor force projections was small. Among the projections of the labor force within the more detailed cohort data, BLS correctly expected several trends within the U.S. labor force. As baby boomers moved into their “golden years,” the growth rate of the labor force was correctly projected to slow. Also, the following trends were correctly anticipated:

· The aging population, decreasing fertility rates, and increasing life expectancies would result in an increase in the median age of the labor force.

· The labor force would grow more diverse. Minorities, particularly Hispanics, would increase their share in the U.S. labor force because of high fertility rates and increasing participation rates.

· The growth rate of women in the labor force would slow from previous decades but continue to increase slightly faster than the rate of men.

· The U.S. workforce would become more “age diverse” as the participation rate of older workers increased noticeably and their share of the population increased.

BLS projections regarding the labor force outperformed the naïve model in most cases, often by an impressive measure. (See table 2.) The growth rate projection of the labor force for women was especially improved with use of the BLS model. The prime 25- to 54-year-old age group as well as the 55-years-and-older group was also captured much more accurately by the BLS model than the naïve model. In fact, the average error by BLS on the prime age group was only 0.1 percentage point, a substantial improvement over the naïve model average error of 1.2 percentage points. The naïve model performed slightly more accurately than the BLS model for the race and ethnic categories, although the error in both models is largely attributable to the increased Hispanic count in the 2000 census.

The macroeconomic model provides projections of GDP, productivity, employment, and many other economic measures. These estimates then serve as constraints to the next step of the projections process: projecting jobs and output for detailed industries. Data Resources, Inc. (DRI), supplied the macroeconomic model software that BLS used in the 2006, 2008, and 2010 projections. BLS incorporated its assumptions and estimates for variables that include energy prices, unemployment, and demographic measures resulting in an independent BLS estimate that is based on the DRI model structure.

Within the macroeconomic model projections, the naïve model came closer to the actual GDP than did the BLS model. Some of the projections of the most important variables outperformed the naïve model, including projections of productivity, household employment, and nonfarm wage and salary employment. BLS correctly expected employment growth to slow in each of the three projected decades because of the aging population. However, the GDP projection was slightly more accurately captured with the use of the naïve model than with the BLS model. Much of the error within GDP stemmed from the BLS expectation that consumption would slow over the period. Financial bubbles and easy credit likely contributed to the unexpected growth. BLS oil price projections were more accurate than the naïve model oil price projections (see table 2).

Although turning points in the economy are notoriously difficult to anticipate, the long-run trend component of economic growth can be captured according to economic theory. Potential GDP provides an estimate of the sustainable output level that is attainable for the economy in the long run. Potential growth is constrained by availability of capital, labor, and technology. In a full-employment economy, GDP is roughly equivalent to its potential and the unemployment rate is at or very near NAIRU.

| Year | Annual unemployment rate | Assumed rate in projections (2006, 2008, and 2010) |

|---|---|---|

| 1950 | 5.3 | — |

| 1951 | 3.3 | — |

| 1952 | 3.0 | — |

| 1953 | 2.9 | — |

| 1954 | 5.5 | — |

| 1955 | 4.4 | — |

| 1956 | 4.1 | — |

| 1957 | 4.3 | — |

| 1958 | 6.8 | — |

| 1959 | 5.5 | — |

| 1960 | 5.5 | — |

| 1961 | 6.7 | — |

| 1962 | 5.5 | — |

| 1963 | 5.7 | — |

| 1964 | 5.2 | — |

| 1965 | 4.5 | — |

| 1966 | 3.8 | — |

| 1967 | 3.8 | — |

| 1968 | 3.6 | — |

| 1969 | 3.5 | — |

| 1970 | 4.9 | — |

| 1971 | 5.9 | — |

| 1972 | 5.6 | — |

| 1973 | 4.9 | — |

| 1974 | 5.6 | — |

| 1975 | 8.5 | — |

| 1976 | 7.7 | — |

| 1977 | 7.1 | — |

| 1978 | 6.1 | — |

| 1979 | 5.8 | — |

| 1980 | 7.1 | — |

| 1981 | 7.6 | — |

| 1982 | 9.7 | — |

| 1983 | 9.6 | — |

| 1984 | 7.5 | — |

| 1985 | 7.2 | — |

| 1986 | 7.0 | — |

| 1987 | 6.2 | — |

| 1988 | 5.5 | — |

| 1989 | 5.3 | — |

| 1990 | 5.6 | — |

| 1991 | 6.8 | — |

| 1992 | 7.5 | — |

| 1993 | 6.9 | — |

| 1994 | 6.1 | — |

| 1995 | 5.6 | — |

| 1996 | 5.4 | — |

| 1997 | 4.9 | — |

| 1998 | 4.5 | — |

| 1999 | 4.2 | — |

| 2000 | 4.0 | — |

| 2001 | 4.7 | — |

| 2002 | 5.8 | — |

| 2003 | 6.0 | — |

| 2004 | 5.5 | — |

| 2005 | 5.1 | — |

| 2006 | 4.6 | 5.4 |

| 2007 | 4.6 | — |

| 2008 | 5.8 | 4.7 |

| 2009 | 9.3 | — |

| 2010 | 9.6 | 4.0 |

| Source: U.S. Bureau of Labor Statistics. | ||

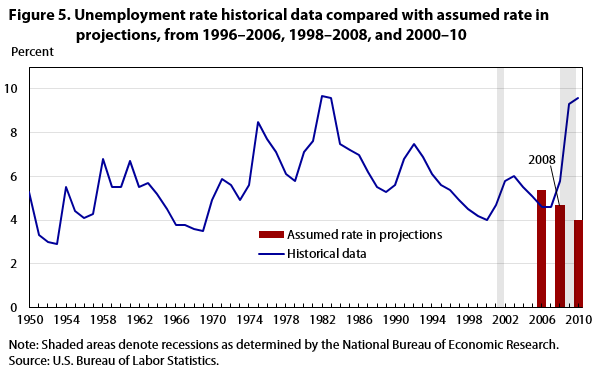

Instead of relying on a NAIRU estimate, BLS assumed that the unemployment rate would be consistent with the mature phase of the business cycle expansion in the 2006, 2008, and 2010 projections. (See figure 5.) The macroeconomic projections rested on a 5.4-percent unemployment rate in 2006, equivalent to the rate posted in 1996. The 2008 and 2010 projections were more optimistic with assumed unemployment rates of 4.7 and 4.0 percent, respectively, nearly equivalent to the rates posted in the base years of 1998 and 2000. When BLS made the 2010 projections, the United States was at the peak of the business cycle and the low unemployment rate was unsustainable as it was likely temporarily supported by demand stemming from the high-tech bubble.

