An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

To assist users in ascertaining the reliability of Employer Costs for Employee Compensation (ECEC) estimates, BLS provides relative standard errors (RSEs). Relative standard errors (expressed as a percentage of cost) provide users a measure of the precision of an estimate to ensure that it is within an acceptable range for its intended purpose. See the HTML or PDF relative standard errors tables for current quarter news releases. Historical relative standard errors are available through the public database and in spreadsheet format.

Relative standard errors relate to differences that occur from sampling errors, but not from nonsampling errors. Sampling errors are differences between the results computed from a sample of observations and those computed from all observations in the population. In the case of the ECEC, the population of an estimate is an industry or occupation in the civilian, private, or state and local government sector. Estimates derived from different samples selected using the same sample design may differ from each other.

Nonsampling errors are not measured. One type of nonsampling error is survey nonresponse, when survey respondents are unwilling or unable to participate in the survey. Other nonsampling errors include inaccurate or incorrectly entered data, and processing errors. BLS quality assurance programs contain procedures for reducing nonsampling errors. These procedures include data collection reinterviews, observed interviews, and systematic reviews of collected data. Finally, field economists (data collectors) undergo extensive training to maintain high data collection standards.

BLS provides measures of reliability for all current National Compensation Survey (NCS) programs: standard errors for the Employment Cost Index (ECI) and the Employee Benefits estimates, and relative standard errors (reported as a percentage of the estimate value) for estimates in the ECEC.

ECI and Employee Benefits estimates are themselves relative values: percent changes and index values for ECI, and percentage shares for Employee Benefits. If an ECI series is estimated to increase by 1.0 percent over a time period and the standard error is 0.2 percent, then this implies a relative standard error of 0.2/1.0, or 20 percent. Reporting an error of 20 percent for an estimate of 1.0 percent would be confusing because the standard error and the estimate it refers to are in the same units. However, the error is one-fifth the amount of the estimate, not twenty times the estimate. The ECI would report the standard error (0.2 percent) instead, for clarity.

ECEC estimates are reported as dollar amounts or, for components of total compensation, as a percentage of total compensation. For dollar amounts, a standard error reported in the same unit provides less information than a relative standard error. There is no inherent value of knowing the dollar amount of a standard error – which is an abstraction – without knowing how it is proportional to the estimate. Relative standard errors are also available for ECEC percentages of total compensation.

Standard errors can be used to measure the precision with which an estimate from a particular sample approximates the expected result (value) of all possible samples (population). The chances are about 68 out of 100 that an estimate from the survey differs from a population result within one standard error. The chances are about 90 out of 100 that this difference would be within 1.645 standard errors.

The standard errors can be used to calculate confidence intervals around an estimate. If all possible samples were selected and an estimate of a value and its sampling error were computed for each, then (for approximately 90 percent of the samples) the intervals from 1.645 standard errors below the estimate to 1.645 standard errors above the estimate would include the "true" average value.

Total compensation for civilian workers = $37.03

Relative standard error = 1.3 %

Step 1. Calculate the standard error

Standard error = relative standard error * estimate

Standard error = 0.013 * $37.03

Standard error = $0.48

Step 2. Calculate a 90% confidence interval

Confidence interval = estimate +/- (critical value * standard error)

Confidence interval = $37.03 +/- (1.645 * $0.48)

Confidence interval = [$36.24, $37.82]

If all possible samples were drawn from the target population, and each time a new estimate and confidence interval were calculated, then 90 percent of those confidence intervals would contain the true population value. Therefore, we are 90 percent confident that the interval [$36.24, $37.82] will contain all possible sample means with NCS sample design.

If you wish to calculate a 95 percent confidence interval, replace the critical value of 1.645 with 1.960. For a 99 percent confidence interval, use 2.576 as the critical value.

Comparative statements appearing in ECEC publications are statistically significant at the 90 percent level of confidence, unless otherwise indicated. A statistically significant difference is a result that is not attributed to chance alone. Differences between estimates which may appear to be substantial at first glance may not be statistically significant.

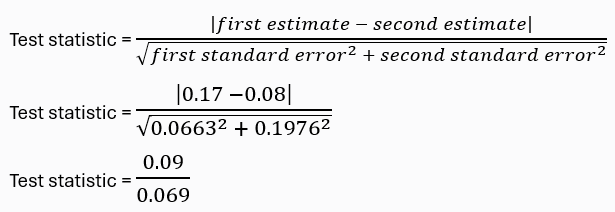

Evaluate the statement: “Health insurance costs are higher for full-time workers ($0.17) than for part-time workers ($0.08).”

Step 1. Calculate the standard errors for each estimate

Health insurance costs for full-time workers = $0.17

Relative standard error = 39.0%

Standard error = relative standard error * estimate

Standard error = 0.390 * $0.17

Standard error = $0.0663

Health insurance costs for part-time workers = $0.08

Relative standard error = 24.7%

Standard error = relative standard error * estimate

Standard error = 0.247 * $0.08

Standard error = $0.1976

Step 2. Calculate a statistical significance test statistic

Test statistic ≈ 1.304

Step 3. Compare against the critical value

A difference is statistically significant if the test statistic is greater than the critical value.

1.304 < 1.645

The test statistic (1.304) is less than the critical value (1.645). Therefore, the difference between the estimates is not statistically significant. That is, the comparative statement that health insurance costs for full-time workers is larger than costs for part-time workers does not pass the statistical significance test.

Note: examples are for illustrative purposes only and are not intended to represent current data.

For a more detailed explanation of relative standard errors, see Calculating estimate reliability in the Calculation section of the Handbook of Methods and the article Measuring Trends in the Structure and Levels of Employer Costs for Employee Compensation. For a detailed explanation of how to use standard error data to analyze differences in year-to-year changes, see Analyzing Year-to-Year Changes in Employer Costs for Employee Compensation.

Last Modified Date: November 14, 2025