An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

The actuarial value of a health insurance plan has long been used by plan administrators to appraise their company’s probable outlay on health insurance claims. But the insured view the actuarial value as a measure of the generosity afforded by a health plan. This study estimates the actuarial values of employer-sponsored health insurance plans using survey data collected from the BLS National Compensation Survey (NCS) and the Medical Expenditure Panel Survey, which is administered by the Agency for Healthcare Research and Quality. These estimates, along with existing health-insurance provisions estimates published by NCS, could provide a more comprehensive assessment of employer-sponsored health insurance benefits offered to American workers if measures of statistical significance were applied to them.

The National Compensation Survey of the Bureau of Labor Statistics (BLS) publishes annually an online bulletin that provides the detailed provisions of employer-sponsored health insurance (ESHI) plans.1 The published data include information on distributions of plan types, such as the percentage of employees enrolled in fee-for-service (FFS) plans or enrolled in health maintenance organization (HMO) plans. These publications also provide information on detailed features and characteristics of plans; this information includes the contractual cost-sharing features of health insurance. Cost-sharing features include deductible amounts, coinsurance rates, copays, and out-of-pocket expense maximums. These and other features of plans published by BLS describe, in part, the designs of ESHI plans offered to American workers. What have not yet been published, however, are actuarial values, a measure of the generosity of health plans. This article shows how reliable actuarial values could be useful to consumers—allowing consumers to compare one plan’s value with another—if such measures were to become available in the future.

The actuarial value of a health insurance plan is the average total costs of covered healthcare expenses the insurer is contractually obligated to pay.2 Actuaries have long used actuarial-value estimates to estimate payouts of plans.3 But from a policyholder’s perspective, a plan’s actuarial-value estimates the financial protection provided by the plan. This financial protection could be viewed as the generosity of the plan. The insurer typically computes the actuarial value of a specific plan by using the plan’s actual claim-payment experience. For instance, if an insurer pays 70 percent of costs that are defined as covered under the plan, the actuarial value of that plan equals 70 percent. Using this general concept of generosity, we take a more comprehensive approach by estimating the average actuarial value of a collection of ESHI plans that were gathered as part of the National Compensation Survey (NCS).

Because claims data from ESHI plans are typically not available to the survey or research community, our study estimates claim payments from a claims-payment model. This model uses healthcare utilization rates and expense levels of a simulated standardized population of healthcare users enrolled in ESHI plans. These utilization rates and expenses are derived from the household component of the Medical Expenditure Panel Survey, which is administered by the Agency for Healthcare Research and Quality. The actuarial values estimated from this claims-payment approach, along with the current NCS published benefit statistics, should provide a more robust picture of ESHI plans provided to American workers.

There are several methods that can be used to construct an actuarial-value calculator. Each method attempts to estimate the percentage of covered health costs paid by an insurer. In its most simplistic form, an actuarial value can be expressed as

For this study, we use an approach that estimates the average expense coverage of groups of ESHI plans. This is an extension of an otherwise straightforward actuarial method that computes the percentage of covered expenses of a particular health plan.

Unlike the single-plan approach, the method used here calculates the average actuarial value across groups of plans by aggregating insurance expenses paid across each plan. To estimate the paid expenses of each plan, we generate microsimulations of claim payments from health expenses of a standardized population of healthcare users covered by ESHI plans. We then gather claims and total healthcare expenses across plans to compute an average actuarial value. Groups may include workers in the same industry or occupation, or who share similar characteristics, such as being employed in small-sized establishments or being members of unions. When we estimate across these groups, plans are sorted based on whether they are indemnity plans (FFS) or prepaid plans (HMO). Although indemnity and prepaid insurance plans mainly define how providers are paid—paid by service rendered or capitation fees—the type of plan also affects the way in which the insured can receive services. For instance, HMO plans typically require gatekeepers of healthcare—by way of selected primary-care physicians—who refer patients to practitioners within HMO healthcare network systems.

Certainly, the percentage that a particular plan pays will depend on several factors: the medical-care goods and services covered, the shared-cost responsibilities, the utilization rates of medical care by enrollees, and the corresponding prices. The medical-care goods and services covered are often particular to the specific plan. For this study, we follow the coverage stipulations of the 2010 Patient Protection and Affordable Care Act (ACA), in which the act lists 10 essential health benefits:4

The utilization rates of healthcare will naturally vary across healthcare users as no two individuals or families are likely to have the same healthcare needs. For the actuarial-value calculator to be useful as a generalized measure of generosity, it must provide measurements that are meaningful across varying plan designs. In the strictest sense, this requires that the actuarial-value estimates of two health insurance plans covering the same services must be equal if they have the same cost sharing design and experience identical claims.5 Moreover, the actuarial values should have meaning over a broad spectrum of users rather than only for users who fall within select health status sets, such as those with chronic illnesses or particular healthcare needs such as prenatal and maternity care.

To generate comparable measures across plans, standardized levels of healthcare utilization and expenses are used to derive claim-payment estimates. To standardize usage and spending across plans, the principal practice among actuaries is to construct an artificial population of diverse healthcare users that is tailored to resemble the population of users of the plans being evaluated. For instance, ESHI plans cover largely the population at or under the age of 65, and so the artificial population should consist mainly, if not exclusively, of individuals at or under 65. Standardizing the population is a key principal because our interest is in how a plan compares with other plans that have different designs but the same usage and spending; our interest is not in how generous a plan might be to a particular healthcare user.