According to now-published data, the United States reached an unemployment rate of 4.6 percent in 2006, 0.8 lower than assumed by the 1996 projections (see table 1). As the recession took hold, the unemployment rate edged up to 5.8 percent in 2008, 1.1 percent higher than assumed by the 2008 projections. By 2010, the unemployment rate reached 9.6 percent, a striking 5.6 percent higher than the assumption within the 2010 projections (see figure 5). Although some of the discrepancy between the 2010 projection and the actual unemployment rate was due to failure to adhere to a NAIRU-based assumption, most of the error was explained by cyclical decline and slack in the labor market. Had BLS used, for example, the CBO estimate for NAIRU within the 2010 projections, the error would have been roughly 1 percentage point lower.

Figure 6A depicts the historical time series of the 10-year compound annual growth rate of real GDP. Viewing average growth rates over 10-year periods removes much of the volatility attributable to the business cycle and provides a direct comparison between historical and projected data series. The annual growth rate of real GDP rose from 3.0 percent in the 1951–61 decade to a peak of 4.8 percent in 1958–68. Growth then quickly fell to roughly 3 percent and remained close to that level for 30 years, through the mid-2000s.

| Year | Real GDP | Nonfarm business labor productivity | Nonfarm employment historical data | |||

|---|---|---|---|---|---|---|

| 10-year annual growth | Projections (2006, 2008, and 2010) | 10-year annual growth | Projections (2006, 2008, and 2010) | 10-year annual growth | Projections (2006, 2008, and 2010) | |

