An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

Crossref 0

Caught Between Volunteerism and Professionalism: Support by Nonprofit Leaders for the Donative Labor Hypothesis, Review of Public Personnel Administration, 2020.

Nonprofit Wage Theory and Evidence, International Encyclopedia of Civil Society, 2022.

Human Service Organizations’ Participation in the Paycheck Protection Program: A Cross-Sector Comparison, Human Service Organizations: Management, Leadership & Governance, 2024.

The Evolution of Talent Management: From Broad Strategies to Integrated Succession Planning, Administrative Sciences, 2026.

Is Compassion a Good Career Move?: Nonprofit Wage Differentials from Employer Changes, SSRN Electronic Journal , 2019.

How did we get here? The career paths of higher education fundraisers, Nonprofit Management and Leadership, 2020.

Multiple Stakeholders and Multiple Bottom Lines, Ethics for Social Impact, 2018.

Nonprofit earnings and sectoral employment in the United States since 1994, Monthly Labor Review, 2024.

Donative labor effect of the nonprofit pay: A multilevel explanation, Nonprofit Management and Leadership, 2020.

Doing Good Work in a Crisis: Views of Pay and the COVID-19 Pandemic in the Public, Nonprofit, and For-Profit Sectors, Review of Public Personnel Administration, 2024.

Public Sector Collective Bargaining: A Meta-Review, Review of Public Personnel Administration, 2025.

Are Nonprofits More Equitable than For-Profits? An Estimate of the Gender Pay Gap in the U.S. Human Services Field, Human Service Organizations: Management, Leadership & Governance, 2020.

A BLS study reveals that, in the aggregate, workers at nonprofit businesses earn a pay premium compared with their for-profit counterparts. Detailed analyses, however, show a more nuanced picture: using wages as the pay measure indicates a slight wage disadvantage for management, professional, and related workers, and a wage advantage for service workers, at nonprofits and wage parity between nonprofit and for-profit sales and office workers; using total compensation as the pay measure indicates compensation parity between nonprofit and for-profit businesses for management, professional, and related workers and for sales and office workers and a compensation premium for nonprofit service workers.

Economic theory provides mixed evidence on whether nonprofit workers are at a compensation advantage or disadvantage relative to their for-profit counterparts. On the one hand, because profits cannot be retained by a nonprofit firm, managers of such firms have few incentives to maximize profits. Hence, managers of nonprofits may have an increased incentive to transfer returns to workers in the form of higher compensation.1 On the other hand, employees who work for nonprofits might be willing to accept lower levels of pay because of the altruistic tendencies and nonpecuniary rewards associated with working for a nonprofit.2

Empirical evidence on whether the gap between nonprofit and for-profit wages is positive or negative is likewise mixed. Laura Leete found no overall wage gap and small wage penalties for nonprofit managers compared with their for-profit counterparts.3 In a study of hospital workers, Edward Schumacher found a wage advantage for workers at nonprofits, which disappears after controlling for worker characteristics.4 Like Schumacher, Christopher Ruhm and Carey Borkoski concluded that workers with similar characteristics receive similar pay whether employed at a nonprofit or for-profit firm, but they also found results consistent with some relatively small premiums and penalties for subgroups of nonprofit workers.5

Most studies that test the pay gap between nonprofit and for-profit firms use household microdata from the Current Population Survey or the decennial census, as well as self-reported information, to determine whether an individual’s employer is a nonprofit. This practice, however, may result in misclassification, biasing the results. Nor do these datasets include comprehensive measures of benefits; therefore, the wage gap, rather than a more complete measure of total compensation, is used to measure the for-profit–nonprofit pay differential. In this article, we consider both wages and total compensation in evaluating the existence and magnitude of such a differential. We also use administrative data as the indicator of nonprofit status.

The article is organized into six sections. The next section describes the data used in the analysis. The third section presents wage and compensation measures separately for industry and occupational groups by nonprofit status. The fourth section offers an analysis of employer-provided benefits by nonprofit status. Results from a regression-based approach to measuring the compensation gap are presented in the fifth section. The final section summarizes the results.