To be fair, using a standardized population does not purge all nondesign variance among plans. Because healthcare usage can, in part, be induced by how well plans cover categories of healthcare, the ease of access to care, and the availability of network providers and treatment options, reliance on a standardized level of usage and spending will likely fail to account for induced spending behavior differences among plans. For instance, some healthcare users may specifically choose plans for their relatively generous claims coverage for specific healthcare, such as the coverage level for prenatal and maternity care. An actuarial-value approach alone cannot account for such preselection insurance choices. Moreover, contractual prices paid to healthcare providers might vary among insurance carriers. That is to say, there is no prevailing rate for a particular service throughout the national healthcare system. These price differences are not captured explicitly in expenditure surveys, and thus quantity levels are lost within expenditure numbers. To adjust for such differences, an average payment rate for the many possible goods and services would have to be applied rather than using straight expenditure data.6 This would require adjusting expenses by price variation for the many different healthcare providers, a task that is simply not possible for this type of study.7 Moreover, two plans may cover the same care—such as maternity—but the extent to which each plan covers that care may differ. For example, one plan may provide hospitalization for up to 48 hours following childbirth while another may provide the same for up to 72 hours.

To see how spending level and plan design affect actuarial values, the following tables provide simplified examples of actuarial values under three different healthcare plan designs; these designs describe the deductible levels, coinsurance rates, and out-of-pocket maximums.8 For illustration purposes only, the plans are evaluated under 3 levels of family spending. For table 1, the actuarial value is lowest for the plan with the highest deductible (the insurer pays 54 percent of covered expenses), even though that plan requires from the healthcare user the lowest coinsurance rate. The low spending coupled with the high deductible limits the claims that are covered under this scenario. The generosity measures of these plans shift, however, as family healthcare spending increases. In table 2, using the same plan designs but doubling the covered healthcare expenses, we find the actuarial values of all 3 plans converge at 72 percent of total covered costs even though each has a very different cost-sharing design. Under this scenario and assuming all else is constant—such as network and provider access—healthcare users would be indifferent in their choices among these three plans. Pushing the expenses even higher, table 3 shows that the ordering of generosity among the three plans flips as the demand for healthcare increases. Plan 3, which was the least preferred when spending was lowest, becomes the most generous plan when costs escalate.9

| Plan | Family-level spending (in dollars) | Cost-sharing parameter of plan | Shared cost | Actuarial value | |||

|---|---|---|---|---|---|---|---|

| Deductible | Co-insurance rate | Out-of-pocket maximum | Participant share | Insurer share | |||

| 1 | 2,500 | 0 | 0.28 | 2500 | 700 | 1800 | 0.72 |

| 2 | 2,500 | 500 | .2 | 2500 | 900 | 1600 | .64 |

| 3 | 2,500 | 1000 | .1 | 2500 | 1150 | 1350 | .54 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | |||||||

| Plan | Family-level spending (in dollars) | Cost-sharing parameter of plan design | Shared cost | Actuarial value | |||

|---|---|---|---|---|---|---|---|

| Deductible | Co-insurance rate | Out-of-pocket maximum | Participant share | Insurer share | |||

| 1 | 5,000 | 0 | 0.28 | 2,500 | 1,400 | 3,600 | 0.72 |

| 2 | 5,000 | 500 | .2 | 2,500 | 1,400 | 3,600 | .72 |

| 3 | 5,000 | 1000 | .1 | 2,500 | 1,400 | 3,600 | .72 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | |||||||

| Plan | Family-level spending (in dollars) | Cost-sharing parameter of plan design | Shared cost | Actuarial value | |||

|---|---|---|---|---|---|---|---|

| Deductible | Co-insurance rate | Out-of-pocket maximum | Participant share | Insurer share | |||

| 1 | 10,000 | 0 | 0.28 | 2,500 | 2,500 | 7,500 | 0.75 |

| 2 | 10,000 | 500 | .2 | 2,500 | 2,400 | 7,600 | .76 |

| 3 | 10,000 | 1,000 | .1 | 2,500 | 1,900 | 8,100 | .81 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | |||||||

These demonstrations illustrate that actuarial values will differ across designs and expenditure levels. Because we are interested in making comparisons across plan designs, we standardized spending to eliminate the major generosity variability demonstrated in these three examples. The utilization and expenses of a standardized population afford a fixed level of average spending. This allows the evaluation of generosity among the three plans designs to be purged, in large part, of spending variance (see tables 1, 2, and 3).

What can be said about the size of actuarial values? To give some perspective to the size of actuarial values, we note that the Internal Revenue Service reported that approximately 98 percent of individuals covered under an ESHI plan are enrolled in plans that pay at least 60 percent of covered healthcare expenses.10 Moreover, according to a report by the Consumers Union,11 the typical preferred provider organization (PPO) plan sponsored by employers pays 83 percent of covered healthcare costs.

With a sketch of the actuarial-value calculator and the expected sizes of actuarial values, we now turn to the two sources of data for the study before we describe the claim payment program that will estimate the actuarial values of ESHI plans.

Both the numerator and denominator of the actuarial-value expression shown earlier must be estimated. To estimate an actuarial value requires healthcare usage and expense data that are paired with the contractual cost-sharing parameters set within the claims-payment model. The usage and expense data come from the household component of the Medical Expenditure Panel Survey-Household Component, or the MEPS-HC. Values for the contractual cost-sharing parameters of the model come from information drawn from summary plan description brochures that are collected in the National Compensation Survey (NCS). Each of these data sources is briefly described below.

