An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

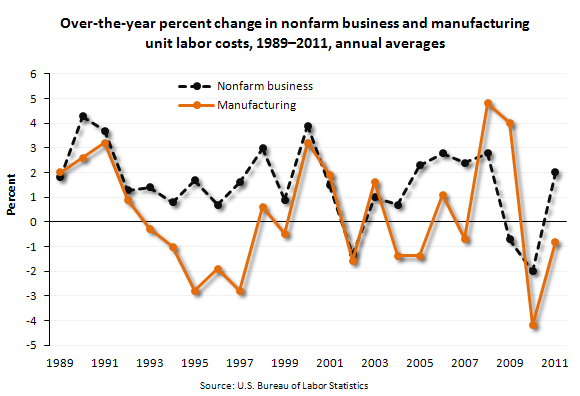

For 2011, in both the nonfarm business and manufacturing sectors, annual average growth in unit labor costs was revised upward; this was due to upward revisions to hourly compensation and downward revisions to productivity.

In the nonfarm business sector, unit labor costs rose 2.0 percent in 2011 and declined 0.8 percent in the manufacturing sector.

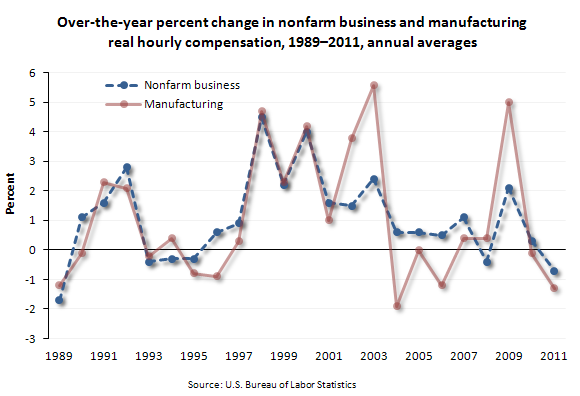

In 2011, real hourly compensation, which takes into account changes in consumer prices, decreased 0.7 percent in the nonfarm business sector. This is the largest annual decline in the measure since a 1.7-percent decline in 1989.

Real hourly compensation in the manufacturing sector decreased 1.3 percent in 2011, the largest decline in the measure since a 1.9-percent decline in 2004.

These data are from the Productivity and Costs program and are subject to revision. Labor compensation includes accrued wages and salaries, supplements, employer contributions to employee benefit plans, and taxes. Unit labor costs describe the relationship between compensation per hour and productivity, or real output per hour, and can be used as an indicator of inflationary pressure on producers. For more information, see "Productivity and Costs: Fourth Quarter and Annual Averages 2011, Revised" (HTML) (PDF), news release USDL-12-0401.

Bureau of Labor Statistics, U.S. Department of Labor, The Economics Daily, Unit labor costs and real hourly compensation, 2011 at https://www.bls.gov/opub/ted/2012/ted_20120308.htm (visited August 03, 2026).