In the first few years of the 21st century, staff from the Bureau of Labor Statistics (BLS) Quarterly Census of Employment and Wages (QCEW) program partnered with researchers from the Johns Hopkins University to produce a set of research data on nonprofits. The research method they used involved matching QCEW data with Internal Revenue Service (IRS) data on tax-exempt organizations.6 More recently, BLS researchers in the QCEW program revisited matching their data with the IRS Exempt Organization Business Master File (EOBMF) and created research data on the nonprofit sector that incorporate both information from the EOBMF and information on “reimbursable” establishments identified in state unemployment insurance reports.7 The resulting QCEW file includes indicators for nonprofit establishments (defined as 501(c)3 establishments). The QCEW provides the framework from which establishments are sampled for the National Compensation Survey (NCS).

From 2007 to 2010, the NCS published information on the wages of workers in private nonprofit establishments in the publication “National Compensation Survey: occupational earnings in the United States.”8 Given that this information has not been published since 2010, having a nonprofit indicator in the QCEW provides the opportunity to match that indicator with the establishment-level information collected in the NCS and produce estimates of wages, compensation, and benefits for private sector nonprofit and for-profit establishments. In what follows, we match data on private sector establishments from the March 2014 National Compensation Survey with the nonprofit indicator in the QCEW. Each establishment is assigned a unique multidigit identifying number when it first appears in the QCEW. This identifier is retained when establishments selected from the QCEW are added to the NCS. We subsequently used these identifying numbers to match NCS establishments back into the QCEW and were able to match 90 percent of establishments in the NCS with establishments in the QCEW.9 The estimates presented in this article are based on these matched establishments.

Nonprofit workers make up 11.7 percent of private sector workers. The proportion of nonprofit workers who work full time10 is 76.4 percent, statistically no different than the proportion of for-profit workers who work full time (73.3 percent).11 The proportion of union workers12 is also statistically equivalent across nonprofit status: 8.6 percent of nonprofits and 8.9 percent of for-profits.

At first glance, workers in nonprofits appear to receive higher wages and more costly benefits. Table 1 presents estimates of the average hourly wages for nonprofit and for-profit workers, as well as their total hourly compensation.13 Breakouts are provided for two of the most costly benefit categories: health insurance, and retirement and savings.

| Category | Nonprofit | Confidence interval | For-profit | Confidence interval |

|---|---|---|---|---|

| Total compensation | $36.62 | $34.51–$38.73 | $28.76 | $28.30–$29.23 |

| Wages | 25.30 | 23.92–26.68 | 20.17 | 19.86–20.47 |

| Health insurance | 3.21 | 3.05–3.37 | 2.22 | 2.17–2.27 |

| Retirement and savings | 1.66 | 1.31-2.00 | 1.08 | 1.03–1.12 |

| Source: U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation. | ||||

On average, workers at nonprofit establishments earn $5.13 per hour more than workers at for-profit establishments. The costs of health insurance benefits paid to nonprofit workers are also higher—$0.99 per hour more, on average—and the employer cost of retirement and savings plans is $0.58 per hour higher for workers at nonprofits. As a result, average total compensation for nonprofit workers is $7.86 per hour higher than that for for-profit workers.

A top-line look at the numbers, however, does not account for the fact that the industries in which we find nonprofit establishments are very different from those we see among for-profit establishments. Nonprofits also have a different pattern of occupational groups than for-profits have.

We first look at the industry distribution in the NCS by nonprofit status. (See table 2.) As one might expect, nonprofit establishments are found primarily in service-providing industries, particularly education and health services.

| Industry group | Share of nonprofit workforce | Share of for-profit workforce |

|---|---|---|

| Goods producing | — | 19 |

| Service providing | — | 81 |

| Trade, transportation, and utilities | — | 27 |

| Information | — | 2 |

| Financial activities | — | 7 |

| Professional and business services | 5 | 18 |

| Education and health services | 83 | 10 |

| Leisure and hospitality | — | 14 |

| Other services | 7 | 3 |

| Note: Dash indicates no workers in this category or data did not meet publication criteria. Source: U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation. | ||

There are just three industry groups in which data are sufficient to provide a comparison: professional and business services, education and health services, and the catchall group titled “other services.” Comparing wage and compensation costs between nonprofit and for-profit establishments by industry for these groups, we see a pay premium for workers in nonprofits within educational and health services and professional and business services. (See table 3.)