National Compensation Survey. The NCS, conducted by the Bureau of Labor Statistics, is an establishment-based survey that provides comprehensive measures of levels and trends in employer costs of employee compensation; it also gives us information about the incidence and provisions of employer-provided benefits. The survey supplies the data for the quarterly Employer Cost Index and the Employer Cost for Employee Compensation reports. The NCS also tabulates—on an annual schedule—the incidence and provisions of health, retirement and other employer-provided benefits. The provisions statistics include detailed estimates about the types of plans, such as the percentage of workers enrolled in different types of FFS plans and HMO plans. The provisions statistics also provide features of health plans, such as the percentage of workers who pay part of premium costs, as well as supplying us with information on cost-sharing requirements of plans including the deductible amounts, copays, coinsurance rates, and out-of-pocket maximums.12 These detailed provisions statistics are tabulated principally from information coded from Summary Plan Descriptions (SPD) brochures. An SPD provides a summary of the detailed provisions of plans that describe the expected and legal obligations of sharing costs between plan participants and health insurers. A full set of coded data from the SPDs provides the cost-sharing arrangements that are necessary to control payment schemes within the claims-payment model.

The NCS is designed to sample civilian workers employed in private industry establishments as well as workers in state and local governments. The survey excludes military personnel; workers in federal agencies, agriculture, private households, and unpaid jobs; and the self-employed and others who set their own pay. The survey data are collected from probability samples that canvass all 50 states and the District of Columbia. Establishments selected are commonly single economic units engaged in one, or predominately one, economic activity. For private industries, an establishment is a single physical location, such as a mine, a factory, an office, or a store. Establishments are classified by their assigned North American Industry Classification System (NAICS) code.13 The number of occupations selected depends on the employment size of establishments. Large establishments can have as many as eight occupations selected while small establishments can have as few as one to four occupations selected. Occupations consist of individual workers or groups of workers who share the same job duties and job characteristics such as part- or full-time work schedules and payment methods—for example, commission pay as opposed to hourly pay or salary. Each sampled occupation is classified on the basis of the Standard Occupational Classification system, or SOC. An occupation is the unit of observation in the NCS.14

The NCS uses a sampling panel structure to rotate establishments in and out of the survey. A panel is a subset of all establishments sampled for the survey that begin their participation at the same time. Approximately one-third of the private industry sample is reselected each year. Establishments in each panel remain in the survey for 3 years. Because of the complexity of the survey, it takes 12 months to initiate a new survey panel. During that initiation period, establishments are asked to provide SPDs of all health plans that are offered to the occupations that are sampled. To reduce response burden, only during this initiation period are establishments asked to provide the SPDs of each plan offered. This study uses a single-sample panel that was initiated in 2011.15 The panel consists only of workers in private industry establishments. The following tabulations provide a summary of the number of plans analyzed from SPDs collected from this sample panel.

| Total number of unique plans analyzed from the panel | 4,300 |

| Medical plans with drug coverage | 2,578 |

| Medical plans with drug coverage, less incomplete records | 2,003 |

| Occupational records mapped to unique plans | 11,911 |

There were 4,300 unique health plans analyzed from the panel. These include any number of combinations of health insurance plans. Most, however, are medical plans that provide coverage for hospitalization, outpatient care, ambulatory services, and outpatient drug coverage. Of the 4,300 plans, 2,578 are medical plans with drug coverage. Many of the remaining plans are either medical-care plans that do not provide drug coverage, plans that provide supplemental coverage such as stand-alone drug plans, dental-care plans, or vision-care plans. This study evaluates only medical plans with drug coverage because its purpose is to assess the ability of the NCS survey to estimate generosity of ESHI plans that cover, in large part, the main components of medical-care goods and services; these components include outpatient drugs, as prescribed by the ACA requirements. Supplemental coverage for dental and vision care are excluded from this study because dental and vision care are not evaluated in the claims-payment model. Of the 2,578 medical plans with drug coverage, 2,003 had sufficient information coded to use in setting the cost-sharing parameters within the claims-payment model.16 These 2,003 unique plans are joined with the appropriate 11,911 occupational records, which were the records used in analysis. Notice that there are more occupational records than unique plans—about 6 occupational records to each plan—because the same medical and drug plans are often offered to any number of workers within an establishment.

Because the cost-sharing parameters coded from the SPDs can vary by provider networks or drug-tier choice, the claims-payment routines of the model assume that participants choose the most generous options offered from the plans. For instance, if a plan offers a network of providers at lower deductible and copay rates, it is assumed that participants will access all health goods and services through that network. This extends to drug usage as well. If a plan offers multiple-tier copay or coinsurance rates such as generic, brand name, and formulary, it is assumed that the participant will select the lower price generic brands whenever available. Consequently, this modeling approach produces actuarial values that must be interpreted as upper-bound estimates.

