An official website of the United States government

An official website of the United States government

The .gov means it's official.

Federal government websites often end in .gov or .mil. Before sharing sensitive information,

make sure you're on a federal government site.

The site is secure.

The

https:// ensures that you are connecting to the official website and that any

information you provide is encrypted and transmitted securely.

The Office of Productivity and Technology (OPT) measures how efficiently the U.S. converts inputs into the outputs of goods and services. Measures of labor productivity compare the growth in output to the growth in hours worked and measures of total factor productivity (TFP), also known as multifactor productivity (MFP), compare growth in output to the growth in a combination of inputs that include labor, capital, energy, materials, and purchased services.

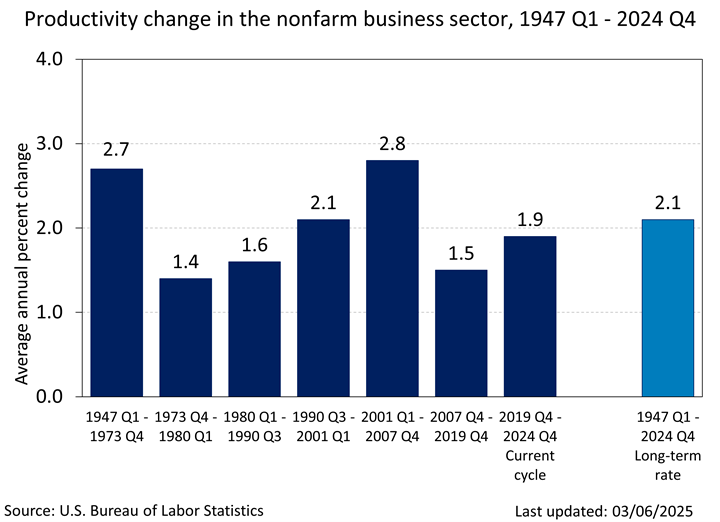

Click the graphic to enlarge chart: Long-term labor productivity in the nonfarm business sector since 1947.

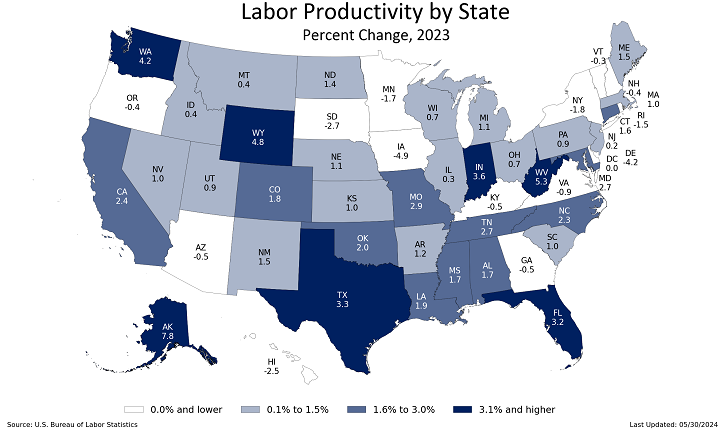

Click the graphic to enlarge chart: Labor Productivity by State, Percent Change.

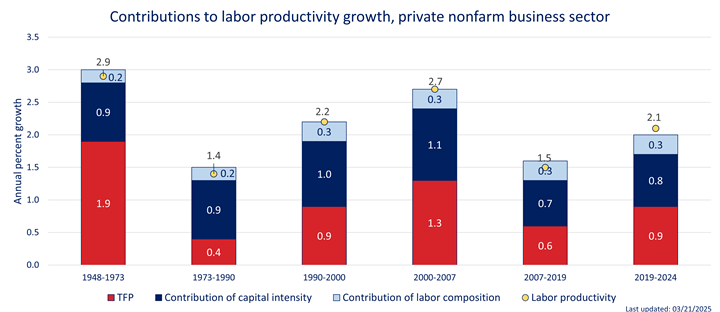

Click the graphic to enlarge chart: Contributions to Labor Productivity Growth, Private Nonfarm Business Sector, Selected Time Periods.

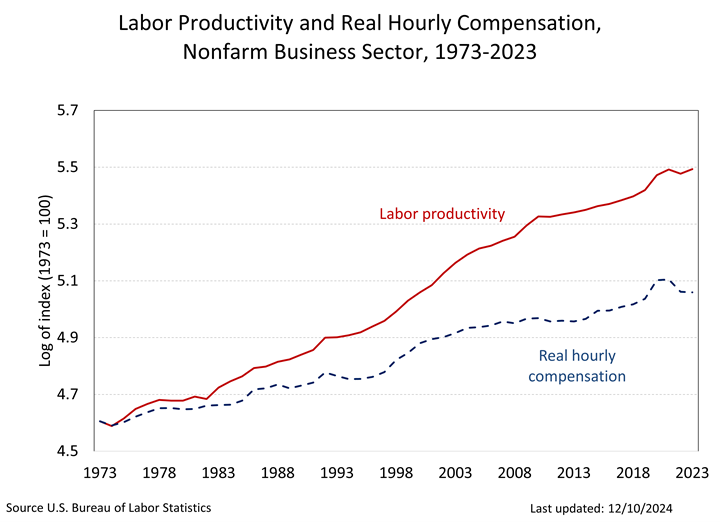

Click the graphic to enlarge chart: Labor Productivity and Real Hourly Compensation, Nonfarm Business Sector since 1973.

