An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

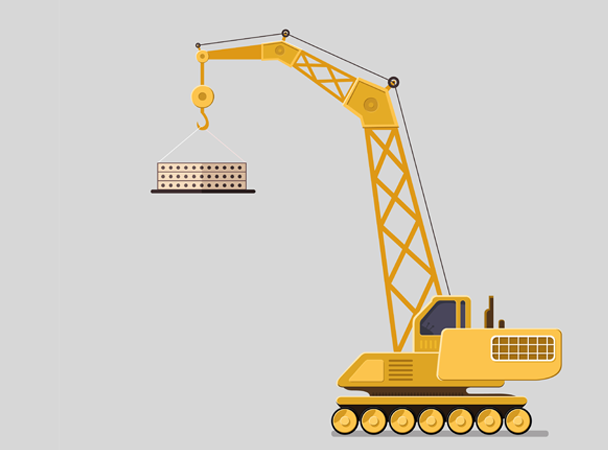

Example: a construction company buys a crane today, and uses the crane to build apartments for many years.

Capital input is not measured by the initial purchase of the crane, but by the services, such as lifting and moving materials, that it provides to the construction company each year thereafter.

The flow of capital services from a building, machinery or a research idea changes over time, usually becoming less productive as it erodes, deteriorates, or becomes obsolete or incompatible with other equipment.

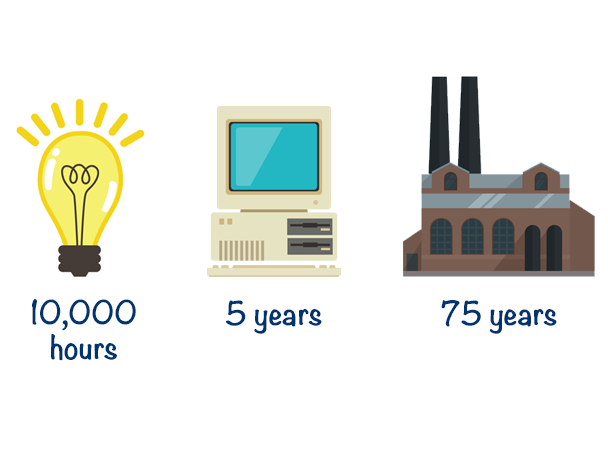

Each type of capital has its own expected life—how long it can be used in production before it is completely deteriorated or obsolete.

Each type of capital also reaches the end of that expected life (through deteriorating or becoming obsolete at its own rate).

A light bulb, for example, doesn’t deteriorate at all, giving the same light hour after hour, until it suddenly stops completely (on average 10,000 hours after first use).

By comparison, a laptop begins to deteriorate shortly after purchase, especially the battery. By the second year, the battery may need replacing. Additionally, new software will be incompatible with the laptop, making it obsolete.

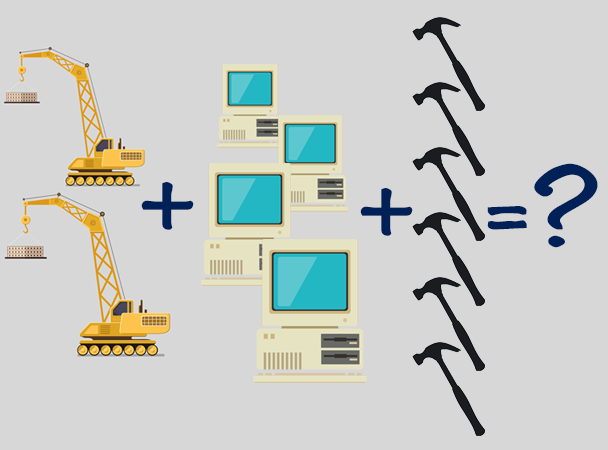

These different capital assets are combined into a single index of capital for each industry or sector.

How do we combine, for example, the productive capacity from 2 cranes, 4 computers and 6 hammers?