The upper-bound approach would seem reasonable in most instances, but concerns do arise. For example, generic drugs are formulated to provide the same treatment responses as their related brand-name drug products. However, generic drugs are not universally available for all possible drug treatments; sometimes only the more expensive brand-name drug products are available. The claim-payment routines of the model look at only the incidence and numbers of prescriptions from the MEPS-HC data and not whether choices were made, when possible, between generic drugs and the more expensive brand-name drugs. A similar argument can be made for medical care treatments, such as when patients have no options aside from obtaining products or treatments outside of a health insurance network. Such instances would require the insured to pay the higher cost-sharing amounts, whether they be in deductibles, copays, or coinsurance rates. Without a data linkage between service and choice, therefore, the model approach cannot properly account for network or drug choice.17

Medical Expenditure Panel Survey, household component.18 The current MEPS, administered by the Agency for Healthcare Research and Quality, consists of two major components: a household survey of families and individuals (the household component, or MEPS-HC) and an establishment survey of private and public sector employers (the insurance component, or MEPS-IC).19 MEPS-HC gathers demographic information and a host of health-related information, from individuals, about such items as health status, insurance coverage, and medical care usage and expenses. Because of the difficulty of collecting from household respondents accurate and detailed information on the types of healthcare received and the corresponding costs, the MEPS-HC is supplemented, when possible, by the medical provider component (MPC) of MEPS. The MPC surveys hospitals, physicians, home healthcare providers, and pharmacies identified in the household survey component and, with the permission of the household respondents, collects the detailed usage and expenditure information from the providers. The MEPS-HC survey data with its demographic information, insurance coverage indicators, and usage and expense amounts provide the necessary set of data to construct a standardized population of healthcare users enrolled in ESHI plans.

The MEPS-HC is a representative sample of the U.S. noninstitutionalized civilian population. The sample is designed as an overlapping panel survey; a new panel of households is selected each year and interviewed over 2 full calendar years. The households selected for each panel are a subsample of households that participated in the previous year’s National Health Interview Survey conducted by the National Center for Health Statistics.20 To construct a representative standardized population, the claims-payment model draws in survey data from MEPS-HC 2009 and 2010 survey years. These data are available from the annual releases of the Full Year Consolidated Data Files.21 Multiple survey years were used to provide a more consistent estimate of usage and expenditures for the model. Because 2009 and 2010 expenditure data are paired with insurance data from 2011, all dollar values are adjusted to 2011 dollars using the medical-component index of the Consumer Price Index. These full-year files provide annualized usage and expense data over a calendar year, and it is those annualized data values that are used in the analysis.

The usage and expenditure values cover the following medical care categories as they are itemized in the MEPS-HC data files:

• Office-based visits to physicians and nonphysicians, each measured separately

• Outpatient visits to physicians and nonphysicians, each measured separately

• Emergency room visits

• Inpatient hospital stays

• Home healthcare

• Prescription medicines

These usage and expenditure categories align well with the NCS ESHI plan data with which they must be paired for us to estimate the actuarial values. These expense categories also align quite well with the broadly defined 10 essential health benefits prescribed by the ACA.

In an effort to construct the standardized population to closely resemble the healthcare usage and spending patterns of ESHI plan enrollees, MEPS-HC individual records are selected based on several criteria. To reduce the influence that Medicare coverage may have on healthcare usage, only individuals age 65 or younger are included.22 Additionally, only individuals who are covered under an ESHI plan are included. This includes individuals covered under their own ESHI plans or covered as dependents of ESHI plans. Since annual utilization and expenditure data are used, only individuals with health insurance coverage for at least 6 months of the year are included. It is our hope that this 6-month selection criterion provides a smooth and representative pattern of healthcare usage over a year even though job switching or unemployment may cause short episodes of interruptions in coverage.

Because many health plans have family deductible and out-of-pocket limits, expenditures in the claims-payment model are analyzed at both the individual and family level. MEPS organizes the individuals represented in the survey into Health Insurance Eligibility Units (HIEU), thereby allowing for individual and family-level estimates. HIEU consists of families living together (including any students living away at school) that are related by blood, marriage or adoption. The HIEUs can be described as subfamilies, a category defined by the Current Population Survey. An HIEU is a subfamily of a CPS-defined family in that the former includes only those individuals of a CPS family who qualify under another family member’s insurance plan.23

The following Medical Expenditure Panel Survey tabulations provide individual and HIEU records counts for the 2009 and 2010 full-year consolidated annual data files.

| Total number of individual records, 2009 | 36,855 |

| Individual records in scope of study | 14,051 |

| Health Insurance Eligibility Units in scope of study | 7,111 |

| Total number of individual records, 2010 | 32,846 |

| Individual records in scope of study | 12,271 |

| Health Insurance Eligibility Units in scope of study | 6,285 |

| Total individual records in scope of study, 2009 and 2010 pooled | 26,322 |

| Total Health Insurance Eligibility Units in scope of study | 13,396 |

With the source of data in hand, we can now turn to the actuarial-value estimates generated from the claims-payment model that uses these data jointly.

The research-based claims-payment model provides the mechanism with which to estimate the actuarial values of plans. Essentially, the model estimates the percentage of MEPS HIEU expenditures that would be paid by health insurance had those HIEUs been enrolled in the ESHI plans similar to those gathered from the NCS. Certainly, the model cannot predict the exact payment that would be made for any given claim, but the model is designed in conjunction with the data to estimate the typical levels of claim payments.

To show the types of estimates that can be produced by this modeling approach, we present our actuarial-value estimates sorted into two main health insurance categories: FFS and HMO plans. The former typically provides more flexible healthcare access options, such as choosing one’s own hospital or doctor, while the latter provides higher coverage rates—and therefore lower out-of-pocket costs—but more restrictive access rules, such as paying claims only if healthcare was received through an HMO-network provider. According to health insurance incidence statistics available from the BLS Employee Benefit Survey (EBS) annual bulletin, 82 percent of private industry workers who participate in ESHI enrolled in FFS plans; the remaining workers enrolled in HMO plans.24 This suggests that workers covered under ESHI prefer some level of choice when it comes to healthcare providers. Most but not all FFS plans offer a choice of healthcare providers.