| 1957 | — | — | 2.7 | — | 1.9 | — |

| 1958 | — | — | 2.7 | — | 1.4 | — |

| 1959 | — | — | 2.7 | — | 2.0 | — |

| 1960 | 3.5 | — | 2.2 | — | 1.8 | — |

| 1961 | 3.0 | — | 2.2 | — | 1.2 | — |

| 1962 | 3.2 | — | 2.5 | — | 1.3 | — |

| 1963 | 3.2 | — | 2.6 | — | 1.2 | — |

| 1964 | 3.8 | — | 2.7 | — | 1.7 | — |

| 1965 | 3.7 | — | 2.6 | — | 1.8 | — |

| 1966 | 4.2 | — | 3.0 | — | 2.0 | — |

| 1967 | 4.2 | — | 3.0 | — | 2.2 | — |

| 1968 | 4.8 | — | 3.1 | — | 2.8 | — |

| 1969 | 4.4 | — | 2.7 | — | 2.8 | — |

| 1970 | 4.2 | — | 2.7 | — | 2.7 | — |

| 1971 | 4.3 | — | 2.8 | — | 2.8 | — |

| 1972 | 4.2 | — | 2.7 | — | 2.9 | — |

| 1973 | 4.4 | — | 2.7 | — | 3.1 | — |

| 1974 | 3.7 | — | 2.2 | — | 3.0 | — |

| 1975 | 3.1 | — | 2.2 | — | 2.4 | — |

| 1976 | 2.9 | — | 2.2 | — | 2.2 | — |

| 1977 | 3.2 | — | 2.1 | — | 2.3 | — |

| 1978 | 3.2 | — | 1.9 | — | 2.5 | — |

| 1979 | 3.2 | — | 1.9 | — | 2.5 | — |

| 1980 | 3.2 | — | 1.7 | — | 2.5 | — |

| 1981 | 3.1 | — | 1.4 | — | 2.5 | — |

| 1982 | 2.4 | — | 1.0 | — | 2.0 | — |

| 1983 | 2.2 | — | 1.1 | — | 1.6 | — |

| 1984 | 3.0 | — | 1.5 | — | 1.9 | — |

| 1985 | 3.4 | — | 1.4 | — | 2.4 | — |

| 1986 | 3.3 | — | 1.4 | — | 2.3 | — |

| 1987 | 3.1 | — | 1.2 | — | 2.1 | — |

| 1988 | 3.0 | — | 1.3 | — | 2.0 | — |

| 1989 | 3.0 | — | 1.4 | — | 1.8 | — |

| 1990 | 3.2 | — | 1.6 | — | 1.9 | — |

| 1991 | 3.0 | — | 1.6 | — | 1.7 | — |

| 1992 | 3.5 | — | 2.1 | — | 1.9 | — |

| 1993 | 3.3 | — | 1.7 | — | 2.1 | — |

| 1994 | 3.0 | — | 1.6 | — | 1.9 | — |

| 1995 | 2.9 | — | 1.5 | — | 1.9 | — |

| 1996 | 2.9 | — | 1.5 | — | 1.9 | — |

| 1997 | 3.0 | — | 1.6 | — | 1.9 | — |

| 1998 | 3.1 | — | 1.7 | — | 1.8 | — |

| 1999 | 3.2 | — | 2.0 | — | 1.8 | — |

| 2000 | 3.4 | — | 2.1 | — | 1.9 | — |

| 2001 | 3.5 | — | 2.3 | — | 2.0 | — |

| 2002 | 3.4 | — | 2.3 | — | 1.8 | — |

| 2003 | 3.3 | — | 2.6 | — | 1.6 | — |

| 2004 | 3.3 | — | 2.8 | — | 1.4 | — |

| 2005 | 3.3 | — | 2.9 | — | 1.3 | — |

| 2006 | 3.2 | 2.5 | 2.8 | 1.2 | 1.3 | 1.4 |

| 2007 | 3.0 | — | 2.8 | — | 1.1 | — |

| 2008 | 2.5 | 1.9 | 2.5 | 1.4 | 0.8 | 1.5 |

| 2009 | 1.7 | — | 2.5 | — | 0.1 | — |

| 2010 | 1.5 | 3.2 | 2.5 | 2.8 | –0.1 | 1.4 |

| Note: Note: Gross domestic product (GDP) is in chained 2005 dollars. Sources: National Bureau of Economic Research, February 2013; U.S. Bureau of Labor Statistics; and authors’ calculations. | ||||||

GDP data are revised and anchored to a new base year every 5 years when BEA releases a set of benchmark input–output tables.15 Therefore, the BLS published projections were adjusted to make them comparable with currently published data. The historical data for the base year and the BLS projection figures for real GDP in table 1 have been rebased to 2005 dollars. Because of an aging population, BLS expected in each of the projections that the growth rate would slow compared with the previous decade. The growth rate of GDP was projected to decline to 2.5 percent over 1996–2006. Instead, 2006 proved to be a peak year in the business cycle and growth reached 3.2 percent over the decade. Just 2 years later, as the effects of the recession started to take hold, the annual growth rate for 1998–2008 slowed to 2.5 percent; BLS projected a lower 1.9-percent growth over the decade. The 2010 projections were compiled at the peak of the high-tech bubble, just before the 2001 recession. BLS took a more optimistic assumption in the unemployment rate and productivity expectations, resulting in a projection of 3.2-percent annual GDP growth over the 2000–10 decade. Instead, GDP slowed dramatically to 1.5 percent over the decade; registering a steep 1.0-percent decline from just 2 years earlier.

Projections for the productivity growth rate exhibit the widest range in projections of any of the variables evaluated in this article throughout the three publication cycles. BLS projected annual productivity growth of 1.2 percent between 1996 and 2006 and then jumped to a 2.8-percent projection in the 2000–10 publication (see figure 6B). BLS expected that the high annual productivity growth rates exhibited just before the “dot-com” bubble burst would be sustainable longer than what occurred. Computers and software were expected to contribute longer to productivity growth and the U.S. economy than they were able to attain. On the other hand, productivity provided a much bigger boost to the economy over 1996–2006 and 1998–2008 than what BLS projected. Together with the low unemployment rate assumed within the 2010 projections, this higher productivity projection led to an upward bias in the projection of GDP for the 2010 projections.

The 10-year average growth of nonfarm payroll employment stayed relatively stable between the late 1980s through 2002, between 1.7 and 2.1 percent (see figure 6C). Over the following decade, the United States endured two slow recoveries following the 2001 and 2007–09 recessions. According to most economic measures, particularly GDP, the effects of the 2001 recession were generally considered “mild.” However, the effects on the labor market were more pronounced. The economy did not reach its previous peak in employment until nearly 3.5 years after the onset of the recession. Thus, by the mid-2000s, the 10-year average annual growth rate of employment slowed to 1.3 percent, slightly below its historical trend. Nonfarm wage and salary employment never fully reached the prerecession peak before the onset of another recession, imposing additional drag on the job market. Employment did not fully recover to its prerecession levels until nearly 7 years after the onset of the 2007–09 recession. U.S. nonfarm wage and salary employment posted a decline between 2000 and 2010.

Much analysis and research have been written about the lackluster performance of the U.S. labor market in recent years compared with earlier historical behavior, but the story as to why this occurred is still unfolding. Globalization and the accompanying offshoring of labor-intensive jobs, consolidation of firms, and rapid productivity gains are three trends that have contributed to the continuation of output growth without the accompanying job growth usually expected. Performance varied greatly among industries, and some researchers suggest that much of the disparity is attributable to worker skill level; job opportunities exist for both high- and low-skilled jobseekers, whereas middle-skilled workers are being “squeezed out.” Middle-skilled workers may include workers who once did repetitive tasks that machines now do.16 This period of structural change proves challenging in evaluating employment projections.

The projected annual growth rate of nonfarm payroll employment for the projections evaluated here was expected to increase between 1.3 and 1.4 percent annually, a narrow range. BLS correctly expected that over each of the analyzed sets of projections, the employment growth rate would continue its trend of slowing down compared with the growth rate of previous decades. The 2006 projections were near the realized growth rate of 1.3 percent. Actual annual growth then slowed to 0.8 percent over 1998–2008 and then fell by 0.1 percent annually over the 2000–10 decade.

BLS estimated models for hundreds of detailed industries that were then summed to subsectors and sectors. Detailed industry projections were constrained to sum to the total nonfarm wage and salary employment provided by the macroeconomic model. Tables 1 and 2 include estimates for nonfarm wage and salary employment and nonagricultural wage and salary workers. These measures vary slightly in definition. The first, nonfarm wage and salary workers, is projected by the macroeconomic model and is defined in the same way as the CES published estimate. The second, nonagricultural wage and salary workers, is the sum of all industry subsectors listed in the table. The nonagricultural workers measure does not include logging.17 The remaining differences between the macroeconomic solution for total nonagricultural wage and salary workers and the sum of the individual industry employment totals are due to the North American Industrial Classification System (NAICS) to Standard Industrial Classification (SIC) conversion process. The employment totals also may be slightly different from the original publication employment totals because of the issues previously mentioned.