| Industry group | Average hourly wage | Confidence interval | Total compensation | Confidence interval | Health insurance | Confidence interval | Retirement and savings | Confidence interval |

|---|---|---|---|---|---|---|---|---|

| Nonprofit: | ||||||||

| Professional and business services | 32.29 | $28.04–$36.54 | 47.85 | $41.81–$53.39 | 4.34 | $3.67–$5.01 | 2.02 | $1.43–$2.59 |

| Education and health services | 25.60 | 23.99–27.20 | 37.17 | 34.72–39.62 | 3.32 | 3.15–3.49 | 1.73 | 1.32–2.15 |

| Other services | 18.31 | 15.73–20.89 | 24.79 | 21.31–28.28 | 1.46 | 1.11–1.82 | .93 | .67–1.19 |

| For-profit: | ||||||||

| Professional and business services | 25.09 | 24.06–26.11 | 34.75 | 33.29–36.21 | 2.18 | 2.06–2.30 | 1.15 | 1.05–1.25 |

| Education and health services | 19.15 | 17.69–20.62 | 25.89 | 23.63–28.15 | 1.72 | 1.53–1.90 | .54 | .30–.76 |

| Other services | 19.03 | 17.72–20.32 | 26.58 | 24.50–28.66 | 2.07 | 1.70–2.43 | 1.2 | .88–1.52 |

| Source: U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation. | ||||||||

Within professional and business services, wages for workers in nonprofits are, on average, $7.20 per hour more than those in for-profits. The gap increases to $13.10 per hour for total compensation. In education and health services, the nonprofit wage advantage is $6.45 per hour and the total-compensation gap is $11.28 per hour. For “other services,” there is no statistically significant difference in the average hourly wage or total compensation between nonprofits and for-profits.

Pay gaps by industry do not control for the different types of labor used in an establishment. For example, within education and health services, a nonprofit may employ a larger share of physicians and managers while a for-profit may employ a larger share of nursing assistants and janitorial staff. Past research finds that controlling for the type of work performed is critical in explaining wage gaps between workers at for-profits and workers at nonprofits.14

As seen in table 4, there are higher proportions of management, professional, and related workers and service workers, and lower proportions of sales and office workers; natural resources, construction, and maintenance workers; and production, transportation, and material moving workers, in nonprofits than in for-profits. Table 5 demonstrates that the mix of occupations explains a lot of the nonprofit wage premiums seen in tables 1 and 3.

| Occupation group | Share of nonprofit workforce | Confidence interval | Share of for-profit workforce | Confidence interval |

|---|---|---|---|---|

| Management, professional, and related | 55.6 | 52.8–58.4 | 21.1 | 20.3–21.9 |

| Service | 25.5 | 22.8–28.3 | 21.8 | 20.7–23.0 |

| Sales and office | 16.0 | 14.1–17.9 | 29.6 | 28.7–30.5 |

| Natural resources, construction, and maintenance | 1.6 | 1.0–2.2 | 8.8 | 8.2–9.3 |

| Production, transportation, and material moving | 1.2 | .8–1.7 | 18.6 | 17.9–19.4 |

| Note: Because of rounding, entries for occupation groups may not sum to 100 percent. Source: U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation. | ||||

| Occupation group | Hourly wage | Confidence interval | Total compensation | Confidence interval | Health insurance | Confidence interval | Retirement and savings | Confidence interval |

|---|---|---|---|---|---|---|---|---|

| Nonprofit: | ||||||||

| Management, professional, and related | $34.14 | $31.96–$36.31 | $49.09 | $45.75–$52.73 | $3.90 | $3.68–$4.11 | $2.45 | $1.83–$3.06 |

| Service | 12.39 | 11.91–12.87 | 18.01 | 17.11–18.90 | 1.87 | 1.65–2.08 | .48 | .41–.54 |

| Sales and office | 16.57 | 15.88–17.25 | 24.71 | 23.60–25.82 | 3.01 | 2.73–3.28 | .87 | .76–.97 |