There are several types of FFS plans that are designed with varying levels of healthcare-provider choice. The most flexible among them are the traditional plans that pay providers similar rates without regard to whether those providers are within contractually arranged healthcare network systems. Among traditional FFS plans, the insured can choose any qualified healthcare provider and expect the same level of claims paid for covered services. On the other end of the flexibility spectrum, exclusive provider organizations (EPOs) offer the least flexibility among FFS plans, as they require the insured to receive healthcare exclusively through select providers if claims are to be paid. Between these two extremes are two other types of FFS plans, point-of-service plans—a rarity among FFS plans—and Preferred Provider Organizations (PPO) plans.25

Of the 82 percent of private industry workers enrolled in FFS plans, nearly 88 percent (72 percent of all ESHI enrollees) are enrolled in PPO plans. With such a large percentage of workers enrolled in PPO plans, the actuarial-value estimates presented for FFS plans are principally driven by the payment features of these plans. PPOs provide the flexible-healthcare-access features found among traditional FFS plans; however, PPOs are defined as managed-care plans similar to HMOs because the shared-payment features are devised to encourage the PPO insured to access healthcare through preferred-provider networks. Healthcare received through preferred-provider networks has deductibles, copays, and coinsurance rates that all are lower than if healthcare were received from providers outside of these networks. The blended features of PPOs—providing choice but offering higher coverage rates within networks—may explain, in part, why they are the most popular plans among all ESHI plans.

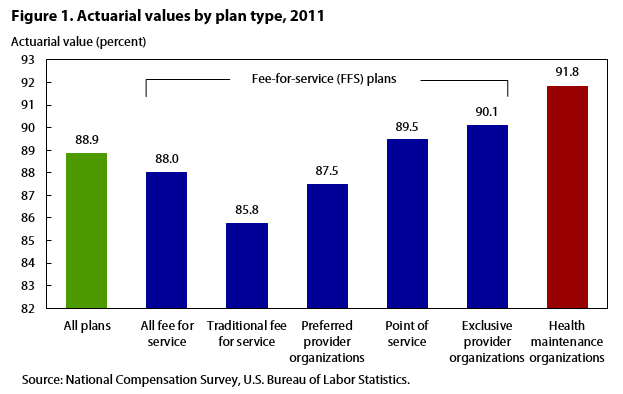

| Type of plan | Number | Actuarial value |

|---|---|---|

| All plans | 11,911 | 88.9 |

| All fee for service | 9,086 | 88.0 |

| Traditional fee for service | 368 | 85.8 |

| Preferred provider organizations | 6,338 | 87.5 |

| Point of service | 1,635 | 89.5 |

| Exclusive provider organizations | 745 | 90.1 |

| Health maintenance organizations | 2,825 | 91.8 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | ||

Figures 1 through 6 provide varying views of the actuarial-value estimates generated from the claims-payment model. Figure 1 shows the average actuarial values by type of plan, while the remaining figures show actuarial-value estimates by plan type arrayed across several establishment and occupational characteristics. Because these estimates are generated from two survey sources, we have not yet developed a method in which to compute standard errors of the estimates. Consequently, any comparisons should be done with caution. Figure 1 shows the monotonically increasing relationship between provider choice and generosity among the different FFS plans. The results exhibited in figure 1 suggest that there is a tradeoff between flexibility to choose providers and generosity in terms of expense coverage. Comparing the most flexible plans in terms of choice of healthcare providers, we find that traditional FFS plans pay 85.8 percent of covered expenses, on average, which is 6 percentage points less than the typical HMO plan. However, exclusive provider organizations (EPOs) pay, on average, 90.1 percent, an actuarial value that falls very close to the average HMO. EPOs are designed as indemnity plans, but they are as restrictive in choice as HMOs, if not more so.

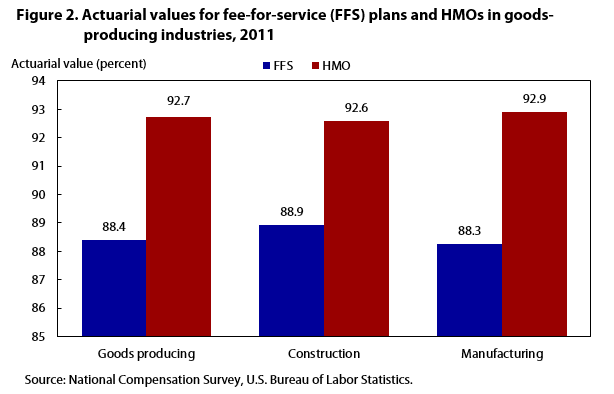

| Industry | FFS | HMO |

|---|---|---|

| Goods producing | 88.4 | 92.7 |

| Construction | 88.9 | 92.6 |

| Manufacturing | 88.3 | 92.9 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | ||