Since the macroeconomic model overprojected U.S. employment, industry sectors also tended to be projected higher than what was realized, especially within the 2010 projections. Given the upward bias in the projections of employment, the following are relevant questions in analyzing the industry employment projections: Did the projections generally steer people in the right directions in their career choices? Did the sectors that were expected to grow actually grow or did they instead decline? Was relative growth by sector accurately captured within the projections? To address these questions, we compare the industry employment projections with the actual data posted but also evaluate directional change and share analysis by industry sector.

Changes to classification systems of both industries and occupations presented considerable challenges in evaluating these sets of projections. BLS decided against reviewing projections of occupations because the Standard Occupation Classification System (SOC) underwent major revisions in 2002. Mapping the current occupational data to the old coding system would require broad assumptions, and the resulting analysis would not be meaningful. A new industrial classification system was adopted for industry employment estimates in 2002. The projections prior to 2002–12 were published on the basis of industries as they were defined by the old SIC codes. BLS converted currently published industry employment data from the current NAICS back to SIC categories. This conversion was done by using a distributional mapping from one period in which data were collected under both classification systems in March 2001. Government and private households were converted on the basis of written definitions since no crosswalk is available. In converting from NAICS to SIC, greater variability exists among individual industries compared with sectors and subsectors. Therefore, we analyze only the major sectors of detail, 17 aggregate industries rather than the roughly 200 industries published within the projections publications.

BLS correctly anticipated the directional change of the majority of the labor market within the 2006 and 2008 projections. The broad sweeping declines in U.S. employment over 2000 to 2010 would not be expected in the BLS projections because of the assumption that the economy is not in a recession in the target year. The service-producing sector, representing 83–85 percent of U.S. employment in the 2006–10 period, was correctly projected to experience continued growth over the 1996–2006 and 1998–2008 decades. The only incorrect projection of directional change within the service subsectors in the 2006 and 2008 projections were declines in the relatively small industries of communication and utilities. The largest directional error was the belief, in all three sets of projections, that manufacturing had reached its trough and would stay nearly flat over the projection period. Instead, job losses in the manufacturing sector continued to decline at a much faster pace. BLS also incorrectly expected that the mining industry would continue its long-run decline. Instead, mining employment in the United States turned around and started to experience growth as oil prices rose dramatically and technological innovation allowed the mining sector to use more domestic resources than had been anticipated. Overall, the anticipated direction of growth by BLS was more accurate in the 2006 and 2008 projections than in the 2010 projections because of the recessionary effects resulting in many unexpected declines.

Projections of industry employment resulted in sizable errors for both the BLS and the naïve models. Again, in both models, errors for 2008 and 2010 were much larger than those errors for 2006. BLS was more accurate than the naïve model in roughly half the sectors (see figure 7). However, the improvements in accuracy tended to be larger within the BLS model than the naïve model. Where the BLS model outperformed naïve model, the improvement was on average more than twice as large as when the naïve model had improved results. For example, the mean absolute error of the BLS model for construction was 0.9 percentage point smaller than the error of the naïve model. However, within the manufacturing projections, the naïve model contained a 0.4-percentage-point smaller error. The BLS model substantially outperformed the naïve model in four sectors: mining; construction; finance, insurance, and real estate; and federal government. The only subsectors for which the naïve model markedly outperformed the BLS model were communications and utilities.

| Industry (all wage and salary workers) | BLS absolute error | Naïve absolute error | Mean absolute error | |||||

|---|---|---|---|---|---|---|---|---|

| 2006 | 2008 | 2010 | 2006 | 2008 | 2010 | BLS | Naïve | |

| Goods | 0.69 | 1.71 | 4.01 | 0.00 | 1.24 | 4.15 | 2.14 | 1.80 |

| Mining | 3.45 | 4.09 | 2.99 | 5.05 | 5.45 | 5.28 | 3.51 | 5.26 |

| Construction | 2.42 | 0.65 | 3.36 | 3.66 | 0.90 | 4.48 | 2.14 | 3.01 |

| Manufacturing | 2.06 | 2.88 | 4.55 | 1.57 | 2.36 | 4.33 | 3.16 | 2.75 |

| Durable | 1.57 | 2.79 | 4.94 | 0.55 | 2.01 | 4.91 | 3.10 | 2.49 |

| Nondurable | 2.80 | 3.01 | 3.93 | 2.98 | 2.88 | 3.42 | 3.25 | 3.09 |

| Service | 0.19 | 0.55 | 1.39 | 0.20 | 0.49 | 1.54 | 0.71 | 0.75 |

| Transportation, communications, and utilities | 0.89 | 1.47 | 3.13 | 0.86 | 1.39 | 3.05 | 1.83 | 1.77 |

| Transportation | 0.75 | 1.05 | 2.76 | 0.86 | 1.41 | 3.03 | 1.52 | 1.76 |

| Communications | 0.33 | 2.56 | 4.41 | 0.30 | 1.32 | 4.24 | 2.43 | 1.95 |

| Utilities | 3.77 | 1.84 | 2.82 | 2.93 | 1.42 | 0.59 | 2.81 | 1.64 |

| Trade | 0.11 | 0.32 | 1.29 | 0.07 | 0.33 | 1.66 | 0.57 | 0.69 |

| Wholesale | 0.48 | 0.58 | 2.04 | 0.04 | 0.50 | 2.31 | 1.03 | 0.95 |

| Retail | 0.28 | 0.24 | 1.07 | 0.08 | 0.28 | 1.48 | 0.53 | 0.61 |

| Finance, insurance, and real estate | 0.77 | 0.30 | 0.67 | 1.25 | 1.82 | 3.30 | 0.58 | 2.12 |