| Natural resources, construction, and maintenance | 20.19 | 18.23–22.14 | 31.17 | 28.15–34.18 | 3.44 | 2.85–4.02 | 1.39 | 1.12–1.66 |

| Production, transportation, and material moving | 14.02 | 11.63–16.40 | 21.28 | 16.74–25.81 | 2.24 | 1.35–3.13 | .86 | .25–1.46 |

| For-profit: | ||||||||

| Management, professional, and related | 37.50 | 36.56–38.44 | 53.76 | 52.34–55.19 | 3.49 | 3.39–3.60 | 2.41 | 2.24–2.57 |

| Service | 10.40 | 10.09–10.72 | 13.45 | 13.02–13.89 | .69 | .62–.75 | .17 | .15–.20 |

| Sales and office | 16.25 | 15.87–16.62 | 22.64 | 22.14–23.14 | 1.97 | 1.90–2.03 | .62 | .59–.66 |

| Natural resources, construction, and maintenance | 22.20 | 21.61–22.79 | 32.86 | 31.78–33.95 | 2.74 | 2.57–2.91 | 1.79 | 1.55–2.02 |

| Production, transportation, and material moving | 17.27 | 16.87–17.67 | 26.21 | 25.53–26.90 | 2.74 | 2.61–2.86 | 1.01 | .93–1.08 |

| Source: U.S. Bureau of Labor Statistics, Employer Costs for Employee Compensation. | ||||||||

Wages of management, professional, and related workers at nonprofits are, on average, $3.36 per hour less than those of their counterparts employed by for-profits. Once the cost of benefits is added in, the difference in total compensation is $4.67 per hour less. Workers employed in production, transportation, and material moving occupations at nonprofits earn $3.25 per hour less, on average, than for-profit workers earn; when the cost of benefits is included, the difference in mean total compensation is $4.93 per hour less.

Service workers at nonprofits earn $1.99 per hour more than service workers at for-profit establishments, and the gap increases to $4.56 per hour for total compensation. The wage gap for sales and office workers is not statistically different from zero; however, the mean total compensation of these workers in nonprofits is $2.07 per hour more than that of sales and office workers at for-profit establishments.

Thus, comparing nonprofit and for-profit pay, even at broad occupational groupings, gives a different picture than the aggregate estimates provide. Across all private sector workers, those at nonprofits earn more than those at for-profit establishments, but this gap is driven largely by differences in occupations seen in these establishments. Managers and professionals make up a disproportionately large share of workers at nonprofits (an observation which makes sense, given that nonprofits tend to be colleges, universities, and hospitals), and the high average earnings of managers skew the aggregate numbers. Accordingly, when we examine pay by occupational group, we see groups for which the wages of nonprofit workers are lower than those of corresponding workers at for-profit firms. We also see different measures of the pay gap, whether we examine wages or total compensation. Gaps in total compensation suggest that nonprofits and for-profits either have a different likelihood of offering benefits, offer benefits that differ in their generosity, or both.

We turn next to an examination of the types of benefits offered to workers by nonprofit and for-profit establishments. We focus on health insurance and on retirement and savings benefits, and we split retirement and savings benefits into defined-benefit plans and defined-contribution plans. Table 6 presents the availability of health and retirement plans by nonprofit and for-profit status for broad occupational groups.

| Occupation group | Health insurance offered | Defined benefit offered | Defined contribution offered | |||||||||

|---|---|---|---|---|---|---|---|---|---|---|---|---|

| Nonprofit | CI | For-profit | CI | Nonprofit | CI | For-profit | CI | Nonprofit | CI | For-profit | CI | |

| All workers | 81 | 67 | 25 | 17 | 68 | 59 | ||||||

| Management, professional, and related | 88 | 85–90 | 87 | 85–88 | 28 | 25–31 | 25 | 23–26 | 75 | 72–78 | 76 | 74–78 |

| Service | 65 | 58–71 | 36 | 33–39 | 20 | 16–24 | 5 | 4–6 | 54 | 47–61 | 32 | 29–34 |

| Sales and office | 86 | 82–90 | 68 | 67–70 | 22 | 17–27 | 16 | 15–17 | 66 | 59–73 | 65 | 63–66 |

| Natural resources, construction, and maintenance | — | … | 75 | 72–78 | — | … | 24 | 21–26 | — | … | 59 | 56–62 |

| Production, transportation, and material moving | — | … | 76 | 74–79 | — | … | 23 | 22–25 | — | … | 61 | 59–64 |

| Note: Dash indicates no workers in this category or data did not meet publication criteria. CI = Confidence interval. Source: U.S. Bureau of Labor Statistics, National Compensation Survey. | ||||||||||||