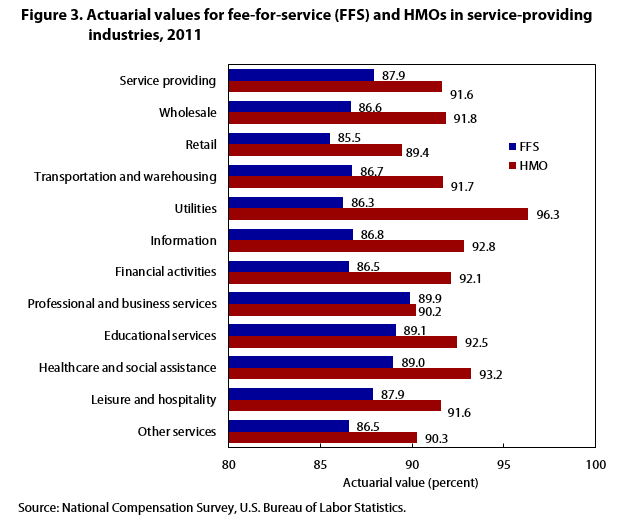

| Industry | FFS | HMO |

|---|---|---|

| Service providing | 87.9 | 91.6 |

| Wholesale | 86.6 | 91.8 |

| Retail | 85.5 | 89.4 |

| Transportation and warehousing | 86.7 | 91.7 |

| Utilities | 86.3 | 96.3 |

| Information | 86.8 | 92.8 |

| Financial activities | 86.5 | 92.1 |

| Professional and business services | 89.9 | 90.2 |

| Educational services | 89.1 | 92.5 |

| Healthcare and social assistance | 89.0 | 93.2 |

| Leisure and hospitality | 87.9 | 91.6 |

| Other services | 86.5 | 90.3 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | ||

By industry, the actuarial-value estimates suggest that workers in the goods-producing industries are offered FFS and HMO plans that are not all that dissimilar, in terms of generosity, to plans offered to workers in service-providing industries (see figures 2 and 3). For the FFS plans, workers in goods-producing industries are offered plans with actuarial values of 88.4 percent, while workers in service-providing industries are offered plans with actuarial values of 87.9 percent. A similar small difference is found among HMOs where goods-producing industry workers are offered plans that pay 92.7 percent whereas workers in service-providing industries have HMOs that pay 91.6 percent. These differences may be economically insignificant in terms of out-of-pocket costs for many workers with typical healthcare expenses. Nonetheless, there are larger numerical differences among some of the individual industry groups that suggest there might be more divergences among plan generosity than observed from the goods-producing and service-providing estimates.

Most notable is the actuarial-value estimate for HMO plans offered to workers in the utility industry. These workers have HMO plans that pay 96.3 percent of covered expenses, which is 4.5 percentage points more than the typical HMO plan and 10.5 percentage points more than the traditional FFS plan. Although identifying the exact factors explaining the levels of actuarial values is beyond this study, these more generous plans might in part be explained by the high rate of unionization among workers in the utility industry. According to a report by the Bureau of Labor Statistics, the utility industry has the highest percentage of workers represented by unions.26 In that unions can collectively bargain for better healthcare plans than nonunion workers, we might expect that plans in highly unionized industries would pay more generously.

On the lower end of generosity are the plans that are offered to workers in retail. FFS plans offered to these workers pay, on average, 85.5 percent of covered healthcare costs, 2.5 percentage points less than the typical FFS plan. Similarly, HMO plans offered to these same workers pay 89.4 percent of covered expenses, or 2.4 percentage points less than the typical HMO plan.

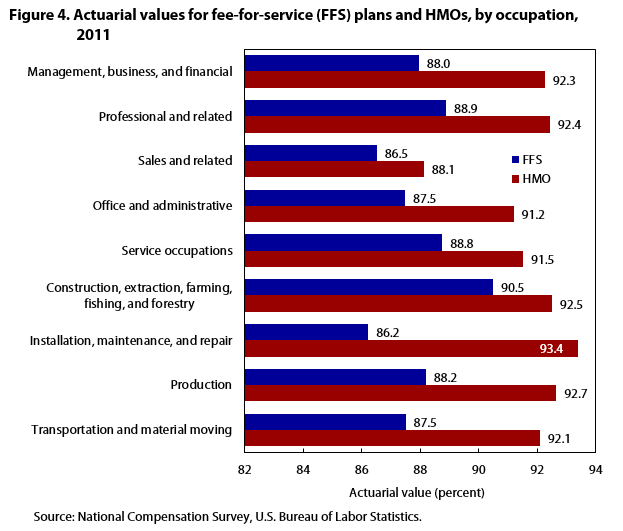

| Occupation | FFS | HMO |

|---|---|---|

| White-collar occupations | ||

| Management, business, and financial | 88.0 | 92.3 |

| Professional and related | 88.9 | 92.4 |

| Sales and related | 86.5 | 88.1 |

| Office and administrative | 87.5 | 91.2 |

| Service occupations | 88.8 | 91.5 |

| Blue-collar occupations | ||

| Construction, extraction, farming, fishing, and forestry | 90.5 | 92.5 |

| Installation, maintenance, and repair | 86.2 | 93.4 |

| Production | 88.2 | 92.7 |

| Transportation and material moving | 87.5 | 92.1 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | ||

Figure 4 provides actuarial-values across occupational groups.27 Perhaps not surprising, sales and related occupations are offered the least generous plans regardless of whether those plans are FFS or HMO plans. This is a predictable result because most sales workers are employed mainly in retail establishments, which was the industry group mentioned above for having the least favorable plans. FFS plans offered to sales workers pay on average 86.5 percent, while HMO plans offered to sales workers pay on average 88.1 percent. It is noteworthy that the HMO plans offered to sales workers are no more generous than the typical FFS plan offered to all private industry workers.