| Other Service | 0.73 | 1.07 | 2.00 | 0.26 | 0.74 | 1.81 | 1.27 | 0.94 |

| Government | 0.32 | 0.38 | 0.02 | 0.13 | 0.57 | 0.39 | 0.24 | 0.36 |

| Federal | 0.23 | 0.80 | 1.27 | 0.27 | 1.78 | 3.50 | 0.76 | 1.85 |

| State | 0.34 | 0.32 | 0.15 | 0.19 | 0.41 | 0.02 | 0.27 | 0.21 |

| Source: U.S. Bureau of Labor Statistics. | ||||||||

BLS overprojected the goods sectors by nearly 7 percent in 2006, more severely by 15.8 percent in 2008, and 33.4 percent in 2010. The goods sector of the U.S. economy, including mining, construction, and manufacturing, changed dramatically between the time the BLS projections were published and the target years. As global demand increased, oil prices rose, contributing to a turnaround in employment in the U.S. mining sector. The construction sector was greatly affected by the housing bubble and bust. Meanwhile, manufacturing employment was heavily affected by increased global competition for labor-intensive jobs, a change in the types of jobs within the manufacturing industries, and rapid productivity gains. The recession accelerated the decline in several industries; computers, communications, and apparel subsectors saw the steepest declines.

Employment in the U.S. mining sector declined over the decades leading up to the three sets of projections. BLS anticipated that this decline would slow considerably but did not expect the turnaround that ensued. As a result, the mining sector grew 30 to 40 percent more than anticipated within the BLS projections, mostly because of an increase in the price of oil. Although both the BLS and naïve models expected a decline over the projection period, BLS expected less contraction, improving its performance over the naïve results.

Construction was underprojected by 21.1 percent in 2006 as employment was likely still supported by bubble-induced demand (see figure 8). The 2008 projection was only 6.2 percent over the actual outcome, similar to the error in the overall economy. As housing starts hit record lows in 2010 and construction employment dropped substantially, BLS overprojected jobs in the construction sector by 40.1 percent. The BLS model notably outperformed the naïve model for the construction sector in each of the three sets of projections, by an average of nearly 1 percentage point.

| Year | Total Nonfarm | Projections (2006, 2008, and 2010) | Construction | Projections (2006, 2008, and 2010) | Manufacturing | Projections (2006, 2008, and 2010) |

|---|---|---|---|---|---|---|

| 1990 | 109,487 | — | 5,263 | — | 17,695 | — |

| 1991 | 108,377 | — | 4,780 | — | 17,068 | — |

| 1992 | 108,745 | — | 4,608 | — | 16,799 | — |

| 1993 | 110,876 | — | 4,779 | — | 16,774 | — |

| 1994 | 114,333 | — | 5,095 | — | 17,020 | — |

| 1995 | 117,336 | — | 5,274 | — | 17,241 | — |

| 1996 | 119,757 | — | 5,536 | — | 17,237 | — |

| 1997 | 122,853 | — | 5,813 | — | 17,419 | — |

| 1998 | 126,033 | — | 6,149 | — | 17,560 | — |

| 1999 | 129,098 | — | 6,545 | — | 17,322 | — |

| 2000 | 131,881 | — | 6,787 | — | 17,263 | — |

| 2001 | 131,919 | — | 6,826 | — | 16,441 | — |

| 2002 | 130,450 | — | 6,716 | — | 15,259 | — |

| 2003 | 130,100 | — | 6,735 | — | 14,509 | — |

| 2004 | 131,509 | — | 6,976 | — | 14,315 | — |

| 2005 | 133,747 | — | 7,336 | — | 14,227 | — |

| 2006 | 136,125 | 137,093 | 7,691 | 5,900 | 14,155 | 18,108 |

| 2007 | 137,645 | — | 7,630 | — | 13,879 | — |

| 2008 | 136,852 | 144,526 | 7,162 | 6,535 | 13,406 | 18,684 |

| 2009 | 130,876 | — | 6,016 | — | 11,847 | — |

| 2010 | 129,917 | 152,447 | 5,518 | 7,522 | 11,528 | 19,047 |

| 2011 | 131,497 | — | 5,533 | — | 11,726 | — |

| 2012 | 133,739 | — | 5,641 | — | 11,919 | — |

| Source: U.S. Bureau of Labor Statistics. | ||||||

The projection of manufacturing sector jobs leveling off is the largest and most notable error of industry employment within these sets of projections (see figure 8C). Employment in the U.S. manufacturing sector peaked just before 1980 and then fell by a little more than 10 percent by the mid-1980s. Employment stayed in a relatively narrow range before falling somewhat after the 2001 recession and again much more precipitously following the 2007 recession. Since employment was fairly stable from the mid-1980s through 2001, BLS expected that within each of the three sets of projections, manufacturing would stay nearly flat. Instead, an unexpected trend of offshoring of labor-intensive work, rapid productivity growth, and recession impacts resulted in manufacturing employment declining by 17 to 23 percent over the projection periods. Productivity led to output growth in the manufacturing sector consistent with long-run trends amidst the rapid declines in employment. The manufacturing sector proved problematic for both the BLS and naïve models; however, the naïve model posted slightly smaller errors.

While the goods sectors experienced dramatic changes, the service sector was relatively more stable and better captured by the projections. BLS projections to 2006, 2008, and 2010 largely expected services, as a whole, to grow in line with rates experienced over the previous 10-year periods. Therefore, the naïve and BLS models contain nearly equivalent error measures.

Growth in the communications subsector increased rapidly over the late 1990s. This subsector was one of the most affected by the dot-com boom and bust. Consolidation and bundling of television, Internet, and telephone services over the following decade also may have contributed to declines in employment within this sector. BLS projected a 0.1-percent average annual decline over 1996–2006, nearly equivalent to the 0.2-percent growth experienced. Projections for 1998–2008 and 2000–10 expected growth to pick up to 1.5 and 0.8 percent, respectively. Instead, this industry lost jobs by 1.0 percent annually over 1998–2008 and 3.6 percent over 2000–10. BLS expected that the increased growth in the last couple historical years would persist over the projection period. Therefore, the naïve model outperformed BLS, improving the mean absolute error by 0.5 percentage point.