Employees at nonprofits are more likely than workers at for-profits to be offered benefits. Eighty-one percent of all workers at nonprofit establishments are offered medical plans by their employers, compared with 67 percent of workers at for-profit establishments. This disparity cannot be attributed simply to the disproportionate share of managers and professionals at the former establishments. In fact, there was no statistically significant difference in the offering of medical plans for management and professional workers by nonprofit status. Most striking is that sales and office workers and service workers at nonprofit establishments are much more likely than their counterparts at for-profit establishments to be offered medical plans. The gap for service workers is nearly 30 percentage points.

Nonprofits are more likely than for-profit establishments to offer defined-benefit plans. This difference is driven mostly by service workers. Nonprofits are also more likely than for-profits (68 percent versus 59 percent) to offer defined-contribution plans. Again, this difference is driven largely by the benefits offered to service workers: fifty-four percent of service workers at nonprofits are offered defined-contribution plans, as opposed to 32 percent of service workers at for-profits.

Although comparisons of wages and compensation by broad occupational groups provide some evidence of pay gaps between for-profits and nonprofits, such gaps may be the result of workers at nonprofits doing substantially different types of work than those at for-profits. In this regard, it is likely that the service workers one sees at nonprofits have very different jobs than the service workers one sees at for-profits. For example, healthcare support occupations are more prevalent among nonprofits and food preparations occupations are more prevalent among for-profits. One approach to controlling for this likelihood might be to compare wages for detailed occupations, as defined by the Standard Occupational Classification system. Unfortunately, the relatively small sample size of the NCS makes this approach infeasible.

The NCS has a unique feature, however, that allows comparison of levels of work. Most jobs in the NCS undergo a process of “point leveling,” whereby they are assigned points on the basis of four factors: knowledge, job controls and complexity, contacts, and physical environment.15

We incorporate this leveling into the regression analysis that follows, enabling us to assess how controlling for job characteristics affects the pay differential between for-profits and nonprofits by broad occupational group. Regressions are estimated first with the natural logarithm of the hourly wage as the dependent variable and then with the natural logarithm of hourly total compensation as the dependent variable.

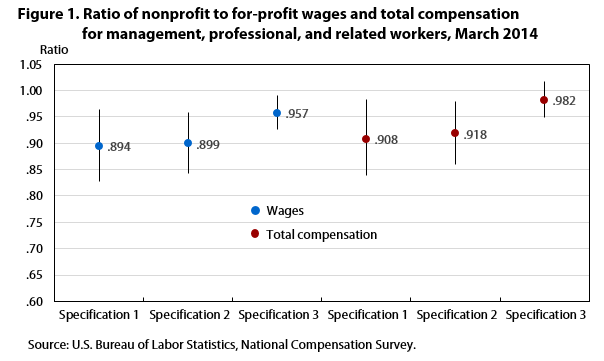

We estimate three specifications: (1) no controls, aside from an indicator variable for nonprofit status; (2) an indicator variable for nonprofit status, as well as indicators for full-time and union coverage; (3) the variables identified in (2), as well as the total number of leveling points and its square.16 Because we are interested in the relative pay between nonprofit and for-profit jobs, we focus on the estimates of the nonprofit coefficients. To allow easier interpretation of relative pay, figures 1–3 present the exponents on the coefficient of the nonprofit indicator for the three largest broad occupational groups: management, professional, and related workers; service workers; and sales and office workers.