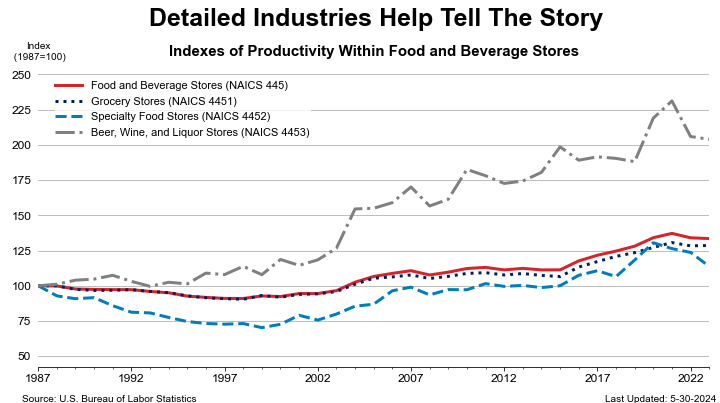

Click the graphic to enlarge chart: Detailed Industries Help Tell the Story, Indexes of Productivity Within Food and Beverage Stores.

Labor productivity (output per hour)

+0.3%(r) in 1st Qtr of 2026

![]()

Hourly compensation

+2.1%(r) in 1st Qtr of 2026

![]()

Unit labor costs

+1.8%(r) in 1st Qtr of 2026

![]()

Real value-added output

+1.0%(r) in 1st Qtr of 2026

![]()

Hours worked

+0.7% in 1st Qtr of 2026

![]()

Labor productivity (output per hour)

+3.2%(r) in 1st Qtr of 2026

![]()

Hourly compensation

+5.5%(r) in 1st Qtr of 2026

![]()

Unit labor costs

+2.2%(r) in 1st Qtr of 2026

![]()

Real sectoral output

+3.3% in 1st Qtr of 2026

![]()

Hours worked

unchanged in 1st Qtr of 2026

![]()