The utilities subsector also was expected to grow across all periods, which instead consistently declined. Technology that is more efficient resulted in productivity growth for the subsector, thereby requiring fewer employees for a given output level. The mean absolute error within the naïve model was 1.2 percentage points lower per year than that within the BLS projections. Communications and utilities were the only detailed subsectors for which the naïve model performed more accurately than the BLS model.

The trade sector was expected to follow the previous 10-year compound annual growth rate over the projected period within the 2006 and 2008 projections at 1.1 and 1.2 percent, respectively. The 2010 projections expected that the growth of 1.6 percent exhibited over 1990–2000 would slow slightly to 1.3 percent over the following decade. However, the sector posted a very slight decline between 2000 and 2010. Since BLS expected historical growth would slow from 2000–10, it slightly outperformed the naïve model.

The BLS model greatly outperformed the naïve model for the finance, insurance, and real estate sector, with a 1.5-percent improvement in the mean absolute error on the annual growth rate. Finance, insurance, and real estate was projected to continue growing but at a much slower rate than posted over the previous historical decade in each of the projection publications. Finance, insurance, and real estate employment slowed from 3.1 percent annually over 1986–96 to 1.8 percent over 1996–2006 but did not quite fall to the 1.0 percent that BLS projected. The bubble in the financial sector may have supported some of the employment over the period. Projections to 2008 were accurate in their expected slowdown in growth rates. On the other hand, 2000–10 projections expected growth to slow from 3.5 percent over 1990–2000 to 0.8 percent over 2000–10. The finance, insurance, and real estate sector slowed even further than the projected amount to 0.2-percent annual growth over the decade.

The "other services" sector was consistently projected to grow slightly faster over the projected decade than over the previous 10 years. While the projections to 2006 were close to the actual outcome, projections to 2008 and 2010 overstated growth. Errors were consistent with those made at the aggregate and therefore are likely cyclical in nature.

BLS projections of state and local government accurately expected the next decade to experience growth rates similar to those exhibited over the previous 10-year period. Therefore, both BLS and the naïve models contained very small errors. The federal government had been declining in the decades immediately preceding these projections. BLS expected that the decline would continue in each projection publication. Projections to 2006 were near the outcome, whereas the industry was relatively stable between 1998 and 2008 and experienced slow growth from 2000 to 2010. Following the September 11 terrorist attack, federal government employment increased, including the opening of a new agency, the Department of Homeland Security, which contributed slightly to more employment than expected within the projections. Since state and local employment is a much larger subsector than federal employment, government projections as a whole performed well and errors were nearly equivalent to those from the naïve model.

Employment changed very slowly over each of the projected decades, including an outright decline between 2000 and 2010. Since aggregate employment was overprojected, detailed industries also tended to be overprojected. The projections, however, do not need to be close to the actual outcomes to be helpful to our data users in advising their career decisions. Evaluating distributional shares offers a method to address the cyclical downturn. Comparing the projected share of the labor market with the actual share helps to address whether BLS correctly advised career-seeking customers which industry to pursue. As mentioned earlier, BLS expected a very slight increase, almost flat, in manufacturing jobs over each of the projections. However, the service sector was projected to grow much faster than the goods sector. Therefore, as a share of total employment, manufacturing was projected to decline by 1 to 2 percent over each of the 10-year periods. Instead, manufacturing employment fell more sharply, from 15 percent of jobs in 1996 to 9 percent in 2010, less than 15 years later (see figures 9–11). Although the decline was more dramatic than anticipated, the projections correctly expected that job prospects were much more likely in the service sector of the U.S. economy.

| Industry (all wage and salary) | Base year 1996 | Projected BLS 2006 | Actual 2006 |

|---|---|---|---|

| Mining | 0.5 | 0.3 | 0.5 |

| Construction | 4.6 | 4.3 | 5.6 |

| Manufacturing | 15.1 | 13.2 | 11.0 |

| Transportation | 3.4 | 3.5 | 3.3 |

| Communications | 1.2 | 1.0 | 1.1 |

| Utilities | 0.6 | 0.7 | 0.5 |

| Wholesale | 5.5 | 5.3 | 5.2 |

| Retail | 18.3 | 17.4 | 18.4 |

| Finance, insurance, and real estate | 5.9 | 5.6 | 6.2 |

| Other service | 28.3 | 33.3 | 31.9 |

| Government | 16.6 | 15.4 | 16.4 |

| Federal | 2.4 | 1.9 | 2.0 |

| State | 14.2 | 13.5 | 14.3 |

| Source: U.S. Bureau of Labor Statistics. | |||

| Industry (all wage and salary) | Base year 1998 | Projected 2008 | Actual 2008 |

|---|---|---|---|

| Mining | 0.5 | 0.3 | 0.5 |

| Construction | 4.8 | 4.5 | 5.2 |

| Manufacturing | 14.7 | 12.9 | 10.4 |

| Transportation | 3.4 | 3.4 | 3.3 |

| Communications | 1.2 | 1.2 | 1.0 |

| Utilities | 0.6 | 0.6 | 0.5 |

| Wholesale | 5.4 | 5.1 | 5.2 |

| Retail | 18.0 | 17.5 | 18.5 |

| Finance, insurance, and real estate | 6.0 | 5.8 | 6.1 |

| Other service | 29.3 | 33.6 | 32.6 |

| Government | 16.1 | 15.0 | 16.8 |

| Federal | 2.2 | 1.8 | 2.1 |

| State | 13.9 | 13.2 | 14.7 |

| Source: U.S. Bureau of Labor Statistics. | |||

| Industry (all wage and salary) | Base year 2000 | Projected 2010 | Actual 2010 |