The measure eb, where b is the coefficient from the regression with the natural logarithm of the hourly wage as the dependent variable, can be interpreted to mean that a worker in a nonprofit job earns eb times the pay of the equivalent worker in a for-profit job. If eb < 1, then the nonprofit pay is less than the for-profit pay; if eb > 1, then the nonprofit pay is more than the for-profit pay. The associated confidence interval is a 95-percent interval (i.e., p ≤ .05); if the confidence interval contains the number 1.0, then there is no statistical difference in the pay of nonprofit and for-profit workers for the given job.

| Confidence interval | Wage | Total compensation | ||||

|---|---|---|---|---|---|---|

| Specification 1 | Specification 2 | Specification 3 | Specification 1 | Specification 2 | Specification 3 | |

| Upper value | 0.965 | 0.959 | 0.99 | 0.984 | 0.98 | 1.017 |

| Lower value | .828 | .843 | .926 | .838 | .860 | .948 |

| Mean | .894 | .899 | .957 | .908 | .918 | .982 |

| Source: U.S. Bureau of Labor Statistics, National Compensation Survey. | ||||||

Controlling for job characteristics matters a great deal in estimating the wage gap between nonprofit and for-profit workers. The left half of each figure shows the value of eb—equivalent to the wage ratio of nonprofit to for-profit workers—and the right half shows the estimated total-compensation ratio—also of nonprofit to for-profit workers—for the three specifications shown. Turning first to figure 1, we see that controlling for job characteristics lessens the wage gap between nonprofit and for-profit workers: once the levels of the job are included in the wage regression, management, professional, and related workers at nonprofit businesses are seen to earn wages that are 96 percent of the level of their for-profit counterparts. Estimates from the model that uses the logarithm of total compensation as the dependent variable show that the ratio of nonprofit to for-profit compensation for these workers is 0.98.

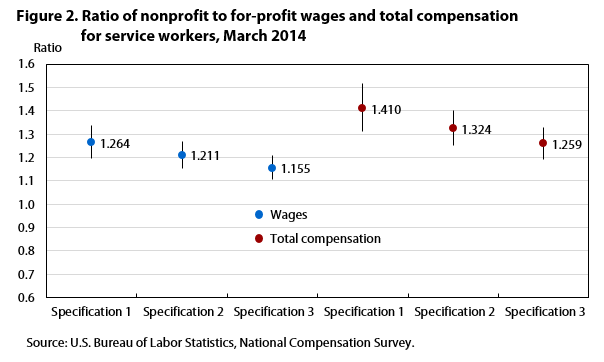

| Confidence interval | Wage | Total compensation | ||||

|---|---|---|---|---|---|---|

| Specification 1 | Specification 2 | Specification 3 | Specification 1 | Specification 2 | Specification 3 | |

| Upper value | 1.336 | 1.269 | 1.209 | 1.517 | 1.401 | 1.328 |

| Lower value | 1.196 | 1.155 | 1.104 | 1.311 | 1.251 | 1.193 |

| Mean | 1.264 | 1.211 | 1.155 | 1.410 | 1.324 | 1.259 |

| Source: U.S. Bureau of Labor Statistics, National Compensation Survey. | ||||||

Recall from table 5 that service workers in nonprofits have higher wages and higher total compensation than for-profit workers have. This fact would lead us to anticipate a nonprofit to for-profit ratio greater than 1 for these workers. Figure 2 shows this wage premium. Although the point estimates of the ratio appear to decrease as we add job characteristic controls to the model, the lower bound of the 95-percent confidence level for specification 1 is roughly equivalent to the upper bound of the 95-percent confidence interval for specification 3, for both the wage and total-compensation models. Therefore, we cannot say definitively that the point estimates are statistically decreasing. When we control for leveling, the point estimate for the wage ratio indicates that service workers employed at nonprofits earn 16 percent more than those at for-profits, and the gap becomes roughly 26 percent once total compensation is considered, even upon controlling for union membership, full-time work, and job level.