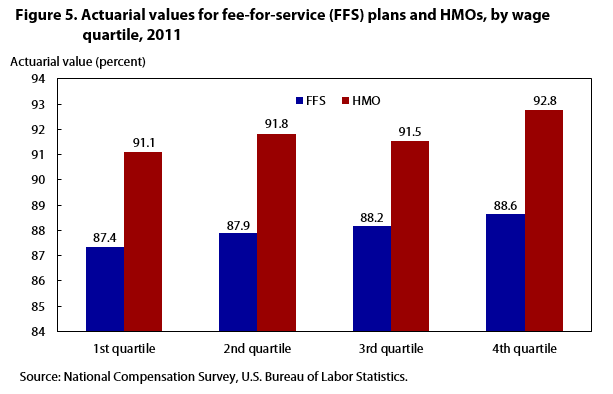

| Quartile | FFS | HMO |

|---|---|---|

| 1st quartile | 87.4 | 91.1 |

| 2nd quartile | 87.9 | 91.8 |

| 3rd quartile | 88.2 | 91.5 |

| 4th quartile | 88.6 | 92.8 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | ||

Figure 5 presents estimates of actuarial values of plans sorted by wage quartiles. The purpose of these estimates is to determine whether there are marked differences in plan generosity between, say, the lowest and highest paid workers in the economy. The quartile results show that the workers falling in the first quartile—the lowest wage earners—have access to both FFS and HMO plans that are not all together numerically different from workers in the top quartile of wage earners. These differences certainly are much smaller than what were found among the industry and occupational groups presented in figures 2, 3, and 4. This would suggest that employment within a particular industry or occupation is a more important determined in the generosity of health insurance than the wage level of a worker.

| Industry | FFS | HMO |

|---|---|---|

| Goods producing | 88.4 | 92.7 |

| Construction | 88.9 | 92.6 |

| Manufacturing | 88.3 | 92.9 |

| Service providing | 87.9 | 91.6 |

| Wholesale | 86.6 | 91.8 |

| Retail | 85.5 | 89.4 |

| Transportation and warehousing | 86.7 | 91.7 |

| Utilities | 86.3 | 96.3 |

| Information | 86.8 | 92.8 |

| Financial activities | 86.5 | 92.1 |

| Professional and business services | 89.9 | 90.2 |

| Educational services | 89.1 | 92.5 |

| Healthcare and social assistance | 89.0 | 93.2 |

| Leisure and hospitality | 87.9 | 91.6 |

| Other services | 86.5 | 90.3 |

| Source: National Compensation Survey, U.S. Bureau of Labor Statistics. | ||

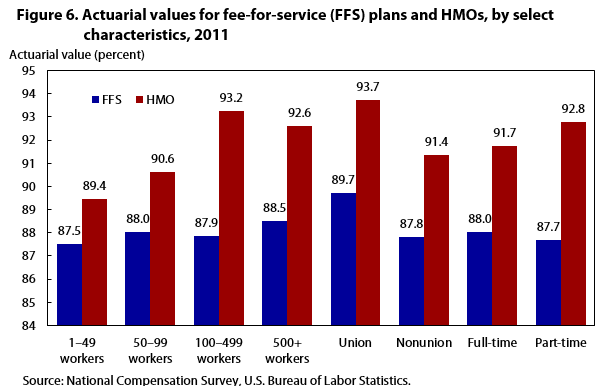

Figure 6 presents actuarial values of plans by establishment size, union and nonunion affiliation, and full-time and part-time work status. Of these characteristics, actuarial values for union workers and workers employed in establishments employing at least 500 workers stand out. Whether one is a union worker or worker in a large establishment, the FFS and HMO plans that are provided appear to be more generous than the average plan. This is not surprising for union workers, as collective bargaining may afford them access to generous plans. Similarly, large-size establishments may be able to offer their employees—through their larger risk pool of enrollees—more actuarially generous plans. In comparison, workers in the smallest establishments, those employing less than 100 workers, are offered the least generous plans, as is true for nonunion workers.28

The paper describes ongoing BLS research work that has developed a method in which to estimate the average actuarial values of employer-sponsored health insurance plans. These actuarial values are measures of health-plan generosity in terms of providing financial protection against unexpected healthcare episodes. The underlying approach is to estimate claims payments using a model that incorporates utilization and expense data of healthcare made available from the Medical Expenditure Panel Survey, coupled with the cost-sharing parameters gathered from Summary Plan Descriptions of employer-sponsored health insurance collected by the National Compensation Survey. These actuarial-value estimates, in conjunction with other National Compensation Survey statistics, should provide a more comprehensive picture of health plans offered to American workers.

More research work is needed. One area of research could be to look at other sources of health claims data that may allow for richer estimates. In addition, research potentially could generate actuarial-value estimates of plans collected over a broader period of time than what is provided in this study so that the claim-payment model could provide a means by which estimates of actuarial value is computed for a series of periods. Improved in these ways, and with calculation of standard errors, this model would likely be of interest as the multifaceted effects of the Affordable Care Act change the healthcare coverage landscape.