|---|---|---|---|

| Mining | 0.4 | 0.3 | 0.5 |

| Construction | 5.1 | 4.9 | 4.2 |

| Manufacturing | 13.8 | 12.5 | 9.4 |

| Transportation | 3.4 | 3.6 | 3.3 |

| Communications | 1.4 | 1.3 | 1.0 |

| Utilities | 0.6 | 0.6 | 0.5 |

| Wholesale | 5.4 | 5.1 | 5.0 |

| Retail | 18.0 | 17.3 | 18.6 |

| Finance, insurance, and real estate | 5.9 | 5.4 | 6.1 |

| Other service | 30.0 | 34.3 | 33.7 |

| Government | 16.1 | 14.7 | 17.7 |

| Federal | 2.2 | 1.7 | 2.3 |

| State | 13.9 | 13.0 | 15.3 |

| Source: U.S. Bureau of Labor Statistics. | |||

Similar to the findings in the levels analysis, the findings of the share analysis showed that mining jobs were projected to decline as a share of U.S. jobs. When instead, employment in this sector grew. Still, mining is a very small sector, accounting for only 0.5 percent of U.S. jobs. Construction was underprojected as a share of U.S. employment in 2006 as the housing bubble reached its peak and then overprojected in 2010 as housing starts lingered at record lows.

The remainder of nonfarm wage and salary jobs composes the sector supporting 80 percent to 81 percent of U.S. employment in the projection base years of 1996, 1998, and 2000. Services were correctly expected to constitute a growing portion of the U.S. labor market, increasing by 1.6 percent to 2.3 percent over the projected years. In the end, they grew roughly twice as fast as expected, by 3.1 percent to 5.2 percent.

Within services, BLS correctly anticipated that other services would be the fastest growing sector by share over each of the three projected periods.18 The "other services" sector includes health care, education, legal, and many other service industries. BLS expected that as baby boomers aged and technology improvements continued, the health care sector would grow because of an aging society; health care has indeed been one of the few sectors that continued to grow even through the steep contraction years. While the levels analysis found that the other services sector grew slower than projected to 2008 and 2010, shares analysis showed that it was accurately projected by BLS to grow by 4 percent to 5 percent of U.S. employment, only about 1 percent more than the actual growth rate.

Trade, the second largest employment sector (see table 1), was projected to constitute a slightly narrowing share of employment. When instead, it stayed relatively constant. Transportation was projected to stay fairly flat in the 2006 and 2008 projections, very close to the actual outcome of a 0.1-percent decline. The drop in 2010 was captured by the projections but was expected to be slightly larger. The finance, insurance, and real estate sector was projected to decline slightly as a share of U.S employment but instead grew marginally. The bursting of the dot-com bubble and consolidation that followed resulted in bundling of phone, cable, and Internet services coincided with a decline in the share of U.S. jobs within the communications subsector. BLS projected this decline precisely within the 2006 projections but expected no change in the share over 1998–2008, and the contraction was more pronounced than expected in the 2000–10 projections. The utilities subsector was correctly expected to stay constant as a share of the U.S. labor market.

Government as a share of U.S. employment, both federal government and state and local government, grew faster than expected within the BLS projections. Government employment tends to be less sensitive to the business cycle than other sectors of the economy and therefore increased as a share of employment in recent years. BLS expected that government employment would decline by roughly 1 percent over the projected decades. Instead, government employment stayed nearly flat to 2006 and rose as a share in 2008 and 2010. The rise was mostly due to growth in state and local government, whereas share analysis showed that federal government projections were very close to the actual outcome. Given the stability of this sector through the business cycle, the levels analysis is likely more meaningful.

Given the steep effects of the latest recession, evaluating projections performance to recent years is challenging. Although BLS projections changed only slightly between 2006, 2008, and 2010, performance varied greatly because of the effects of the 2007–09 recession. This disparity reflects the importance of the assumed rate of unemployment underlying the projections. Comparing the BLS performance with the performance of other published projections and a naïve model helped mitigate the recession effect, as did evaluating industry employment projections by shares.

BLS projections performed relatively well overall and outperformed the naïve model projections for at least half the variables evaluated here. Where comparable projections were available, the mean absolute error within the BLS projections was nearly equivalent to other agency projections. Labor force projections performed well not only at the aggregate level but also for the cohort components. Faced with census population projections that were too low, BLS subtly adjusted labor force participation rates upward. The resulting projection of the labor force was accurate and captured underlying demographic trends, including the aging labor force, slowing growth in women’s participation rates, and increasing diversity.

Although employment overall and within industries tended to be overprojected, BLS was effective in providing helpful information for jobseekers as evidenced within the share analysis. Opportunities in the other services sector, which include health care and education, were accurately captured in their expectation to provide substantial job opportunities over the projected periods. The service sector, constituting more than 80 percent of the U.S. labor market, was generally well captured in the projections. The largest error in all three sets of projections was the expectation that manufacturing employment declines would dissipate and the sector would stay relatively flat over the coming decades. Through share analysis, we show the projections expected far more job growth in the service sector of the economy than the goods sector. Therefore, the projections likely did not steer jobseekers to the manufacturing sector. Other sectors with large errors included construction and mining. These sectors largely affected the steep downturn in the housing market and the technological innovation of commercial fracking. BLS improved on the naïve model results for both mining and construction sectors.

The most notable error of the 2006, 2008, and 2010 projections was the use of an unemployment rate thought to be consistent with a mature business cycle expansion rather than the use of a NAIRU-based estimate. Although most of the discrepancy between the 2010 projections and actual outcomes was due to the severity of the 2007–09 recession, the assumed 4 percent unemployment rate in the 2010 projections was overly optimistic and added unnecessary error. As such, starting with the 2002–12 projections, BLS explicitly assumed a “full employment” economy in the target year, basing the assumed unemployment rate on a NAIRU estimate.