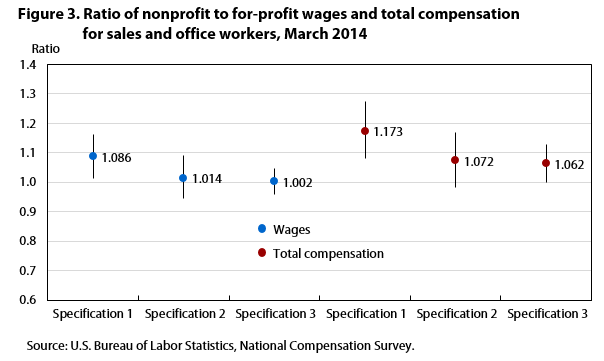

| Confidence interval | Wage | Total compensation | ||||

|---|---|---|---|---|---|---|

| Specification 1 | Specification 2 | Specification 3 | Specification 1 | Specification 2 | Specification 3 | |

| Upper value | 1.162 | 1.089 | 1.047 | 1.275 | 1.169 | 1.128 |

| Lower value | 1.014 | .944 | .958 | 1.079 | .983 | 1.000 |

| Mean | 1.086 | 1.014 | 1.002 | 1.173 | 1.072 | 1.062 |

| Source: U.S. Bureau of Labor Statistics, National Compensation Survey. | ||||||

With no controls, sales and office workers at nonprofits appear to have a wage and total-compensation advantage over those at for-profits. (See figure 3.) However, once all job characteristics, including levels, are controlled for, the nonprofit–for-profit ratio is equivalent to 1.0 for both wages and total compensation.

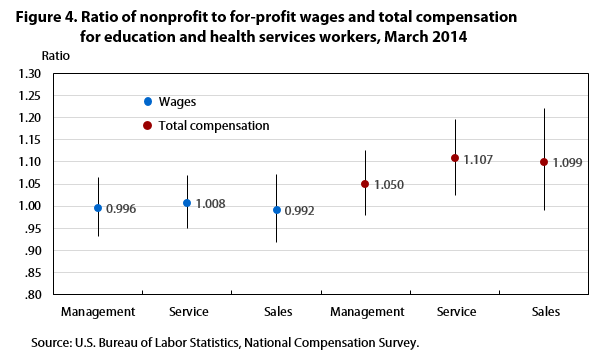

| Confidence interval | Wage | Total compensation | ||||

|---|---|---|---|---|---|---|

| Specification 1 | Specification 2 | Specification 3 | Specification 1 | Specification 2 | Specification 3 | |

| Upper value | 1.065 | 1.07 | 1.072 | 1.126 | 1.196 | 1.221 |

| Lower value | .932 | .949 | .919 | .979 | 1.025 | .990 |

| Mean | .996 | 1.008 | .992 | 1.05 | 1.107 | 1.099 |

| Source: U.S. Bureau of Labor Statistics, National Compensation Survey. | ||||||

In these models, we are unable to control for industry. As seen in table 2, some industries have very few nonprofit workers, a circumstance that poses problems for including industry indicators in regression analysis. Fortunately, the industry grouping of education and health services workers has a sample size large enough to estimate wage and total-compensation models. Rather than reporting the results for all three specifications, we present only the results from specification 3 (containing the full set of job controls), shown in figure 4 for all three occupational groups.

Within the broad industry group of education and health services, once we control for job characteristics, there is no statistical difference in nonprofit and for-profit wages for any occupational group. (All confidence intervals for the exponent of the coefficient contain the number 1.0.) Although the point estimates for total compensation are greater than 1.0 for management, professional, and related workers and for sales and office workers, neither of these point estimates is statistically different from 1.0. The only group for which there is a compensation ratio statistically different from 1.0 is service workers: nonprofit service workers in education and healthcare earn a statistically significant 11 percent more than their for-profit counterparts.

Matching QCEW and NCS data enables us to generate estimates of wage and compensation costs by nonprofit and for-profit status. The estimates indicate that, in the aggregate, nonprofit workers earn a pay premium, but still, industry and occupation patterns differ greatly between nonprofits and for-profits and explain a great deal of the pay gap.

Using regression analysis to control for the level of work performed, we find a slight wage disadvantage for management, professional, and related workers at nonprofits, a wage advantage for service workers at nonprofits, and no statistical wage gap between nonprofit and for-profit sales and office workers. If we use total compensation costs rather than wages as our pay measure, the results change: there is no statistical compensation gap between nonprofit and for-profit businesses for management, professional, and related workers and for sales and office workers, but there is a compensation premium for service workers at nonprofits. These results highlight the importance of a pay measure that includes benefits: across both occupations and levels, workers at nonprofits receive more costly benefits. Thus, ignoring this component of pay can lead to incorrect inferences regarding the pay gap.