06/04/2026

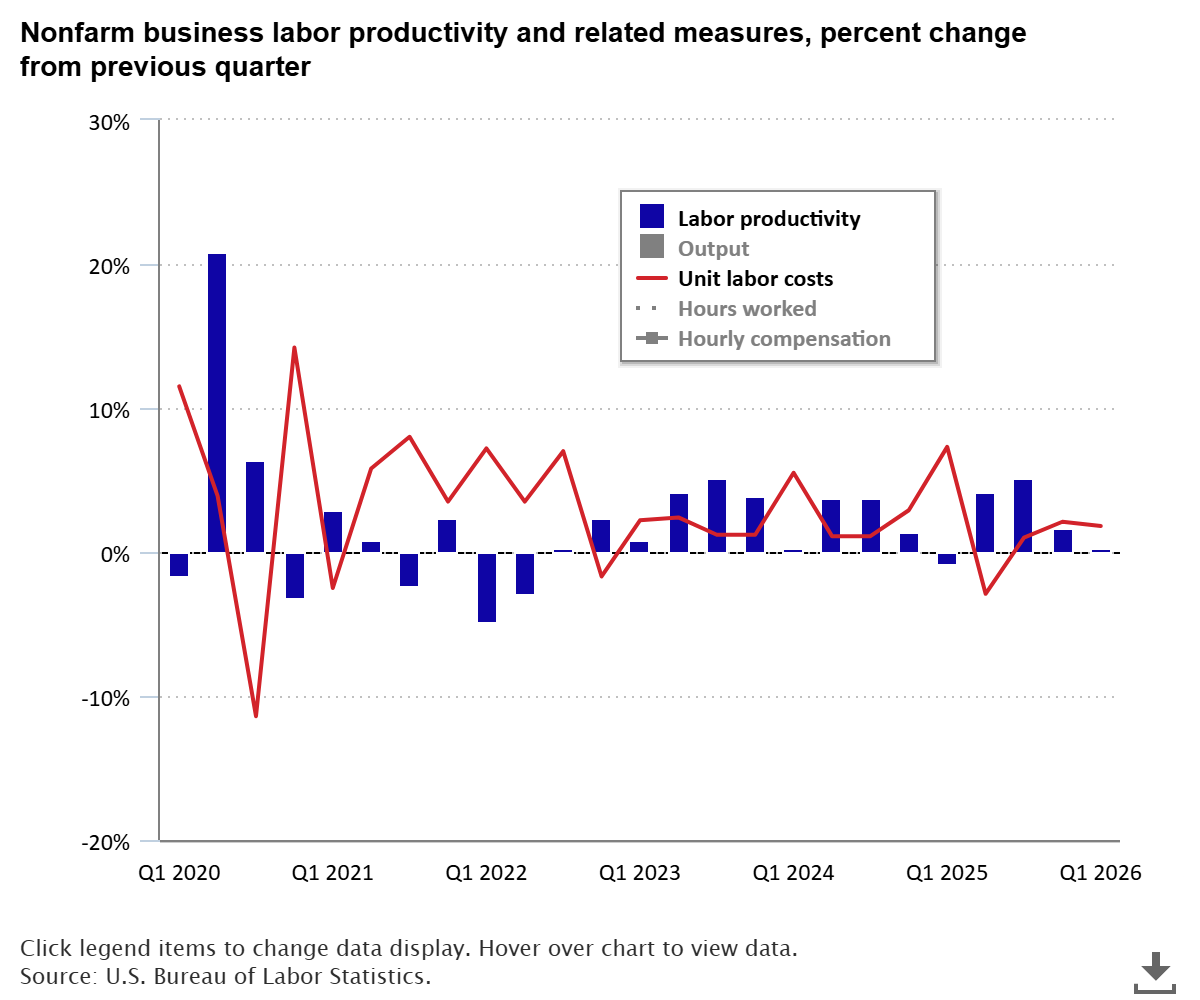

Productivity increased 0.3 percent in the nonfarm business sector in the first quarter of 2026; unit

labor costs increased 1.8 percent (seasonally adjusted annual rates). In manufacturing,

productivity increased 3.2 percent and unit labor costs increased 2.2 percent.

HTML

|

PDF

|

RSS

|

Charts

06/24/2026

Labor productivity increased in 39 of 80 covered four-digit NAICS manufacturing industries and in 2 of 5 mining industries in 2025. Output fell in 66 of 85 manufacturing and mining industries while hours worked fell in 52 industries. Seven industries increased both output and hours worked.

HTML

|

PDF

|

RSS

|

Charts

05/28/2026

Labor productivity increased in 42 states and the District of Columbia in 2025. Output increased in all 50

states and the District of Columbia and hours worked increased in 33 states.

HTML

|

PDF

|

RSS

|

Charts

06/26/2025

Labor productivity rose in 20 of 31 selected service-providing industries in 2024. Output increased in 21 industries while hours worked rose in 13 industries. Unit labor costs went up in 25 of the 31 industries.

HTML

|

PDF

|

RSS

|

Charts

05/28/2026

Wholesale trade productivity increased 4.4 percent in 2025 with retail trade productivity up 2.9 percent. Output grew and hours worked fell in both sectors. Unit labor costs declined 0.4 percent in wholesale trade and dropped 0.7 percent in retail trade.

HTML

|

PDF

|

RSS

|

Charts

06/24/2026

Total factor productivity fell in 70 of 86 4-digit NAICS manufacturing industries in 2023, up from 65 industries that declined in 2022. Output fell in 64 industries while intermediate inputs grew in 56 industries and capital increased in 31 industries.

HTML

|

PDF

|

RSS

12/19/2025

In 2024, total factor productivity increased in 13 out of 21 major industries, led by the retail trade and the agriculture, forestry, fishing and hunting industries.

HTML

|

PDF

|

RSS

|

Charts

03/19/2026

Total factor productivity increased 0.8 percent in the private

nonfarm business sector in 2025 as output

increased 2.6 percent and combined inputs increased 1.7 percent.

HTML

|

PDF

|

RSS

The COVID-19 pandemic brought about dramatic changes in the work environment. Although 6.5 percent of workers in the private business sector worked primarily from home in 2019, the pandemic was the start of a massive experiment in full-time remote work for most workers and firms. People often ask: are workers more productive or less productive when working from home? read more »

Artificial intelligence (AI) is an emerging technological innovation in many aspects of production and across many industries. The U.S. Bureau of Labor Statistics (BLS) implicitly captures AI use through its capital measure of software used in production. This article uses data from the BLS productivity program to break down recent investment growth by asset category and, more specifically, to examine recent investment in the software category. read more »

Nonfarm business sector labor productivity increased 0.3 percent in the first quarter of 2026, as output increased 1.0 percent and hours worked increased 0.7 percent. This is the smallest increase in nonfarm business sector labor productivity since the first quarter of 2025, when there was a 0.9-percent decrease. read more »

This Spotlight on Statistics reviews historical establishment, employment, and wage trends for the amusement and theme parks industry. Additionally, productivity, consumer expenditures for entertainment fees and admissions, and producer prices for select amusement and theme parks products are reviewed. read more »