The process of evaluating the BLS employment projections exposes the strengths and weaknesses of the BLS employment projections model. Over time, this analysis helps BLS review for biases while developing a better understanding of errors that have been made. Evaluations of the projections to 2012 and thereafter will not face issues with the NAICS revision or the major revision to the SOC code, both implemented in 2002. BLS anticipates that evaluations of these projections will again include a review of the detailed industries and occupations. Also, as the economy moves further along in the recovery from the 2007–09 recession, comparisons of the projections to trend behavior rather than cyclical influences should improve.

!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>!--?pagebreak>Kathryn J. Byun, Richard Henderson, and Mitra Toossi, "Evaluation of BLS employment, labor force and macroeconomic projections to 2006, 2008, and 2010," Monthly Labor Review, U.S. Bureau of Labor Statistics, November 2015, https://doi.org/10.21916/mlr.2015.46

1 For the purposes of this article, the terms “2006 projections” and “1996–2006 projections” will be used interchangeably.

2 The 2006 evaluations were evaluated previously. They are presented here for comparing performance over the business cycle. For detailed analysis of the 2006 projections, see Ian D. Wyatt, “Evaluating the 1996–2006 employment projections,” Monthly Labor Review, September 2010, pp. 33–69, https://www.bls.gov/opub/mlr/2010/09/art3full.pdf.

3 In 2002, all BLS programs, including employment projections, changed from the Standard Industrial Classification system to the North American Industrial Classification System.

4 The projections to 2012 were not included in this article because they were based on the new industrial classification system (North American Industrial Classification System) and were therefore inconsistent with data presented here based on the Standard Industrial Classification system.

5 The naïve model comparisons are based on a 10-year, two-point linear model from the previous decade. A static or no-growth model is assumed for the unemployment rate. H.O. Stekler and Rupin Thomas, contractors hired to evaluate the BLS projections to 2000, suggested the naïve model approach. For more information, see H.O. Stekler and Rupin Thomas, “Evaluating BLS labor force, employment, and occupation projections for 2000,” Monthly Labor Review, July 2005, pp. 46–56, https://www.bls.gov/opub/mlr/2005/07/art5full.pdf.

6 For the first formal reference to an assumed full employment economy in the BLS projections, see Michael W. Horrigan, “Employment projections to 2012: concepts and context,” Monthly Labor Review, February 2004, pp. 3–22, https://www.bls.gov/opub/mlr/2004/02/art1full.pdf.

7 For the purposes of this article, the terms “projected,” “expected,” and “anticipated” are used interchangeably.

8 We calculated errors of each of the projections with the use of published data. Some errors were estimated to arrive at comparable figures. The CBO growth rate for real GDP was calculated as an average of its annual projected growth rates, whereas the BLS growth on GDP was calculated as the compound annual growth rate. The CBO comparison estimates were based on their baseline scenario. We obtained comparison data from the CBO at http://www.cbo.gov/sites/default/files/cbofiles/attachments/Eb01-97.pdf, http://www.cbo.gov/publication/11329, and http://www.cbo.gov/publication/12958. Data from the OMB were gathered from https://obamawhitehouse.archives.gov/omb/budget/Supplemental in the History of Economic Assumptions table referencing the FY 1998, FY 2000, and FY 2002 projections because they were the nearest release dates to the comparison data from BLS. The EIA data were compiled from http://www.eia.gov/forecasts/archive/aeo97/pdf/038397.pdf, http://books.google.com/books?id=BGjSgr3cktIC&printsec=frontcover&dq=annual+energy+outlook +1999&hl=en&sa=X&ei=T-4YUeuCCIyN0QGChoBI&ved=0CC0Q6AEwAA%20-%20v=onepage&q=macroeconomic%20indic&f=false#v=onepage&q=macroeconomic%20indic&f=false, and http://books.google.com/books?id=h6dyboxP_ecC&printsec=frontcover&dq=annual+energy+outlook +2001&hl=en&sa=X&ei=3_oYUcmmHIjX0QHnlYHoCA&ved=0CDUQ6AEwAQ#v=onepage&q=annual%20energy%20outlook%202001&f=false.

9 BLS and EIA generally publish projections in December, whereas the CBO and OMB release projections in January and February of the following year. We used publicly available data to calculate errors.

10 For example, see Congressional Budget Office, The Budget and Economic Outlook: 2014 to 2024, February 2014, https://www.cbo.gov/publication/45010.

11 Jennifer Cheeseman Day, “Population projections of the United States, by age, sex, race, and Hispanic origin: 1995 to 2050,” Current Population Reports, P25-1130 (U.S. Bureau of the Census, 1995). The population projections are based on estimates derived from the 1990 census of population and reflect findings from the 1990 census of population. They are not adjusted for the undercount. For more information about the methodology and assumptions used to develop the recently released projections of the population of the United States from 1999 to 2100, see Frederick W. Hollmann, Tammany J. Mulder, and Jeffrey E. Kallan, “Methodology and assumptions for the population projections of the United States: 1999 to 2100,” Population Division Working Paper 38 (U.S. Bureau of the Census, January 13, 2000).

12 For more information, see Mitra Toossi, “Labor force projections to 2012: the graying of the U.S. workforce,” Monthly Labor Review, February 2004, pp. 37–57, https://www.bls.gov/opub/mlr/2004/02/art3full.pdf.

13 Because these data are the first assembled during the BLS projection process, they are generally finalized roughly 1 year before publication.

14 For more information, see Howard N Fullerton Jr., “Evaluating the BLS labor force projections to 2000,” Monthly Labor Review, October 2003, pp. 3–12, https://www.bls.gov/opub/mlr/2003/10/art1full.pdf.

15 For more information about the Benchmark Input-Output accounts, see https://www.bea.gov/industry/index.htm#io.

16 For instance, see Nir Jaimovich and Henry E. Siu, “The trend is the business cycle: job polarization and jobless recoveries,” NBER Working Paper no. 18334 (Cambridge, MA: National Bureau of Economic Research, August 2012), http://www.nber.org/papers/w1833 4.pdf.