!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->!--?pagebreak?-->Thomas G. Moehrle, "Measuring the generosity of employer-sponsored health plans: an actuarial-value approach," Monthly Labor Review, U.S. Bureau of Labor Statistics, June 2015, https://doi.org/10.21916/mlr.2015.16

1 For the latest online bulletin describing employer-sponsored health insurance, see EBS Annual Bulletin on “Benefit plan details in private industry,” http:/www.bls.gov/ncs/ebs.

2 The term insurer is used universally throughout the paper even though the payer or underwriter of health expenditure claims for employees might be a self-insured employer or employee union rather than an insurance company.

3 See Lynn Quincy and Deanna Okrent, “Creating a usable measure of actuarial value,” Consumers Union Policy and Action from Consumer Reports, synopsis of October 17, 2011 meeting, http://www.consumersunion.org/wp-content/uploads/2013/04/CU_Actuarial_Value_2012_Report.pdf.

4 For more information about the 10 essential health benefit categories stipulated by the ACA, see https://www.healthcare.gov/blog/10-health-care-benefits-covered-in-the-health-insurance-marketplace/.

5 Although the actuarial values may be equal, other parts of each plan may differ. For instance, one plan might have a more limited network of healthcare providers and therefore be less preferred than another plan that has an identical cost-sharing design but easy access to a wide variety of network providers.

6 To use an analogy, a $100 market basket of goods bought in a discount grocery store might have the same types of groceries—meats, vegetables and such—as a $100 basket bought in a gourmet grocery store, but the two baskets would likely have differences in quantity and quality of items within those baskets. Insurance companies that compute actuarial values for their own plans avoid these difficulties as they typically use their own claims data, which reflect usage-induced spending behavior and contractual network payment rates that they negotiate with their providers.

7 Price variation becomes particularly important in terms of generosity of plans in high-healthcare-price areas. For instance, plans that principally require copays will afford more financial protection with the same levels of healthcare utilization in high-price areas than would plans requiring coinsurance-shared arrangements.

8 Copays, which are present in many plans, are suppressed to keep the examples simple by not directly illustrating utilization.

9 Notice that plan 1 would have been less generous with the higher spending behavior had the out-of-pocket limit not been met.

11 L. Quincy and D Okrent, “Creating a usable measure of actuarial value.”

12 For the most recent detailed health plan bulletin that provides these estimates, see “National Compensation Survey: health and retirement plan provisions in private industry in the United States, 2013,” Bulletin 2778 (U.S. Bureau of Labor Statistics, August 2014), https://www.bls.gov/ncs/ebs/detailedprovisions/2013/ownership/private/ebbl0054.pdf.

13 NAICS is the North American Industry Classification System, which is designed to assign a unique six-digit numeric code to each industry according to its economic activity.

14 For more information about the NCS design, see “Chapter 8, National compensation measures,” BLS Handbook of Methods, which can be found at https://www.bls.gov/opub/hom/pdf/homch8.pdf.

15 The National Compensation Survey refers to this sample panel initiated in 2011 as Panel 109.

16 The 575 plans that were dropped from this study lacked the complete information necessary to set all the cost-sharing parameters of the claims-payment model.

17 If the effects caused by choice are nontrivial, the actuarial-value differences found between traditional FFS plans, which provide higher cost-sharing responsibilities but minimal service-access rules, and HMO plans, which provide low cost-sharing responsibilities but strict access rules, are not as large as reported in estimates presented in this paper.

18 The immediate text is drawn from survey descriptions of the MEPS. A more complete description of the surveys can be found at http://meps.ahrq.gov/mepsweb.

19 Data from the MEPS-IC are not used in this study.

21 See http://meps.ahrq.gov/mepsweb/data_stats/download_data_files_results.jsp?cboDataYear=All&cboDataTypeY=1%2CHousehold+Full+Year+File&buttonYearandDataType=Search&cboPufNumber=All&SearchTitle=Consolidated+Data.

22 At age 65, individuals are eligible to enroll in Medicare. If they are enrolled, Medicare becomes their primary insurance provided that they are no longer covered by an employer-sponsored health insurance plan. Thus, age 65 has been used as the border age between employer-sponsored plans as primary coverage and Medicare.

23 See MEPS HC-129 full year consolidated data file documentation on pages C5–C6 for more descriptive details of Health Insurance Eligibility Units construction. The documentation can be found at http://meps.ahrq.gov/mepsweb/data_stats/download_data/pufs/h129/h129doc.pdf.

24 For employer-sponsored health insurance incidence and provision estimates for 2013—the latest Employee Benefit Survey estimates available—see https://www.bls.gov/ncs/ebs/detailedprovisions/2013/ownership/private/basic_health.htm.

25 See https://www.bls.gov/ncs/ebs/glossary20132014.htm for a glossary of employee benefit terms, including definitions for health-plan types that describe differences among FFS and HMO plans.

26 Current Population Survey, Bureau of Labor Statistics “Union Members—2013,” news release, USDL-14-0095 (U.S. Bureau of Labor Statistics, January 23, 2015), https://www.bls.gov/news.release/pdf/union2.pdf.

27 The occupational groups of this study are the same occupational groups that are found in the National Compensation Survey publications, such as the Employment Cost Index. These relatively high-level aggregates enable estimation by job tasks as defined by the Standard Occupational Classification Manual.

28 Some caution must be exercised for estimates by establishment size. Establishments are single-site units; therefore, estimates by establishment size might be somewhat muted in comparison with analysis at the enterprise or firm level. NCS survey design precludes estimates at higher organizational levels such as the firm level.