It is not possible to control for industry in our analysis because of the relatively small share of nonprofit workers in some industries. We note, however, that if we restrict the analysis to educational and health service industries, we find a persistent total compensation premium for service workers employed at nonprofits.

John L. Bishow, and Kristen Monaco, "Nonprofit pay and benefits: estimates from the National Compensation Survey," Monthly Labor Review, U.S. Bureau of Labor Statistics, January 2016, https://doi.org/10.21916/mlr.2016.4

1 See Martin S. Feldstein, The rising cost of hospital care (Washington, DC: Information Services Press, 1971).

2 See Susan Rose-Ackerman, “Altruism, nonprofits, and economic theory,” Journal of Economic Literature, June 1996, vol. 34, no. 2, pp. 701–728.

3 Laura Leete, “Whither the nonprofit wage differential? Estimates from the 1990 census,” Journal of Labor Economics, January 2001, vol. 19, no. 1, pp. 136–170.

4 Edward J. Schumacher, “Does public or not-for-profit status affect the earnings of hospital workers?” Journal of Labor Research, March 2009, vol. 30, no. 1, pp. 9–34.

5 Christopher J. Ruhm and Carey Borkoski, “Compensation in the nonprofit sector,” The Journal of Human Resources, autumn 2003, vol. 38, no. 4, pp. 992–1021.

6 A comprehensive description of the project is found in Lester M. Salamon and S. Wojciech Sokolowski, “Nonprofit organizations: new insights from QCEW data,” Monthly Labor Review, September 2005, pp. 19–26, https://www.bls.gov/opub/mlr/2005/09/art3full.pdf.

7 For a detailed description of the matching process, see “Research data on the nonprofit sector,” Business Employment Dynamics (U.S. Bureau of Labor Statistics, April 30, 2015), https://www.bls.gov/bdm/nonprofits/nonprofits.htm.

8 The information presented was based on the BLS Locality Pay Survey (LPS). The last of these NCS reports is “National Compensation Survey: occupational earnings in the United States, 2010,” National Compensation Survey, Bulletin 2753 (U.S. Bureau of Labor Statistics, May 2011), https://www.bls.gov/ncs/ncswage2010.htm. The LPS was discontinued with the 2011 federal budget. (See “Announcement,” National Compensation Survey—wages (U.S. Bureau of Labor Statistics), https://www.bls.gov/ocs/.) The data in the NCS publication provided the basis for two BLS reports by Amy Butler in Compensation and Working Conditions that compared the wages of nonprofit workers with the wages of those employed at for-profit firms as well as the wages of state and local government workers: “Wages in the nonprofit sector: management, professional, and administrative support occupations” (U.S. Bureau of Labor Statistics, October 28, 2008); and “Wages in the nonprofit sector: occupations typically found in educational and research institutions” (U.S. Bureau of Labor Statistics, November 26, 2008).

9 We analyzed matched and unmatched NCS data to determine whether both establishment size and average compensation were statistically different between the two groups. The point estimates obtained indicate that the matched establishments were less likely to employ fewer than 50 workers and more likely to have slightly higher average compensation, but the differences were not statistically significant.

10 The NCS defines “full time” and “part time” on the basis of the establishment’s definition of these terms, not on actual number of hours worked.

11 All significance testing for this article was performed at the 95-percent level of confidence.

12 A union worker is defined as a worker who is covered by a collective-bargaining agreement.

13 Throughout this article, “wages” refers to wages and salaries.

14 See, for instance, Zack Warren, “Occupational employment in the not-for-profit sector,” Monthly Labor Review, November 2008, pp. 11–43, https://www.bls.gov/opub/mlr/2008/11/art2full.pdf; Leete, “Whither the nonprofit wage differential?”; Schumacher, “Does public or not-for-profit status?” and Ruhm and Borkoski, “Compensation in the nonprofit sector.”

15 For more details on the leveling process, see “National Compensation Survey: guide for evaluating your firm’s jobs and pay,” May 2013, https://www.bls.gov/ncs/ocs/sp/ncbr0004.pdf.

16 Initial analysis provided evidence of a quadratic relationship between the logarithm of pay and the number of leveling points; that is, pay tends to increase with the point total, but in a nonlinear fashion.